High-risk insurance pools are a concept in health insurance that segregates individuals with pre-existing medical conditions from the conventional individual market. This separation results in lower premiums for those in the standard pool and higher premiums for those in the high-risk pool. Before the Affordable Care Act (ACA) mandated that insurers cover people with pre-existing conditions, 35 states had high-risk pools that provided insurance for those deemed uninsurable by the individual market. Since the ACA standardized the individual market and prohibited medical underwriting, high-risk pools are no longer necessary. However, the idea of high-risk pools has resurfaced as a potential way to lower premiums for healthy individuals.

| Characteristics | Values |

|---|---|

| Purpose | To provide insurance for individuals deemed "uninsurable" due to pre-existing conditions |

| Participants | Individuals with serious pre-existing conditions who don't have access to health insurance from an employer |

| Impact on Premiums | High-risk pools can help keep premiums lower for those in the conventional market. However, premiums for high-risk pool participants are typically higher. |

| Funding | State funds, enrollee premiums, fees assessed on private health insurance carriers, federal or state general revenues |

| Administration | High-risk pools are typically administered at the state level, but federal rules have reduced variation across states. |

| Benefits | High-risk pools may offer fewer benefit choices, provider options, and insurer choices compared to the individual market. |

| Enrollment Impact | High-risk pools may experience increased volatility in enrollment, with consumers potentially exiting the market if assigned to the high-risk pool, leading to higher uninsurance rates. |

| Applicability | High-risk pools were common before the Affordable Care Act (ACA) mandated that insurers cover people with pre-existing conditions. Now, insurers are prohibited from medical underwriting, making high-risk pools less necessary. |

Explore related products

What You'll Learn

- High-risk pools were the only pre-2014 coverage for those with serious pre-existing conditions

- states established their own high-risk pools, mostly in the 1990s

- The ACA's Pre-Existing Condition Insurance Plan (PCIP) guaranteed health insurance for those with pre-existing conditions

- High-risk pools are separate from the conventional individual market

- High-risk pools are no longer necessary due to the ACA's consumer protections

![]()

High-risk pools were the only pre-2014 coverage for those with serious pre-existing conditions

High-risk pools were the only pre-2014 coverage option for individuals with serious pre-existing conditions who lacked employer-provided or government-provided health insurance (Medicare, Medicaid, CHIP, etc.). Before the Affordable Care Act (ACA) mandated that insurers cover people with pre-existing conditions, high-risk pools, which existed in 35 states starting in the 1970s, provided insurance for some of those deemed \"uninsurable\" by the individual market.

High-risk pools were often underfunded, with expensive coverage and limited plan choices. The ACA's Pre-Existing Condition Insurance Plan (PCIP) was a temporary program established in 2010 to bridge the gap until 2014, when private non-group policies would be available under new market rules prohibiting insurance discrimination based on health status. To qualify for PCIP coverage, individuals had to be uninsured for at least six months and have a pre-existing condition or have been denied coverage.

The ACA's consumer protections have eliminated the need for high-risk pools as applications for individual/family health insurance are no longer denied due to medical history. High-risk pools were funded by enrollee premiums, state funds, fees assessed on private health insurance carriers, and, to a lesser extent, federal grants. The broader the base of funds, the lower the burden on contributing entities. However, high-risk pools were typically separate from the individual market, which could result in fewer benefit choices, provider options, and higher costs.

High-risk pools were intended to protect people with pre-existing conditions, but they required sufficient government funding, which they often lacked. Removing high-cost individuals from the standard risk pool could significantly decrease premiums for healthier individuals while increasing premiums for those in the high-risk pool.

Understanding Commercial Property Insurance Rates

You may want to see also

Explore related products

![]()

35 states established their own high-risk pools, mostly in the 1990s

Before the Affordable Care Act (ACA) mandated insurers to cover people with pre-existing conditions, 35 states had established their own high-risk pools, mostly in the 1990s. These pools provided insurance for those deemed "uninsurable" by individual market insurers due to their health conditions. People with pre-existing conditions have historically faced challenges in obtaining private health coverage and have been costly to insure. High-risk pools were often the only option for those with serious pre-existing conditions who lacked access to employer-provided health insurance.

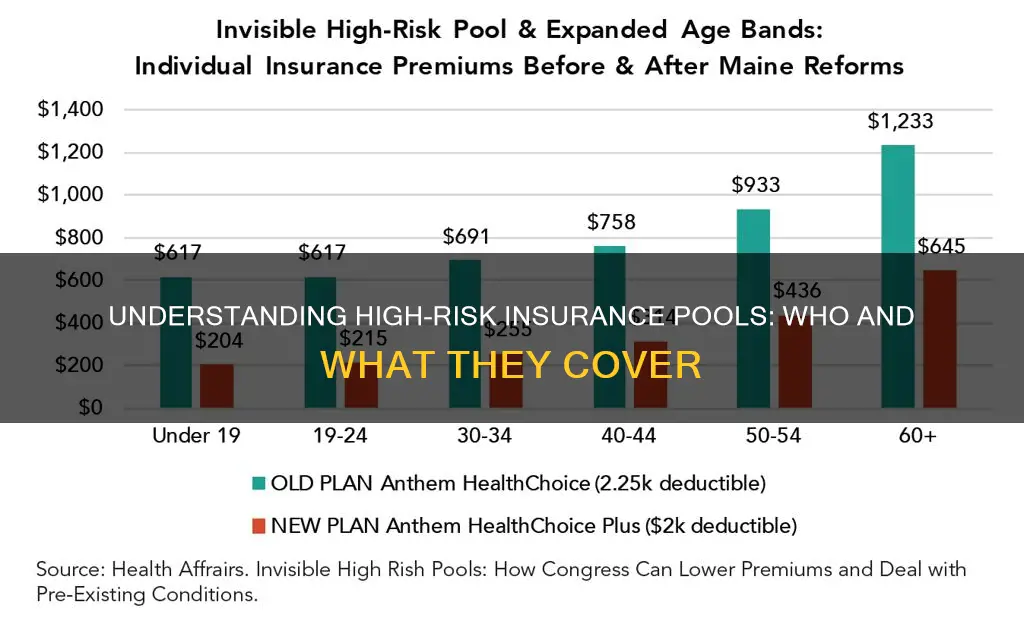

High-risk pools were typically funded by a combination of state funds, enrollee premiums, and fees assessed on private health insurance carriers. However, they were often underfunded, leading to limited coverage options and high costs for enrollees. The premiums in these pools were significantly higher than those paid by healthier individuals, sometimes up to two and a half times more. Additionally, nearly all state high-risk pools excluded coverage of pre-existing conditions, usually for 6-12 months, and many included lifetime or annual limits on coverage.

By segregating high-risk individuals from the conventional individual market, these pools helped keep premiums lower for those in the standard pool. However, the costs for the high-risk pool were substantial, requiring external funding to supplement enrollee premiums. The lack of sufficient government funding for these pools resulted in inadequate coverage or no coverage at all for many enrollees.

Following the enactment of the ACA in 2010, a temporary national high-risk pool, the Pre-Existing Condition Insurance Plan (PCIP), was created to bridge the gap until the new law's insurance market regulations took effect in 2014. With the full implementation of the ACA, high-risk pools became obsolete as insurers were prohibited from medical underwriting, and all policies were required to be guaranteed issue.

Country Music Star: Now an Insurance Salesman

You may want to see also

Explore related products

![]()

The ACA's Pre-Existing Condition Insurance Plan (PCIP) guaranteed health insurance for those with pre-existing conditions

High-risk insurance pools are a form of health insurance coverage for individuals deemed "uninsurable" due to pre-existing conditions. Before the Affordable Care Act (ACA), 35 states established their own high-risk pools, mostly in the 1990s. These pools were often underfunded, offered limited plan choices, and had high costs.

The ACA's Pre-Existing Condition Insurance Plan (PCIP) was designed to bridge the gap until 2014, when the ACA's consumer protections would be fully implemented. The PCIP guaranteed health insurance for those with pre-existing conditions who were uninsured for at least six months, had a pre-existing condition, and were denied coverage or offered inadequate insurance by private insurance companies. The plan was funded by Congress through the Department of Health and Human Services (HHS) and provided coverage to up to 350,000 people.

The ACA mandated that insurers cover people with pre-existing conditions, eliminating the need for high-risk pools. As a result, applications for individual or family health insurance are no longer denied based on medical history, and premiums are not increased due to pre-existing conditions. The ACA's goal was to make health insurance accessible to nearly all Americans, regardless of their health status.

The PCIP ran from 2010 until 2014, when individuals could transition to affordable health insurance plans through the Health Insurance Marketplace, which prohibits discrimination based on pre-existing conditions. The Marketplace offers a competitive environment with a range of health insurance choices, ensuring that individuals with pre-existing conditions have access to affordable and comprehensive coverage.

The ACA provides federal funding to support Pre-Existing Condition Insurance Plans in every state. These plans are designed to offer affordable insurance to Americans living with pre-existing conditions, with premiums based on the standard cost of individual health insurance policies in the respective geographic areas. Out-of-pocket maximums are also limited to $5,950 for individuals and $11,900 for families.

Insurance: Risk Avoidance or Risk Mitigation Strategy?

You may want to see also

Explore related products

![]()

High-risk pools are separate from the conventional individual market

High-risk insurance pools are a way to provide insurance coverage for individuals who are deemed high-risk due to pre-existing medical conditions. These individuals are typically segregated from the conventional individual market risk pool and offered coverage in a separate pool. This separation has several implications for both the high-risk pool and the standard pool.

Firstly, the number of individuals in each pool affects premium rates. Generally, the more people in the high-risk pool, the lower the rates in the standard pool, as the costs of the less healthy are offset by the lower costs of the healthy. This separation can enhance the affordability and enrollment in the standard pool. However, it also drives up the costs of the high-risk pool, necessitating external funding if premiums do not fully cover the higher costs.

Secondly, when high-risk pools are separate, there may be fewer benefit choices, provider options, and insurer choices. Lowering provider payment rates can be a strategy to reduce costs in the high-risk pool. However, providers may be less willing to treat patients if payment rates are significantly lower than in the individual market. This can lead to difficulties in ensuring that high-risk individuals receive adequate care coordination and management, potentially worsening healthcare outcomes and increasing spending.

Additionally, the administrative costs of defining and managing separate risk pools can be significant. The process of calibrating tax credits and addressing challenges to pool assignments can be complex and increase the overall cost of coverage. Furthermore, the potential implementation of separate risk pools can disrupt the market landscape, leading to increased volatility in enrollment as consumers may exit the market if assigned to the high-risk pool.

While separating high-risk individuals from the conventional individual market can help keep premiums lower for those in the standard pool, it also has important consequences. The costs for the high-risk pool are typically higher, and the availability of choices and options may be more limited. These factors must be carefully considered when proposing or implementing separate high-risk pools.

Fidelis: Commercial Insurance and Its Benefits

You may want to see also

Explore related products

![]()

High-risk pools are no longer necessary due to the ACA's consumer protections

High-risk insurance pools were the only coverage option for people with serious pre-existing conditions before the Affordable Care Act (ACA) came into effect in 2014. These pools were often underfunded, with limited plan choices and expensive coverage. 35 states had established their own high-risk pools, mainly in the 1990s, to provide an alternative for those who were denied individual/family health insurance due to medical underwriting.

The ACA aimed to make health insurance accessible to nearly all Americans, regardless of their health status, by prohibiting insurers from medical underwriting. This practice involved screening applicants for pre-existing conditions and either denying them coverage or charging higher premiums. Now, with the ACA, everyone is in a single risk pool, and premiums are based on income rather than health status.

The ACA also included the Pre-Existing Condition Insurance Plan (PCIP), which served as a bridge until 2014, when all policies were required to be guaranteed issue. This plan ensured that individuals with pre-existing conditions could obtain health insurance. As a result, high-risk pools are no longer necessary, as people are no longer denied coverage or charged more due to their medical history.

While some have suggested returning to high-risk pools as a way to lower premiums for healthier individuals, this approach has its drawbacks. High-risk pools were historically underfunded, leading to inadequate coverage for those with pre-existing conditions. Additionally, separating high-risk individuals from the conventional market can result in fewer benefit choices, provider options, and higher costs for those in the high-risk pool.

In conclusion, the consumer protections provided by the ACA have rendered high-risk pools unnecessary. The ACA ensures that all individuals, regardless of their health status, have access to affordable health insurance without the need for separate high-risk pools.

The House Call: When Insurance Adjusters Come Knocking

You may want to see also

Frequently asked questions

High-risk insurance pools are groups of individuals whose medical costs are combined to calculate premiums. In the past, 35 states had high-risk pools for residents who didn't have access to employer coverage or public insurance and were deemed "uninsurable" due to pre-existing conditions.

High-risk insurance pools were created to provide insurance for individuals who were deemed "uninsurable" due to pre-existing conditions. They were often the only coverage available before the Affordable Care Act (ACA) mandated that insurers cover people with pre-existing conditions.

High-risk insurance pools are no longer necessary as the ACA has standardized the individual market and established community rating and federal subsidies. Insurers are now prohibited from medical underwriting, which was the practice of screening people for pre-existing conditions and charging them more or denying them coverage.