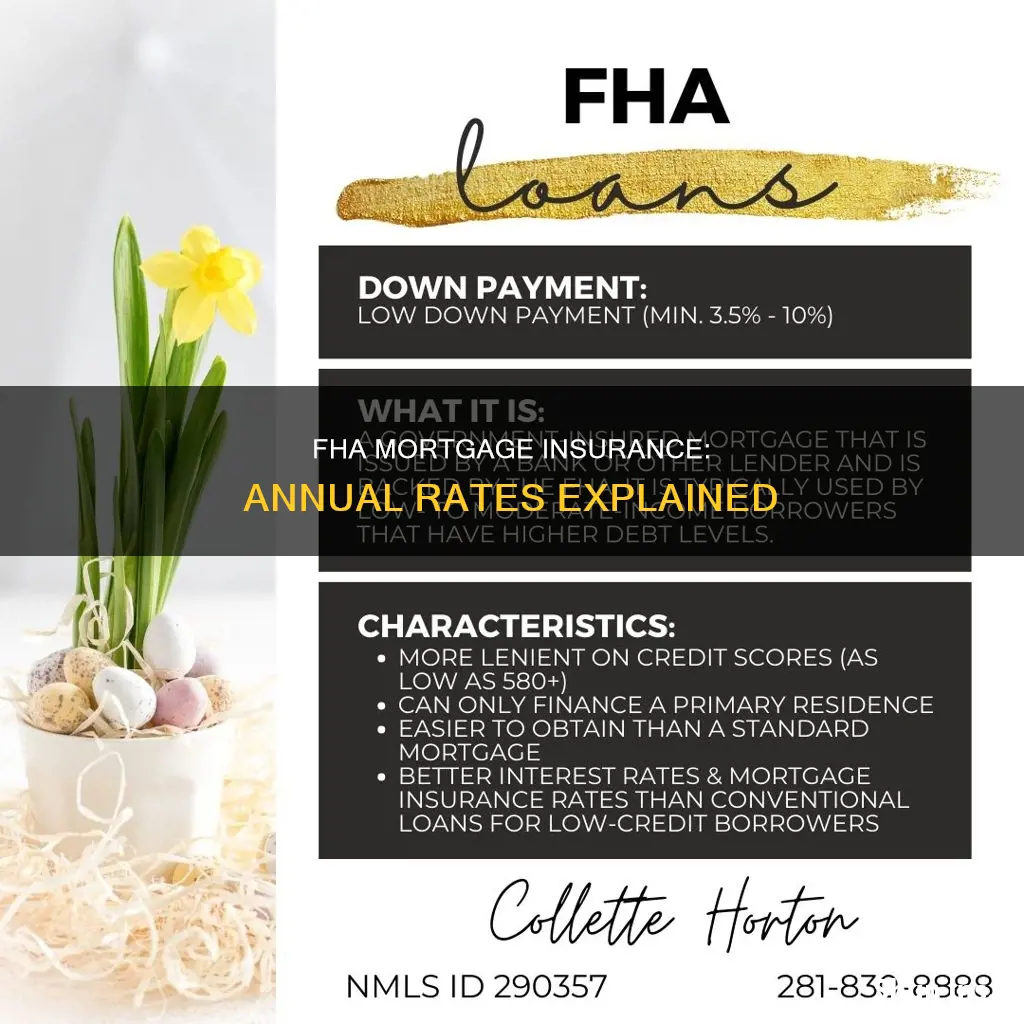

FHA mortgage insurance is a policy that protects lenders against losses that result from defaults on home mortgages. The Federal Housing Administration (FHA) requires both upfront and annual mortgage insurance for all borrowers, regardless of the amount of the down payment. The upfront mortgage insurance premium (UFMIP) is typically 1.75% of the loan amount, while the annual mortgage insurance premium (MIP) ranges between 0.15% to 0.75% of the loan amount. The annual MIP rate varies depending on the size of the down payment and the total loan amount. For example, for a loan amount of $726,200 with a term of more than 15 years, the annual MIP is 0.50%. It's important to note that FHA mortgage insurance is not the only option, and there are other loan types available that do not require mortgage insurance, such as conventional loans and VA loans.

| Characteristics | Values |

|---|---|

| FHA mortgage insurance purpose | Protects lenders against losses that result from defaults on home mortgages |

| FHA mortgage insurance types | Upfront mortgage insurance premium (UFMIP) and annual mortgage insurance premium (MIP) |

| UFMIP rate | 1.75% of the base loan amount |

| Annual MIP range | 0.15% to 0.75% of the loan amount |

| Annual MIP factors | Loan amount, loan term, and loan-to-value (LTV) ratio |

| FHA loan term options | 15 years or 30 years |

| FHA loan limit for a single-family home in most areas | $524,225 |

| FHA loan limit for high-cost areas | Up to $1,209,750 |

| Avoiding FHA mortgage insurance | Opt for conventional loans, VA loans, or USDA loans |

Explore related products

What You'll Learn

![]()

FHA mortgage insurance premium (MIP)

FHA mortgage insurance, also known as FHA MIP, is a type of policy that protects lenders against losses that result from defaults on home mortgages. FHA requires both upfront and annual mortgage insurance for all borrowers, regardless of the amount of down payment. The upfront mortgage insurance premium (UFMIP) is typically 1.75% of the loan amount, while the annual mortgage insurance premium (MIP) ranges between 0.15% to 0.75% of the loan amount.

The annual MIP rate depends on several factors, including the loan amount, loan term, and loan-to-value (LTV) ratio. For example, as of March 20, 2023, loans with an amount less than or equal to $726,200 and an LTV of less than or equal to 90% will have an annual MIP of 50 basis points. On the other hand, loans with an amount greater than $726,200 and an LTV of less than or equal to 90% will have a higher annual MIP.

The annual MIP is typically divided by 12 and charged in monthly installments along with the mortgage payment. It is important to note that FHA mortgage insurance premiums are additional fees that borrowers must pay upfront and over the mortgage term, and they do not protect the borrower but instead safeguard the lender.

One way to avoid paying FHA mortgage insurance is to opt for a different type of home loan, such as a conventional loan, VA loan, or USDA loan. However, each of these alternative loan types has its own set of requirements and fees associated with them. Additionally, refinancing an FHA loan into a conventional loan can help eliminate FHA mortgage insurance premiums, but it may not always be the best option solely for reducing MIP.

Snapshot Technology: Lowering Insurance Rates or a Gimmick?

You may want to see also

Explore related products

![]()

Upfront mortgage insurance premium (UFMIP)

Upfront mortgage insurance, also known as Upfront Mortgage Insurance Premium (UFMIP) or Up-Front Mortgage Insurance (UFMI), is a type of mortgage insurance premium that is collected when the loan is initially made. It is required for borrowers with an FHA loan, in addition to monthly mortgage insurance. The UFMIP is a requirement for FHA home loans and acts as a form of protection for the lender in case the borrower defaults on their mortgage payments.

The upfront mortgage insurance premium is typically financed into the mortgage amount but can also be paid in full in cash upfront. It is important to note that partial cash payments are not allowed. The UFMIP is not refundable, except when refinancing to a new FHA-insured mortgage within three years of the original loan. In certain cases, homeowners may be eligible for a partial UFMIP refund if they meet specific criteria, such as refinancing their FHA loan within five years from the date of closing.

The rate for upfront mortgage insurance is typically set at 1.75% of the base loan price or the purchase price of the home, minus any down payment. For example, if the initial loan amount is $300,000, the UFMIP would be $5,250 (1.75% of $300,000), resulting in a total mortgage amount of $305,250. FHA Streamline refinance loans are charged a lower UFMIP rate of 0.55%.

The UFMIP is just one component of the costs associated with FHA loans. Borrowers should also be aware of the ongoing mortgage insurance premium payments, such as the annual mortgage insurance premium (MIP), which is paid monthly as part of the FHA loan. The MIP can range from 0.45% to 1.05% of the loan amount, depending on various factors, including the down payment amount and loan term.

Insurance Fraud: Deceiving Vehicle Claims

You may want to see also

Explore related products

![]()

Annual mortgage insurance premium (MIP)

The Federal Housing Administration (FHA) requires both upfront and annual mortgage insurance for all borrowers, regardless of the amount of the down payment. The annual mortgage insurance premium (MIP) is an additional fee that all FHA loan borrowers pay over the mortgage term. The cost of the annual MIP ranges between 15 and 75 basis points, which is 0.15% to 0.75% of the loan amount. The average annual MIP rate is 0.55%.

The annual MIP is charged annually, divided by 12, and added to the monthly payment. The cost of FHA mortgage insurance varies based on the LTV ratio. Lenders divide the loan amount by the home's value to determine the LTV ratio. The more you borrow, the higher the LTV ratio. The loan term also determines the cost of the annual MIP. The loan term is the length of time you choose to repay the loan, typically 15 or 30 years for FHA loans.

The annual MIP rate will vary depending on the size of the FHA loan and the down payment. The larger the loan and the smaller the down payment, the higher the annual MIP rate. Most borrowers can expect to pay around 0.55% of the total loan amount in annual MIP. This rate is lower than in previous years, when the typical annual MIP was 0.85%.

FHA annual MIP can be removed in some cases. If the borrower makes a down payment of at least 10%, they can remove the MIP after 11 years. However, if the down payment is less than 10%, the MIP will last for the entire loan term. It is not possible to lower the MIP amount on an existing loan, but refinancing into a conventional loan without PMI may be an option to reduce the MIP.

Statistical Models Powering Auto Insurance Pricing Strategies

You may want to see also

Explore related products

![]()

FHA loans and insurance

FHA loans are insured by the Federal Housing Administration (FHA), which operates under the US Department of Housing and Urban Development (HUD). This insurance protects lenders against losses that may result from borrower defaults on home mortgages.

FHA loans require both upfront and annual mortgage insurance for all borrowers, regardless of the amount of the down payment. The upfront mortgage insurance premium (UFMIP) is typically 1.75% of the base loan amount, although it can be paid in cash or financed into the loan amount. The annual mortgage insurance premium (MIP) varies depending on the loan amount, loan term, and loan-to-value (LTV) ratio. It typically ranges between 0.15% to 0.75% of the loan amount and is paid in monthly installments.

The annual MIP rate for FHA loans has decreased over time. Before March 2023, the typical annual MIP was 0.85%. As of February 2023, the US Department of Housing and Urban Development (HUD) reduced the annual FHA MIP by 30 basis points, resulting in a rate of 0.50% for loans with terms longer than 15 years and a loan amount of $726,200 or less.

It's important to note that FHA mortgage insurance is not the same as private mortgage insurance (PMI) on conventional loans. While PMI is paid to the lender, FHA mortgage insurance is paid to HUD. This insurance allows the FHA to offer loans with lower down payment requirements and more flexible credit criteria, making homeownership more accessible.

Borrowers can avoid paying FHA mortgage insurance by opting for other home loan types, such as conventional loans, VA loans, or USDA loans, each with their own requirements and fees.

Security Systems: Insurance Rates and Peace of Mind

You may want to see also

Explore related products

![]()

Strategies to reduce or eliminate MIP

Mortgage insurance is a policy that protects lenders against losses that result from defaults on home mortgages. The Federal Housing Administration (FHA) requires both upfront and annual mortgage insurance (MIP) for all borrowers, regardless of the amount of the down payment. The upfront mortgage insurance premium (UFMIP) is typically 1.75% of the loan amount, while the annual MIP ranges between 0.15% to 0.75% of the loan amount. This annual MIP is charged monthly.

- Refinance into a Conventional Loan: If you have an FHA loan with MIP, refinancing into a conventional loan is an effective strategy to eliminate MIP. Conventional loans do not require mortgage insurance if you have at least 20% equity in your home. However, if you put down less than 20%, you will have to pay private mortgage insurance (PMI), which can be removed once you reach 20% equity.

- Increase Down Payment: Making a larger down payment of at least 10% can help reduce long-term mortgage costs by automatically removing MIP after 11 years. This is a strategic move as it lowers the overall loan amount and interest paid over time.

- Shorten Loan Term: Opting for a shorter loan term, such as a 15-year mortgage instead of a 30-year mortgage, can result in lower mortgage insurance premiums. This strategy can help you pay off your loan faster and reduce the overall cost of mortgage insurance.

- Build Home Equity: Paying more than the required minimum each month can help you build home equity faster. Once you reach at least 20% equity, you may be able to request the elimination of mortgage insurance premiums, provided you are current on all your payments.

- Alternative Loan Options: Consider alternative loan options that do not require mortgage insurance, such as VA loans for military members, veterans, or their spouses, or USDA loans for purchasing homes in rural areas. However, these loan options may have other fees, such as funding or guarantee fees, so be sure to understand the full cost of the loan.

It is important to carefully consider your financial situation and seek expert advice before making any decisions regarding your mortgage or insurance options.

Creating an Auto Insurance Binder: A Step-by-Step Guide

You may want to see also

Frequently asked questions

FHA mortgage insurance, or mortgage insurance premium (MIP), is an added cost that you’ll need to consider when taking out an FHA loan. It is a policy that protects lenders against losses that result from defaults on home mortgages.

There are two types of FHA loan insurance payable on an FHA loan: the upfront mortgage insurance premium (UFMIP) and the annual mortgage insurance premium (MIP). The upfront MIP rate is 1.75% of the loan amount, while the annual MIP ranges from 0.15% to 0.75% of the loan amount.

The upfront MIP is a one-time payment required at closing or added to the loan balance. The annual MIP is a recurring yearly fee, divided into monthly installments, that continues throughout the loan term or until certain conditions are met.

One way to avoid paying FHA mortgage insurance is to select another home loan type, such as a conventional loan, VA loan, or USDA loan. However, these alternative loan types may have their own fees and requirements.