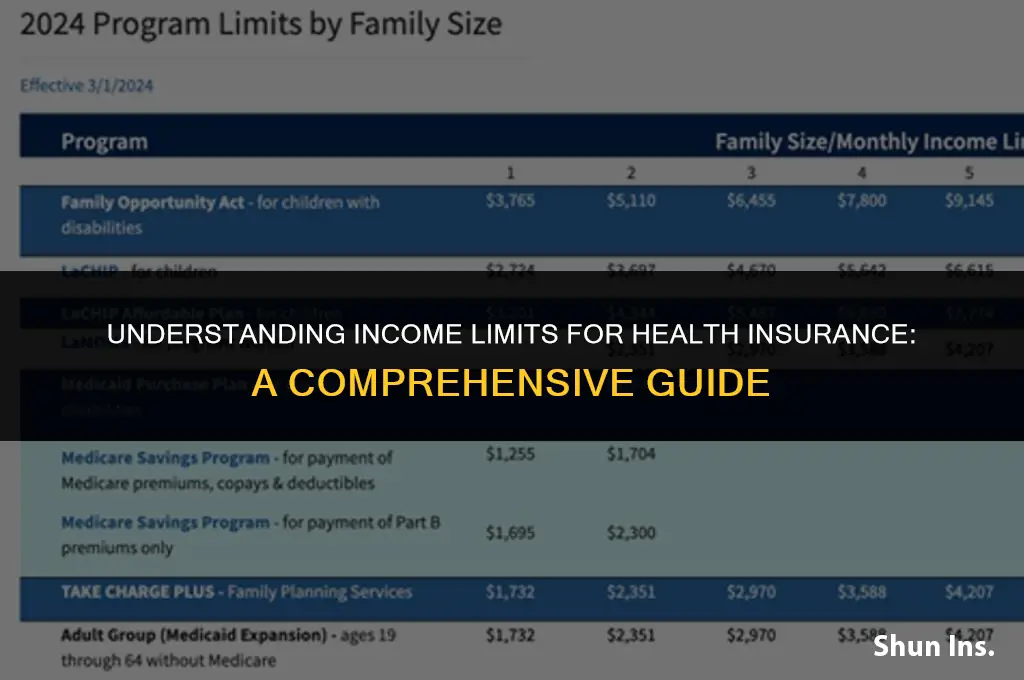

The income limits for health insurance vary depending on the country and the specific insurance program. In general, these limits are set to determine eligibility for subsidized health insurance or Medicaid. For example, in the United States, the income limits are based on the Federal Poverty Level (FPL) and can range from 100% to 400% of the FPL, depending on the state and the size of the household. It's important to check with the relevant health insurance authority or a healthcare provider to understand the specific income limits that apply to your situation.

| Characteristics | Values |

|---|---|

| Income Limit | Varies by state and family size |

| Subsidy Eligibility | Based on income and family size |

| Coverage Options | Private, Medicaid, CHIP, Medicare |

| Enrollment Period | Annual, with special enrollment periods |

| Documentation Required | Proof of income, citizenship, and identity |

| Premium Costs | Depends on income and subsidy eligibility |

| Out-of-Pocket Costs | Varies by plan and income level |

| Network Providers | Depends on insurance plan |

| Pre-Existing Conditions | Covered under most plans |

| Essential Health Benefits | Required under most plans |

What You'll Learn

- Federal Poverty Level (FPL) Guidelines: Income thresholds determining eligibility for Medicaid and subsidized health insurance

- Medicaid Expansion: State-specific income limits for Medicaid eligibility under the Affordable Care Act

- Subsidy Eligibility: Income ranges qualifying for premium tax credits on health insurance marketplaces

- CHIP Income Limits: Eligibility criteria for the Children's Health Insurance Program by state

- Income Verification: Documentation requirements and processes to verify income for health insurance purposes

![]()

Federal Poverty Level (FPL) Guidelines: Income thresholds determining eligibility for Medicaid and subsidized health insurance

The Federal Poverty Level (FPL) Guidelines serve as a critical determinant for eligibility in various health insurance programs, including Medicaid and subsidized health insurance under the Affordable Care Act (ACA). These guidelines are updated annually by the Department of Health and Human Services (HHS) and are based on income thresholds that vary according to family size and composition. Understanding these guidelines is essential for individuals and families seeking to access affordable health care.

For Medicaid eligibility, the FPL Guidelines set the income limits at or below 138% of the federal poverty level for adults and children. This means that a family of four with an annual income of $35,510 or less would qualify for Medicaid benefits. However, it's important to note that Medicaid eligibility also depends on other factors such as residency, citizenship status, and specific state policies, as Medicaid is a jointly funded federal and state program.

In the context of the ACA's health insurance marketplace, the FPL Guidelines are used to determine eligibility for premium tax credits and cost-sharing reductions. Individuals and families with incomes between 100% and 400% of the federal poverty level may qualify for premium tax credits to help offset the cost of health insurance premiums. Additionally, those with incomes below 250% of the FPL may be eligible for cost-sharing reductions, which lower the out-of-pocket costs for deductibles, copayments, and coinsurance.

The FPL Guidelines also play a role in determining eligibility for other health insurance programs and benefits, such as the Children's Health Insurance Program (CHIP) and the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC). CHIP provides health insurance coverage to low-income children who do not qualify for Medicaid, while WIC offers nutrition assistance to pregnant women, breastfeeding women, and infants and children under the age of five who are at nutritional risk.

It's crucial for individuals and families to understand the FPL Guidelines and how they impact eligibility for various health insurance programs. By doing so, they can make informed decisions about their health care options and ensure they are accessing the benefits for which they are eligible. Resources such as the HHS website and local health insurance navigators can provide valuable assistance in navigating the complexities of the FPL Guidelines and health insurance eligibility.

Best Affordable Medical Insurance Options for You

You may want to see also

![]()

Medicaid Expansion: State-specific income limits for Medicaid eligibility under the Affordable Care Act

Under the Affordable Care Act (ACA), Medicaid expansion allows states to extend Medicaid eligibility to many low-income adults, but the specific income limits vary by state. Generally, states that have expanded Medicaid cover adults with incomes up to 138% of the federal poverty level (FPL). However, some states have chosen not to expand Medicaid, leaving a coverage gap for low-income individuals who earn too much to qualify for traditional Medicaid but still cannot afford private insurance.

For those living in states that have expanded Medicaid, the process of determining eligibility involves comparing an individual's modified adjusted gross income (MAGI) to the state's FPL threshold. MAGI is calculated by taking into account the individual's taxable income, as well as certain deductions and exclusions. It's important to note that not all income is counted towards MAGI, such as Supplemental Security Income (SSI) and certain types of disability benefits.

In addition to income, other factors can affect Medicaid eligibility, including family size, age, and disability status. For example, pregnant women and individuals with disabilities may have different eligibility criteria or income limits. Some states also have additional requirements, such as work or job training obligations for certain Medicaid recipients.

Navigating the Medicaid expansion landscape can be complex, as the rules and limits vary significantly from state to state. Individuals seeking Medicaid coverage should consult their state's Medicaid website or contact a local Medicaid office to determine their eligibility and understand the specific income limits and requirements in their area.

North Carolina's Individual Health Insurance Carriers: A Comprehensive Guide

You may want to see also

![]()

Subsidy Eligibility: Income ranges qualifying for premium tax credits on health insurance marketplaces

To determine subsidy eligibility for premium tax credits on health insurance marketplaces, it's essential to understand the income ranges that qualify. These ranges are typically expressed as a percentage of the Federal Poverty Level (FPL), which varies based on household size and income. For instance, a household earning up to 400% of the FPL may be eligible for premium tax credits, but this can differ by state and specific marketplace rules.

Analyzing the FPL is crucial because it sets the benchmark for subsidy eligibility. The FPL is adjusted annually to reflect changes in the cost of living and is used to determine eligibility for various government programs, including health insurance subsidies. For example, in 2023, the FPL for a single individual was $13,590, while for a family of four, it was $27,700. Households earning below these thresholds may qualify for Medicaid or other state-specific programs, whereas those earning above may still be eligible for premium tax credits, depending on the percentage of the FPL they fall into.

When applying for health insurance through a marketplace, individuals must provide detailed income information to determine their subsidy eligibility. This includes wages, salaries, tips, self-employment income, and other sources of income. Additionally, applicants must consider their household size, as this directly impacts the FPL threshold and, consequently, subsidy eligibility. For example, a single individual earning $30,000 may qualify for premium tax credits, but a family of four with the same income may not, due to the higher FPL threshold for larger households.

It's also important to note that subsidy eligibility can change from year to year, based on fluctuations in the FPL and any updates to marketplace rules. Therefore, individuals should regularly review their income and household size to ensure they are still eligible for the appropriate subsidies. Failure to do so could result in paying higher premiums or missing out on available financial assistance.

In conclusion, understanding subsidy eligibility for premium tax credits on health insurance marketplaces requires a clear grasp of the FPL, household size, and income sources. By staying informed about these factors and any changes to marketplace rules, individuals can maximize their chances of receiving the financial assistance they need to afford health insurance.

Top Insurance Companies: Who Offers the Best Rates in 2023?

You may want to see also

![]()

CHIP Income Limits: Eligibility criteria for the Children's Health Insurance Program by state

The Children's Health Insurance Program (CHIP) is a vital initiative aimed at providing health coverage to children from low-income families who may not qualify for Medicaid. Each state administers its own CHIP program, which means eligibility criteria, including income limits, can vary significantly from one state to another. Generally, CHIP is designed to cover children up to age 19, but some states extend coverage to pregnant women and infants.

Income limits for CHIP are typically expressed as a percentage of the Federal Poverty Level (FPL). For instance, a state might set its CHIP income eligibility threshold at 200% of the FPL, meaning families with incomes below this level would qualify for the program. It's important to note that these limits are subject to change and may be adjusted annually based on federal guidelines and state policies.

To determine if a family qualifies for CHIP, they must consider not only their gross income but also the number of people in their household. This is because CHIP uses a sliding scale based on family size to assess eligibility. For example, a family of four with an income of $48,000 might qualify for CHIP in a state with a 200% FPL threshold, whereas a family of two with the same income would not.

Families interested in CHIP should contact their state's health department or visit the official CHIP website to obtain the most current information on income limits and eligibility criteria. Additionally, some states offer online pre-screening tools that can help families determine if they are likely to qualify for CHIP based on their income and other factors.

In conclusion, while CHIP is a federally funded program, its administration and eligibility rules are state-specific. This means that families must be aware of their state's unique CHIP income limits and criteria to determine if they qualify for this important health insurance program.

Understanding Eligibility for Ohio Medical Insurance

You may want to see also

![]()

Income Verification: Documentation requirements and processes to verify income for health insurance purposes

Income verification is a critical step in determining eligibility for health insurance, particularly for programs like Medicaid or subsidized health plans under the Affordable Care Act. The process typically involves providing documentation to prove your income level, which must fall within certain limits to qualify for assistance. Required documents may include pay stubs, tax returns, bank statements, or proof of unemployment benefits. It's essential to gather all necessary paperwork before applying to ensure a smooth verification process.

The specific income limits for health insurance vary depending on the program and your state of residence. For Medicaid, eligibility is often based on the Federal Poverty Level (FPL), with different states offering coverage to individuals earning up to 100% to 200% of the FPL. Subsidized health plans on the health insurance marketplace also use the FPL to determine eligibility for premium tax credits, with subsidies available to those earning up to 400% of the FPL in many cases. Understanding these limits is crucial for determining whether you qualify for financial assistance with your health insurance.

When applying for health insurance, it's important to be aware of common mistakes that can delay or complicate the income verification process. For example, failing to provide all required documentation or submitting incomplete or inaccurate information can lead to delays or even denial of coverage. To avoid these issues, carefully review the application instructions and ensure that all necessary documents are submitted in a timely manner. Additionally, be prepared to provide explanations or additional documentation if requested by the insurance provider.

In some cases, individuals may need to provide additional information or undergo further verification steps if their income situation is complex. This might include scenarios such as self-employment, irregular income, or recent changes in employment status. In these situations, it's important to be proactive in providing any requested information and to communicate openly with the insurance provider to ensure that your application is processed as efficiently as possible.

Overall, understanding the income verification process and being prepared to provide the necessary documentation is key to successfully obtaining health insurance coverage. By familiarizing yourself with the requirements and potential pitfalls, you can help ensure that you receive the coverage you need in a timely manner.

Pet Insurance: Medical Cover for Cats

You may want to see also

Frequently asked questions

The income limits for health insurance vary depending on the specific program and your location. Generally, Medicaid and the Children's Health Insurance Program (CHIP) have income limits based on the Federal Poverty Level (FPL). For example, in many states, Medicaid is available to adults with incomes up to 138% of the FPL.

To determine if you qualify for Medicaid or CHIP, you can use the Federal Poverty Level (FPL) as a guideline. The FPL varies based on your household size and income. You can find the current FPL guidelines on the Department of Health and Human Services (HHS) website. Additionally, you can apply for Medicaid or CHIP through your state's health department or online marketplace, and they will assess your eligibility based on your income and other factors.

Yes, if your income is too high for Medicaid or CHIP, you may be eligible for other health insurance options. You can explore plans through the Health Insurance Marketplace, which offers a range of plans with different premiums and coverage levels. Additionally, you may be able to get health insurance through your employer or purchase a private plan directly from an insurance company. Some states also offer their own health insurance programs for low-income individuals who do not qualify for Medicaid or CHIP.