Subsidized health insurance is a crucial component of many countries' healthcare systems, designed to make health coverage more affordable for low- and middle-income individuals. The income salaries that qualify for subsidized health insurance vary significantly depending on the country and its specific policies. Generally, these subsidies are aimed at those who earn too much to qualify for Medicaid or other free health insurance programs but still cannot afford private insurance. The subsidies often come in the form of tax credits or direct payments to insurance companies, reducing the monthly premium cost for the insured. Eligibility is typically determined by income level relative to the federal poverty line, with different tiers of subsidies available based on income brackets. Understanding these income thresholds is essential for individuals seeking to take advantage of subsidized health insurance options.

| Characteristics | Values |

|---|---|

| Income Level | Varies by state and family size |

| Subsidy Amount | Depends on income and family size |

| Eligibility | Based on income and family size |

| Insurance Type | Private health insurance |

| Coverage | Essential health benefits |

| Enrollment | Through state or federal marketplace |

| Premium Payment | Monthly |

| Deductibles | May apply |

| Co-payments | May apply |

| Out-of-pocket | Limited |

Explore related products

What You'll Learn

- Eligibility Criteria: Income limits and requirements for qualifying for subsidized health insurance

- Premium Subsidies: How subsidies reduce monthly premiums based on income levels

- Cost-Sharing Reductions: Lowering out-of-pocket costs like deductibles and copays for low-income individuals

- Tax Credits: Explanation of tax credits available to help pay for health insurance premiums

- State-Specific Programs: Variations in subsidized health insurance programs across different states

![]()

Eligibility Criteria: Income limits and requirements for qualifying for subsidized health insurance

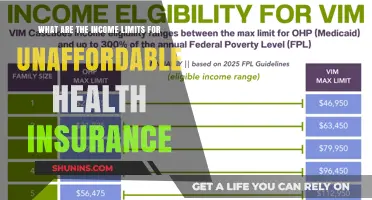

To qualify for subsidized health insurance, individuals must meet specific income criteria. These criteria vary depending on the country or region, but generally, they are designed to ensure that those who earn lower incomes have access to affordable healthcare. In the United States, for example, the Affordable Care Act (ACA) established income limits for eligibility. As of 2023, individuals earning up to 400% of the Federal Poverty Level (FPL) may qualify for subsidies. This translates to an annual income of approximately $51,040 for a single person or $106,080 for a family of four.

However, meeting the income criteria is not the only requirement for subsidized health insurance. Applicants must also demonstrate that they do not have access to employer-sponsored health coverage or other forms of insurance. Additionally, they must be citizens or legal residents of the country or region offering the subsidies. In some cases, there may be additional requirements, such as age limits or health status, but these are less common.

The process of applying for subsidized health insurance typically involves submitting an application through a government-run marketplace or exchange. Applicants will need to provide proof of income, such as tax returns or pay stubs, as well as documentation of their citizenship or residency status. Once approved, individuals can select a health plan from a range of options offered by private insurers. The subsidies are then applied directly to the premiums, reducing the cost of coverage for the individual.

It's important to note that the eligibility criteria for subsidized health insurance can change over time, as governments adjust their policies in response to economic conditions and healthcare needs. As such, it's essential for individuals to stay informed about the latest requirements and deadlines for enrollment. Failure to meet the eligibility criteria may result in the loss of subsidies, leaving individuals responsible for the full cost of their health insurance premiums.

In conclusion, qualifying for subsidized health insurance requires meeting specific income limits and other eligibility criteria. The application process involves providing documentation of income and citizenship status, and selecting a health plan from a range of options. By understanding the requirements and staying informed about policy changes, individuals can ensure they have access to affordable healthcare.

Do Spouses Get Separate Health Insurance Marketplace Statements?

You may want to see also

Explore related products

$23.74 $24.99

$59.91 $64.95

![]()

Premium Subsidies: How subsidies reduce monthly premiums based on income levels

Subsidies play a crucial role in making health insurance more affordable for individuals and families. By reducing monthly premiums based on income levels, subsidies help ensure that health coverage is accessible to a wider range of people, including those who might otherwise struggle to afford it. This financial assistance is particularly important in today's healthcare landscape, where the cost of insurance can be prohibitively high for many.

The way subsidies work is by providing a discount on the monthly premium cost, which is typically based on a percentage of the individual's or family's income. This means that as income increases, the subsidy amount decreases, ensuring that those who need the most assistance receive the most help. Subsidies are often funded by government programs, such as Medicaid and the Children's Health Insurance Program (CHIP), as well as through private insurance companies that offer subsidized plans.

One of the key benefits of premium subsidies is that they help to level the playing field when it comes to accessing healthcare. By reducing the financial burden of insurance premiums, subsidies enable individuals and families to focus on their health and well-being rather than worrying about how they will pay for their coverage. This can lead to better health outcomes, as people are more likely to seek preventive care and treatment when they have affordable access to healthcare services.

In addition to reducing the cost of premiums, subsidies can also help to improve the overall quality of healthcare. When more people have access to affordable insurance, it can lead to a more stable healthcare system, as providers are better able to plan for and manage the needs of their patients. This, in turn, can result in better care coordination, more effective treatment options, and improved patient satisfaction.

Overall, premium subsidies are a vital tool in ensuring that health insurance is accessible and affordable for all. By reducing the financial barriers to coverage, subsidies help to promote better health outcomes, improve the quality of healthcare, and create a more equitable healthcare system for everyone.

Does Foreign Health Insurance Impact Your U.S. Tax Obligations?

You may want to see also

Explore related products

![]()

Cost-Sharing Reductions: Lowering out-of-pocket costs like deductibles and copays for low-income individuals

Cost-sharing reductions are a crucial component of making health insurance more affordable for low-income individuals. These reductions lower the out-of-pocket costs that insured individuals must pay, such as deductibles, copays, and coinsurance. By doing so, they help to ensure that health care is more accessible to those who need it most.

One of the key aspects of cost-sharing reductions is that they are typically tied to the individual's income level. This means that the lower an individual's income, the greater the reduction in their out-of-pocket costs. For example, an individual earning 150% of the federal poverty level may be eligible for a significant reduction in their deductible, while someone earning 200% of the poverty level may receive a smaller reduction.

It's important to note that cost-sharing reductions are not the same as premium subsidies, which help to lower the monthly cost of health insurance. While premium subsidies are also based on income level, they do not directly reduce the out-of-pocket costs associated with health care. Cost-sharing reductions, on the other hand, are designed to make health care more affordable at the point of service.

To be eligible for cost-sharing reductions, individuals must typically enroll in a health insurance plan through a state or federal marketplace. These reductions are often applied automatically, based on the individual's reported income. However, it's important for individuals to understand their eligibility and to choose a plan that offers the best possible cost-sharing reductions for their specific needs.

In conclusion, cost-sharing reductions play a vital role in making health insurance more affordable for low-income individuals. By lowering out-of-pocket costs, these reductions help to ensure that health care is more accessible and that individuals are better able to manage their health care expenses.

Adding Your Step Son to Your Medical Insurance

You may want to see also

Explore related products

![]()

Tax Credits: Explanation of tax credits available to help pay for health insurance premiums

Tax credits are a vital component of the Affordable Care Act (ACA), designed to make health insurance more affordable for lower-income individuals and families. These credits are applied directly to your monthly premiums, reducing the amount you pay out-of-pocket each month. The size of the tax credit you receive depends on your income, the number of people in your household, and the cost of health insurance in your area.

To qualify for tax credits, you must meet certain criteria. First, you must be a U.S. citizen or lawfully present in the United States. Second, you must not be eligible for Medicaid or Medicare. Third, your income must fall within a specific range – generally between 100% and 400% of the Federal Poverty Level (FPL). For a family of four, this would translate to an annual income between $26,500 and $106,000 as of 2023.

The tax credit amount is calculated based on a sliding scale. Those with lower incomes receive larger credits, while those with higher incomes within the eligible range receive smaller credits. For example, if your income is at 150% of the FPL, you may receive a tax credit that covers up to 90% of your monthly premium. However, if your income is closer to 400% of the FPL, your tax credit might only cover 20% of your premium.

Applying for tax credits is done through the health insurance marketplace. When you fill out your application, you'll need to provide information about your income, household size, and other relevant details. The marketplace will then determine your eligibility and the amount of tax credit you qualify for. It's important to note that tax credits are only available for plans purchased through the marketplace, not for plans bought directly from an insurance company or through an employer.

One key aspect to keep in mind is that tax credits are reconciled at tax time. This means that you'll need to report the tax credit amount you received on your federal income tax return. If you received more in tax credits than you were eligible for based on your actual income for the year, you may have to repay some or all of the excess credit. Conversely, if you received less in tax credits than you were eligible for, you may be able to claim the additional amount on your tax return.

Understanding tax credits is crucial for making informed decisions about your health insurance. By knowing how tax credits work and how they impact your premium costs, you can choose a plan that best fits your needs and budget.

Why Insurance Companies Require Mortgage Lenders to Endorse Claim Checks

You may want to see also

![]()

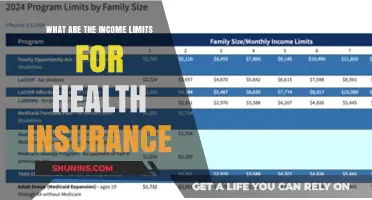

State-Specific Programs: Variations in subsidized health insurance programs across different states

Subsidized health insurance programs vary significantly across different states, reflecting the unique healthcare needs and economic conditions of each region. While the Affordable Care Act (ACA) provides a federal framework for health insurance subsidies, states have considerable leeway in implementing their own programs. This flexibility allows states to tailor their subsidized health insurance offerings to better meet the needs of their residents.

One notable example of state-specific variation is the expansion of Medicaid under the ACA. While some states have embraced Medicaid expansion, providing comprehensive health coverage to low-income individuals, others have opted out, leaving a significant gap in healthcare access for their most vulnerable populations. This decision has far-reaching implications for the availability and affordability of health insurance in these states.

In addition to Medicaid expansion, states have also implemented their own unique health insurance programs. For instance, some states have established state-run health insurance exchanges, while others have opted for federal-state partnerships or federally facilitated exchanges. These differences in exchange models can impact the types of health plans available, the level of competition among insurers, and ultimately, the affordability of health insurance for consumers.

Furthermore, states have varying eligibility criteria for subsidized health insurance programs. While federal guidelines set a general framework for eligibility based on income and family size, states can adjust these criteria to better align with their specific healthcare needs and resources. This can result in differences in who qualifies for subsidized health insurance from state to state, potentially affecting the overall accessibility of these programs.

The variation in state-specific programs also extends to the types of health coverage offered. Some states may prioritize comprehensive health plans that cover a wide range of services, while others may focus on more limited or specialized coverage options. This can impact the overall quality of care available to residents, as well as the financial burden of healthcare costs.

In conclusion, the landscape of subsidized health insurance programs is complex and varied across different states. Understanding these variations is crucial for policymakers, healthcare providers, and consumers alike, as they navigate the intricacies of the healthcare system and work towards improving access to affordable, high-quality health coverage for all.

Personal Injury Protection: Medical Products Covered by PIP Insurance

You may want to see also

Frequently asked questions

The income range for subsidized health insurance varies by state and family size, but generally, it is available for individuals and families with incomes between 100% and 400% of the Federal Poverty Level (FPL).

Health insurance subsidies are calculated based on your income, family size, and the cost of health insurance in your area. The subsidy amount is determined by the difference between the cost of a benchmark plan and what you can afford to pay.

Yes, self-employed individuals can qualify for subsidized health insurance if their income falls within the eligible range and they meet other criteria, such as not being eligible for employer-sponsored health insurance.

If your income changes during the year, you may need to update your information with the health insurance marketplace. Depending on the change, you might receive a different subsidy amount or become ineligible for subsidies.

Yes, under the Affordable Care Act, you cannot be denied health insurance or charged more due to a pre-existing condition. Subsidies are based on income and other factors, not health status.