The new health insurance rules, effective from January 1st, 2024, introduce significant changes aimed at improving coverage and reducing costs for policyholders. These updates include expanded eligibility for subsidies, increased coverage for preventive care, and new provisions for individuals with pre-existing conditions. Additionally, the rules streamline the enrollment process and enhance transparency in billing. This paragraph provides a concise overview of the key changes, highlighting their potential impact on healthcare accessibility and affordability.

| Characteristics | Values |

|---|---|

| Effective Date | January 1, 2024 |

| Coverage Expansion | Includes dental and vision care for adults |

| Premium Subsidies | Increased subsidies for low-income individuals |

| Network Changes | Expanded network of healthcare providers |

| Telehealth Services | Enhanced coverage for telehealth consultations |

| Prescription Drug Coverage | Improved coverage for specialty medications |

| Wellness Programs | Incentives for participating in wellness initiatives |

| Appeals Process | Streamlined process for appealing denied claims |

| Mental Health Services | Increased access to mental health professionals |

| Dependent Coverage | Extended coverage for dependents up to age 26 |

Explore related products

What You'll Learn

- Eligibility Expansion: New rules may broaden eligibility criteria, allowing more individuals to qualify for health insurance

- Coverage Enhancements: Updates could include additional covered services, such as mental health, dental, or vision care

- Premium Changes: Revisions might affect premium costs, potentially introducing subsidies or increasing rates based on new risk assessments

- Network Adjustments: Insurers may update their provider networks, impacting which doctors and hospitals are considered in-network

- Appeals Process: New regulations could streamline or modify the appeals process for denied claims, enhancing consumer protections

![]()

Eligibility Expansion: New rules may broaden eligibility criteria, allowing more individuals to qualify for health insurance

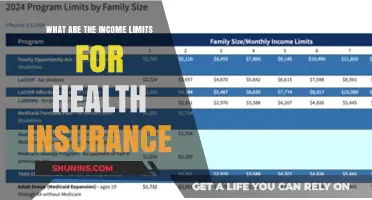

The recent changes in health insurance regulations have brought about a significant shift in eligibility criteria, potentially opening up access to healthcare for a larger segment of the population. Under the new rules, individuals who previously fell just outside the eligibility brackets may now find themselves covered. This expansion is particularly noteworthy as it addresses some of the longstanding gaps in the healthcare system, ensuring that more people can access essential medical services.

One of the key aspects of this eligibility expansion is the broadening of income thresholds. Previously, many individuals were excluded from health insurance programs because their income exceeded certain limits, albeit by a small margin. The new rules have adjusted these thresholds, allowing people with slightly higher incomes to qualify for coverage. This change is expected to benefit working families and individuals who, despite having steady employment, struggled to afford health insurance.

Another important facet of the eligibility expansion is the inclusion of additional criteria beyond just income. For instance, some programs now consider factors such as family size, age, and health status when determining eligibility. This more holistic approach ensures that coverage is extended to those who need it most, regardless of their income level. Furthermore, the new rules may also provide for retroactive coverage in certain cases, ensuring that individuals who were previously denied access to healthcare can now receive the necessary medical attention.

The implementation of these new rules is likely to have a profound impact on public health outcomes. By increasing the number of insured individuals, the healthcare system can better address preventive care, chronic disease management, and emergency medical needs. This, in turn, can lead to a reduction in overall healthcare costs, as early intervention and regular check-ups can help prevent more serious and expensive health issues down the line.

However, it is important to note that the eligibility expansion may also come with certain challenges. For example, the increased demand for healthcare services could put a strain on existing resources, potentially leading to longer wait times and difficulties in accessing certain medical professionals. Additionally, the administrative burden of managing the expanded eligibility criteria may require additional staff and training, which could pose logistical challenges for healthcare providers.

In conclusion, the expansion of eligibility criteria under the new health insurance rules represents a significant step forward in ensuring that more individuals have access to essential healthcare services. While there may be challenges associated with this change, the potential benefits in terms of improved public health outcomes and reduced healthcare costs make it a worthwhile endeavor. As the healthcare system continues to evolve, it will be important to monitor the impact of these new rules and make adjustments as necessary to ensure that they are effectively meeting the needs of the population.

Congress Members' Medical Insurance: Understanding Deductibles

You may want to see also

Explore related products

![]()

Coverage Enhancements: Updates could include additional covered services, such as mental health, dental, or vision care

The recent updates to health insurance rules have brought about significant coverage enhancements, particularly in the realm of mental health, dental, and vision care. These additions reflect a growing recognition of the importance of comprehensive healthcare, addressing not just physical ailments but also mental well-being and essential dental and vision needs.

One of the key updates is the inclusion of mental health services as a covered benefit. This expansion ensures that individuals have access to crucial mental health treatments, such as therapy sessions, counseling, and psychiatric evaluations. The coverage extends to various mental health conditions, including anxiety, depression, and substance abuse disorders, thereby promoting overall mental wellness and reducing the stigma associated with seeking help.

In addition to mental health, dental care has also seen notable enhancements. The new rules now cover a range of dental services, from routine check-ups and cleanings to more complex procedures like fillings, extractions, and even orthodontic treatments. This inclusion is particularly beneficial for individuals who may have previously struggled to afford dental care, as it helps prevent more serious oral health issues down the line.

Vision care is another area that has received a boost under the updated health insurance rules. Coverage now includes eye exams, prescription glasses, and contact lenses, making it easier for individuals to maintain good eye health and address any vision problems early on. This enhancement is especially important for those with chronic eye conditions or those who require regular vision corrections.

These coverage enhancements not only improve access to essential healthcare services but also contribute to a more holistic approach to health. By addressing mental, dental, and vision health alongside traditional medical care, the new health insurance rules aim to provide a more comprehensive and inclusive healthcare experience for all individuals.

Understanding Insurance Claim Denials: Navigating the Medical Maze

You may want to see also

Explore related products

![]()

Premium Changes: Revisions might affect premium costs, potentially introducing subsidies or increasing rates based on new risk assessments

The recent revisions to health insurance rules have brought about significant changes to premium costs. Insurers are now reassessing risk factors, which could lead to either subsidies or increased rates for policyholders. This shift is aimed at creating a more equitable system where premiums better reflect individual health risks and needs.

One of the key changes is the introduction of new risk assessment models. These models take into account a wider range of factors, including lifestyle choices, medical history, and even genetic predispositions. As a result, some individuals may see their premiums decrease if they are deemed to be at lower risk, while others may face higher costs if they are considered to be at greater risk.

Another important aspect of these revisions is the potential for subsidies. Insurers may now offer financial assistance to policyholders who are struggling to afford their premiums. This could be in the form of direct discounts or tax credits. The goal is to ensure that everyone has access to affordable health care, regardless of their financial situation.

However, these changes are not without controversy. Some critics argue that the new risk assessments could lead to discrimination against certain groups, such as those with pre-existing conditions. There are also concerns that the subsidies may not be sufficient to offset the increased costs for some policyholders.

Despite these challenges, the revisions are a step towards a more personalized and fair health insurance system. By taking into account individual risk factors and offering subsidies, insurers are working to create a system that is more responsive to the needs of their policyholders.

Top Insurance Companies for First-Time Drivers: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Network Adjustments: Insurers may update their provider networks, impacting which doctors and hospitals are considered in-network

Insurers frequently update their provider networks, which can significantly impact policyholders. These updates may include adding or removing healthcare providers, altering the status of certain facilities from in-network to out-of-network, or vice versa. Such changes can affect the continuity of care for patients, potentially requiring them to seek new providers or pay higher out-of-pocket costs for services previously covered.

The reasons behind these network adjustments are multifaceted. Insurers may renegotiate contracts with providers to control costs, improve the quality of care, or expand access to specialized services. Additionally, providers may choose to leave a network due to financial disagreements or to focus on other patient populations. These dynamics can lead to a shifting landscape of in-network options for insured individuals.

Policyholders should stay informed about network changes to avoid unexpected costs or disruptions in care. Insurers are typically required to notify policyholders of significant network updates, often through mail or email. It is crucial for individuals to review these notifications carefully and contact their insurer with any questions or concerns. Furthermore, policyholders may need to coordinate with their current providers to ensure a smooth transition if they are affected by network changes.

To mitigate the impact of network adjustments, some insurers offer transitional periods during which policyholders can continue to see their current providers at in-network rates, even if they are scheduled to be removed from the network. This grace period allows individuals time to find new providers or appeal network decisions. Additionally, insurers may provide resources to help policyholders navigate network changes, such as online provider directories or customer service hotlines.

In conclusion, network adjustments are a common aspect of health insurance that can have significant implications for policyholders. By staying informed and proactive, individuals can better manage these changes and maintain access to quality healthcare services.

Using Insurance Cards for Medical Care in Europe

You may want to see also

Explore related products

![]()

Appeals Process: New regulations could streamline or modify the appeals process for denied claims, enhancing consumer protections

Under the new health insurance regulations, the appeals process for denied claims is set to undergo significant changes. These modifications aim to streamline procedures and enhance consumer protections, ensuring that individuals have a clearer and more efficient path to challenge decisions made by their insurance providers.

One key aspect of these changes is the introduction of a more transparent review process. Insurers will now be required to provide detailed explanations for claim denials, including the specific reasons and criteria used to reach their decision. This increased transparency will empower consumers to better understand why their claims were denied and what steps they can take to appeal.

Additionally, the new regulations will establish stricter timelines for the appeals process. Insurers will have a limited window to respond to appeals, and failure to do so within the specified timeframe may result in the claim being automatically approved. This measure is designed to prevent insurers from dragging out the appeals process unnecessarily, thereby reducing the financial and emotional burden on consumers.

Another important change is the expansion of the appeals process to include external review options. In cases where the insurer's internal review does not result in a satisfactory outcome for the consumer, they will now have the right to request an independent external review. This external review will be conducted by a third-party organization, providing an unbiased assessment of the claim and ensuring that consumers have a fair chance of having their appeals heard.

Furthermore, the new regulations will require insurers to establish clear and accessible appeals procedures. This includes providing consumers with easily understandable information about the appeals process, as well as ensuring that the necessary forms and documentation are readily available. By making the appeals process more user-friendly, these regulations aim to reduce the barriers that consumers may face when challenging denied claims.

Overall, these changes to the appeals process represent a significant step forward in enhancing consumer protections within the health insurance industry. By increasing transparency, establishing stricter timelines, expanding external review options, and improving accessibility, the new regulations will provide consumers with a more robust and effective means of challenging denied claims.

Does Health Net Insurance Cover Therapy? A Comprehensive Guide

You may want to see also

Frequently asked questions

Under the new health insurance rules, insurance companies are prohibited from denying coverage or charging higher premiums based on pre-existing conditions. This ensures that individuals with prior health issues have equal access to affordable health insurance.

The new health insurance rules allow young adults to stay on their parents' health insurance plans until they are 26 years old. This provision helps young adults who are still in school or starting their careers to maintain health coverage without having to purchase their own plans.

Under the new health insurance rules, preventive care services such as annual check-ups, vaccinations, and screenings for various health conditions are covered without any out-of-pocket costs. This encourages individuals to seek preventive care, which can help detect and manage health issues early on.

The new health insurance rules include provisions to close the prescription drug coverage gap, often referred to as the "donut hole." This means that individuals on Medicare Part D plans will receive better coverage for their prescription medications, reducing their out-of-pocket expenses.