Insurance is a way to protect oneself or one's organization from unforeseen events that may cause potential harm. There are several types of risks in insurance, and they can be broadly categorized into three levels: pure risk, speculative risk, and non-financial risk. Pure risk, also known as absolute risk, carries the potential for loss or, at best, breaking even, but has no possibility of gain. Speculative risk, on the other hand, involves the potential for either a gain or a loss, such as in business ventures or gambling transactions. Non-financial risks are those that cannot be measured in monetary terms and often involve personal choices. Additionally, insurance companies often classify risks into groups with similar characteristics to determine the risk associated with underwriting a new policy and the premium charged. These risk classes can vary but typically include preferred, standard, and substandard categories.

| Characteristics | Values |

|---|---|

| Risk types | Pure risk, speculative risk, fundamental risk, particular risk, financial risk, non-financial risk |

| Pure risk | Natural events, accidents, personal risks, property risks, liability risks |

| Speculative risk | Business ventures, gambling transactions |

| Fundamental risk | Natural disasters, floods, earthquakes, hurricanes, droughts |

| Particular risk | Individual or group behaviour, carelessness, failure to maintain |

| Financial risk | Damage to property, vehicle accidents |

| Non-financial risk | Choosing the wrong car, the wrong spouse, the wrong menu item at a restaurant, the wrong career |

| Risk classes | Super preferred, preferred, standard, substandard, preferred plus, standard plus |

| Preferred risk classes | Healthy individuals, no serious health issues, no medication for chronic conditions, no family history of early-onset diseases, healthy height-weight ratio, normal levels of cholesterol and blood pressure |

| Standard risk classes | Average health and life expectancy |

| Substandard risk classes | High-risk individuals |

| Risk factors | Age, health, lifestyle, driving record, risky hobbies, dangerous behaviours, occupation, health and lifestyle questions, blood and urine samples |

Explore related products

What You'll Learn

![]()

Pure risk vs speculative risk

Pure risk and speculative risk are two distinct categories of risk that are relevant to the insurance industry. Pure risk refers to situations where the only possible outcome is a loss. These types of risks are typically beyond human control and are not voluntarily taken on. Examples of pure risk include natural disasters, fires, accidents, and untimely deaths. Pure risks are commonly insurable through liability, commercial, or personal insurance policies, allowing individuals and businesses to transfer the financial burden to an insurer.

On the other hand, speculative risk involves situations where there is uncertainty regarding the outcome, which could result in either a gain or a loss. Speculative risks are generally made as conscious choices and are not solely due to uncontrollable circumstances. Examples of speculative risk include investing in stocks, buying junk bonds, and sports betting. These types of risks are typically handled by the capital markets rather than insurance companies, as they lack the core elements of insurability.

The distinction between pure risk and speculative risk is important in the insurance industry. Pure risks, with their definite potential for loss, can be more easily assessed and priced by insurers. The likelihood of a loss occurring and the potential financial impact can be estimated using statistical analysis and historical data. This allows insurance companies to determine the appropriate premium amounts to charge their customers.

In contrast, speculative risks are more challenging to insure as they involve the possibility of gain. Speculative risks are often associated with financial investments, where the outcome is uncertain and can vary significantly. While speculative risks may result in substantial gains, they can also lead to significant losses. As such, insurance companies typically do not offer coverage for speculative risks, as it becomes difficult to accurately assess and price these risks.

It is worth noting that the boundary between the insurance industry and capital markets in managing risks is becoming increasingly blurred. Insurance products are increasingly using capital market approaches to hedge the pure risks they assume, and insurance companies are expanding into areas that were traditionally handled by capital markets. Additionally, when a company provides insurance against a pure risk, it takes on a speculative risk by trying to ensure that the customer doesn't experience a loss until after the company has profited from the risk transfer.

Insurance Gain: An Asset or Not?

You may want to see also

Explore related products

![]()

Fundamental risk

While fundamental risks are beyond human control, there are measures that individuals and communities can take to mitigate their impact. For instance, in areas prone to earthquakes, building codes and structural reinforcement can help minimize damage to properties. Similarly, flood defences and early warning systems can reduce the impact of flooding on communities. These measures not only protect against physical damage but also help reduce the financial losses associated with these events.

Insurance companies assess the risk associated with fundamental events using statistical analysis and historical data. They consider the likelihood of these events occurring and the potential magnitude of their impact. Based on this assessment, insurance providers determine the premium costs for coverage against fundamental risks. Higher-risk areas or individuals with a higher risk profile will generally be subject to higher premium costs.

It is worth noting that while fundamental risks are insurable, there may be limitations to the coverage provided. For example, flood insurance typically does not cover certain types of damage, such as mould, outdoor property, or temporary housing. Similarly, standard auto insurance may not cover vehicle damage caused by flooding, requiring comprehensive coverage for such incidents. Therefore, it is essential for individuals to carefully review their insurance policies and understand the specific risks that are covered.

Root Insurance: Saving Money or Not?

You may want to see also

Explore related products

![]()

Particular risk

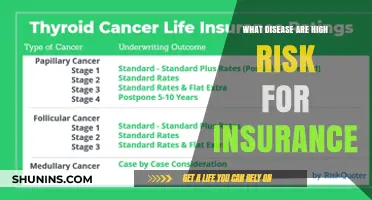

Insurers use risk classes to determine the amount of coverage needed and the cost of that coverage. Riskier risk groups will pay higher premiums. For example, people who are older, have a poor driving record, or engage in risky hobbies or behaviours, such as substance abuse, will pay higher premiums. When applying for life insurance, the answers provided to health and lifestyle questions are considered by the insurer to determine the applicant's risk class and quote.

Who's the Actor in Farmers Insurance Ads?

You may want to see also

Explore related products

![]()

Financial risk

In the context of insurance, financial risk is a crucial consideration for both individuals and insurance companies. For individuals, financial risk influences their decision to purchase insurance and the type of coverage they require. People who are more willing to take financial risks tend to purchase more insurance. This could be because they want to protect themselves from potential financial losses or because they are comfortable with the idea of transferring risk to an insurer. On the other hand, those who are more risk-averse may prefer to self-insure or opt for lower levels of coverage.

When applying for insurance, individuals are assessed based on specific criteria to determine their financial risk profile. This includes factors such as age, health status, lifestyle choices, driving record, and occupation. These factors help insurers calculate the likelihood of a claim being made and subsequently influence the premium costs. For example, a young and healthy individual with a clean driving record is likely to be offered lower premiums on their life and auto insurance policies compared to older individuals with pre-existing health conditions or a history of accidents.

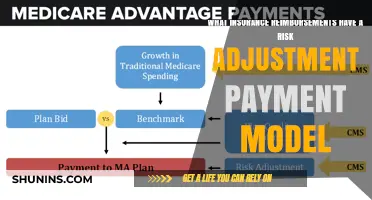

Insurance companies also face financial risk when underwriting policies. They must accurately assess the risk associated with each policyholder to ensure profitability. Insurers use risk classes to group individuals with similar characteristics, enabling them to estimate the chances of a claim being filed. Riskier risk groups, such as those with health issues, advanced age, or a history of accidents, will generally pay higher premiums to compensate for the increased financial risk undertaken by the insurer. Additionally, insurers primarily cover pure risks, which carry the potential for loss without the possibility of gain. Speculative risks, such as gambling or investing, are typically not insured due to their unpredictable nature.

How Insurance Companies Profit from the Sick

You may want to see also

Explore related products

![]()

Risk classes

There are several types of risk classes. The most common risk classifications fall into three groups: preferred, standard, and substandard. Preferred classes are reserved for the healthiest individuals and offer the best pricing. Standard risk classes are for people with average health and life expectancy. Substandard classes are for high-risk individuals. Within these broad categories, there are more nuanced classifications. For example, within the preferred category, there is Preferred Plus, for individuals healthier than the average person of their age and gender, and below that, there is simply Preferred, for individuals who are still in great health but may have some minor health concerns. Standard Plus is for individuals with above-average health conditions but who may be out of range in some health metrics, such as having a higher BMI. They often pay higher premiums than those in the Preferred category. Finally, the standard category is for individuals of average health.

In the case of auto insurance, an insurer may examine the age of the vehicle, the age of the driver, the driver’s history, the amount of coverage requested, and the area in which the vehicle is operated. These factors create a profile of a specific type of driver, which can be used to determine how drivers in this profile act and the amount of coverage needed, as well as how much that coverage should cost.

Pure risk, also referred to as absolute risk, is the potential for a loss to occur without any corresponding potential for gain. Speculative risk, on the other hand, is the potential for either a gain or a loss to occur, such as in gambling or investing. Most insurance providers only cover pure risks, as speculative risks lack the core elements of insurability. Pure risks can be divided into three categories: personal risks that affect the income-earning power of the insured person, property risks, and liability risks that cover losses resulting from social interactions.

Unraveling the Mystery: Do Insurance Adjusters Scrutinize Receipts?

You may want to see also