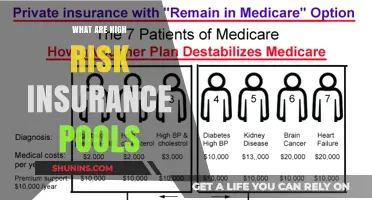

When applying for insurance, an applicant's medical history is one of the first things that insurers consider. Certain medical conditions may lead insurers to consider an applicant high-risk, which can make it difficult to qualify for a policy or result in significantly higher premiums. While the implementation of the Affordable Care Act (ACA) has made health insurance more accessible to Americans with pre-existing conditions, high-risk applicants may still face challenges in obtaining coverage. Some common conditions that can lead to high-risk categorization include cancer, heart disease, kidney disease, diabetes, mental health conditions, and engaging in hazardous hobbies.

Explore related products

What You'll Learn

![]()

Cancer

When applying for insurance, one of the first things that insurers will consider is your medical risk. They will typically ask for a health history, a list of current prescriptions, and sometimes a brief medical exam or medical records. If you have certain conditions, you are likely to be considered high-risk and may be charged higher premiums or even denied coverage.

In the context of life insurance, a cancer diagnosis can affect your insurability and premiums. Many insurers will postpone offering coverage until you have been cancer-free for a set number of years. This is because a history of cancer indicates a higher risk of future health issues, which poses additional financial risk to the insurance company.

Additionally, certain types of cancer may be excluded from coverage, such as non-melanoma skin cancer in some cancer insurance policies. Cancer insurance is a supplemental form of insurance that can provide financial security and peace of mind in the event of a cancer diagnosis. It can help cover the costs of specialized cancer centres and health providers, ensuring that you and your loved ones are not financially strained during treatment.

It's important to carefully read the policy to understand what is and isn't covered. Some providers may not offer coverage if your cancer diagnosis occurred before applying for the policy or if you've had cancer in the past. Cancer insurance is particularly relevant considering the high prevalence of cancer; according to the National Cancer Institute, one in two men and one in three women in the US are at risk of developing cancer during their lifetime.

Furthermore, certain lifestyle choices and occupations can increase the risk of cancer. For example, smoking and exposure to chemicals or toxins in the workplace have been linked to higher cancer risks. In such cases, cancer insurance can provide added protection and peace of mind.

The Confidential Conundrum: Navigating the Privilege of Insurance Adjuster Log Notes

You may want to see also

Explore related products

$16.99

![]()

Heart disease

When it comes to insurance, heart disease is considered a high-risk condition. This includes congenital heart disease, which refers to heart defects that are present at birth. People with congenital heart disease may face challenges in obtaining adequate insurance coverage, especially as they transition to adulthood and can no longer be covered by their parents' insurance plans.

Young adults with congenital heart conditions can usually purchase life insurance, but they may face higher costs. Term life insurance, especially when obtained through an employer, can be a more affordable option and typically requires less medical information. It is recommended to compare policies from different companies, as their considerations of congenital heart disease can vary significantly. Reapplying for life insurance as an adolescent or adult may also increase the chances of approval, as the severity of the condition can be assessed with greater certainty.

For those with heart disease or conditions that increase the risk of heart disease, such as high blood pressure or high cholesterol, health insurance plans cannot deny coverage, charge higher premiums, or impose annual or lifetime dollar limits on benefits due to these factors. This is a protection provided by the Affordable Care Act, which aims to make health insurance accessible to nearly all Americans, regardless of pre-existing conditions. However, it's important to review the details of your specific health plan, as large employers are not required to offer essential health benefits, although most do.

Medicare and Medicaid offer special programs for home monitoring of blood pressure and other heart risks, and they also have out-of-pocket maximums that limit the amount you pay out of your own pocket. Additionally, if you're buying insurance through your state's Marketplace, you may be eligible for financial assistance or tax credits to lower your insurance premiums. These options can help make insurance more affordable for individuals with heart disease.

In summary, while heart disease is considered a high-risk condition by insurers, there are options available to obtain coverage. Comparing policies, taking advantage of employer-provided insurance, and utilizing the protections and financial assistance offered by the Affordable Care Act can help individuals with heart disease secure the insurance they need.

Vacancy Provisions: Builders Risk Insurance Explained

You may want to see also

Explore related products

![]()

Kidney disease

When it comes to insurance, kidney disease is considered a high-risk condition. It is a chronic condition that often requires routine medical maintenance, and it can lead to complications such as stroke. The progression of kidney disease can impact insurance options, and it is important to understand how insurance works in relation to this disease.

Firstly, it is worth noting that the Affordable Care Act (Obamacare) has made it illegal for insurance providers to deny coverage based on pre-existing conditions, which includes kidney disease. This means that, regardless of your health status, you cannot be turned down for health insurance. This is true for both public and private health insurance options. Public health insurance is funded by the government, while private insurance is paid for by the individual or shared between an employee and their employer.

For those with kidney disease, Medicare is an important option to consider. Medicare is typically available for people over 65, but there is a special provision for those with kidney failure, also known as End-Stage Renal Disease (ESRD). Medicare covers 80% of dialysis treatment costs and 80% of immunosuppressant medications after a kidney transplant. There are two main ways to get coverage through Medicare: Original Medicare (Parts A and B) and Medicare Advantage Plans (Part C), which often offer additional benefits such as prescription drug coverage. It is important to review your Medicare plan annually to understand any changes to your coverage.

In addition to Medicare, there are other financial assistance options for those with kidney disease. State Health Insurance Assistance Programs (SHIPs) offer local advice and counselling to help individuals choose the best plan for their needs. State kidney programs also provide financial assistance and other services, and State Pharmaceutical Assistance Programs (SPAPs) help pay for prescription medications in certain states. Group health insurance, obtained through an employer or union, can also provide coverage for kidney disease, and it often works in conjunction with Medicare to cover additional costs.

While kidney disease is a high-risk condition, there are insurance options available to help manage the costs of treatment. It is important to carefully review your insurance plan to understand your coverage and explore the various financial assistance programs that can provide support.

Creating an E-Insurance Account: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

HIV/AIDS

When applying for life insurance, companies will typically ask for a health history, a list of current prescriptions, and sometimes a brief medical exam. They may also request a copy of your medical records from your healthcare providers. Insurers will then categorise applicants based on their risk. If you have any of the following conditions, you are likely considered high-risk: cancer, heart attack, stroke, kidney disease, and chronic obstructive pulmonary disease (COPD).

To apply for HIV life insurance, you will typically need to undergo a medical exam and submit 5+ years of medical records. All traditional life insurance policies (term, whole, universal) require HIV testing during the application process. Guaranteed issue policies do not. Underwriting requires a self-identification process, where you review a series of statements. If you meet the criteria, you can proceed with the application. The above are the minimum required criteria and are subject to change. Other health issues may impact eligibility. You must be in good health, between the ages of 30 and 60, and free of respiratory diseases such as tuberculosis (TB) or non-TB mycobacterial infection. You must also have no history of an AIDS-defining condition.

In the United States, the Affordable Care Act (ACA), passed in 2010, has expanded access to coverage and services for people with and at risk of HIV. As a result, the number of uninsured people living with HIV has fallen significantly. Most people with HIV do have insurance coverage, particularly through Medicaid and private insurance. Additionally, many receive support from the Ryan White HIV/AIDS Program, the nation's safety net program for people with HIV.

Gap Insurance: Money-Waster or Smart Buy?

You may want to see also

Explore related products

![]()

Stroke

When applying for life insurance, companies will often categorise applicants based on their risk profile. Insurers will consider your medical history, current prescriptions, and may request a brief medical examination or a copy of your medical records.

If you have a history of strokes, a recent stroke, or a stroke that has led to complications like paralysis, you may be considered high-risk and face challenges in obtaining life insurance. This is because strokes are associated with an increased risk of mortality and disability, and the subsequent medical treatment and rehabilitation can be costly. Studies have shown that uninsured and Medicaid patients tend to have lower utilisation of inpatient rehabilitation services after a stroke, which can impact their recovery and increase the risk of permanent disability.

Additionally, certain social factors can influence the risk of stroke. Research has indicated that living in a poor or rural area, having a low education or income level, and belonging to certain racial groups can increase the likelihood of experiencing a stroke. These social determinants of health can have a significant impact on an individual's overall health and well-being.

It is important to note that the impact of a stroke on insurance rates may vary depending on the specific circumstances and the individual's overall health profile. Different insurance companies may have varying criteria for assessing risk, so it is beneficial to explore options from multiple insurers.

In terms of health insurance, the implementation of the Affordable Care Act has made it so that applications are no longer denied based on medical history or pre-existing conditions. However, insurance status can still impact the quality of care and outcomes for stroke patients, with uninsured and Medicaid patients potentially facing disparities in treatment and rehabilitation services.

Fixed Interest Account Insurance: Benefits and Drawbacks

You may want to see also

Frequently asked questions

Some common diseases that may be considered high-risk for insurance include cancer, heart disease, kidney disease, diabetes, and mental health conditions such as depression and anxiety.

Having a high-risk disease may make it more difficult to qualify for an insurance policy, and you may face higher premiums or have certain restrictions on your policy. However, it is still possible to obtain insurance even with a high-risk disease, and there are ways to reduce your risk classification.

Insurance companies consider various factors when determining an applicant's risk level, including medical history, current health, treatments, hobbies, lifestyle choices, and profession. They may request your health records, a list of prescriptions, and sometimes a brief medical exam.