Flooding is the most common and costly natural disaster in the US, with 99% of counties experiencing floods. The Federal Emergency Management Agency (FEMA) designates special areas with elevated flood risk, known as 100-year flood zones. These zones have an annual probability of 1% of experiencing a major flood. Homes and businesses in high-risk flood areas with mortgages from government-backed lenders are required to have flood insurance. FEMA's National Flood Insurance Program (NFIP) provides insurance to help reduce the socioeconomic impact of floods, with nearly one-third of NFIP claims coming from outside high-risk flood areas. The NFIP provides flood insurance to property owners, renters, and businesses, aiding them in faster recovery after floods.

| Characteristics | Values |

|---|---|

| Flood Insurance Provider | National Flood Insurance Program (NFIP) |

| NFIP Manager | Federal Emergency Management Agency (FEMA) |

| FEMA's High-Risk Flood Zones | Zones that start with the letters "A" or "V" |

| NFIP Coverage | Buildings, contents in a building, or both |

| NFIP Policyholders | 4.7 million |

| NFIP Coverage Amount | $1.3 trillion |

| NFIP Claims from High-Risk Zones | 60% |

| NFIP Average Claim Payment | $68,000 |

| NFIP Waiting Period | 30 days |

| NFIP Quote Tool | Available |

| NFIP Contact Number | (877) 336-2627 |

| Flood Risk Factors | Ground elevation, building foundation, number of floors, wall type, flood openings |

Explore related products

![]()

Flood zones

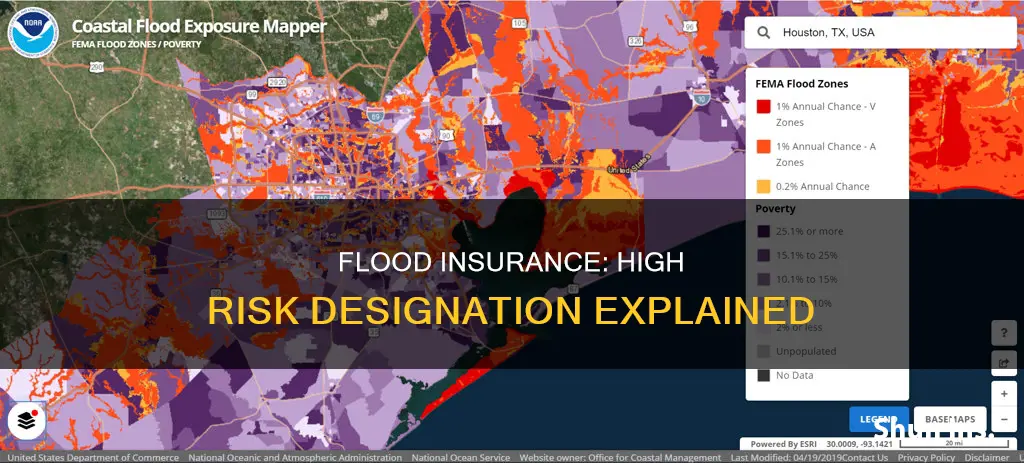

FEMA's high-risk flood zones, also known as Special Flood Hazard Areas (SFHAs), are those that begin with the letters "A" or "V". Homeowners located in these zones are typically required to purchase flood insurance, especially if they have a government-backed mortgage. Over a 30-year period, homes in these areas have a 1 in 4 chance of flooding at least once.

FEMA's low and moderate-risk flood zones, on the other hand, are designated by the letters "X," "B," or "C". Flood insurance is not mandatory in these zones, but it is still recommended as flooding can occur in these areas as well. About 40% of NFIP claims come from outside high-risk flood areas, and even areas with mitigation efforts like levees can experience shallow flooding.

When determining a property's flood risk, FEMA considers various factors, including the ground elevation relative to the surrounding area and nearby flooding sources. Other factors that influence flood risk include the number of floors in a building, the type of construction, and the presence of flood openings or crawl spaces.

It's important to note that flooding can occur anywhere, and even properties outside of official flood zones can be at risk. FEMA recommends flood insurance to protect property owners from financial losses, and it is available to anyone living in the participating NFIP communities.

The Lady in Standard Insurance Commercials: Her Real Age

You may want to see also

Explore related products

![]()

Mortgage lenders

As a mortgage lender, it's important to understand the flood risk in the areas you serve and how this may impact your clients. Flood insurance is a crucial consideration for homeowners, particularly those in high-risk flood zones. While standard homeowners' insurance typically does not cover flood damage, flood insurance provides specialized coverage for damage caused by flooding, rising waters, and storm surges.

Designating High-Risk Flood Zones

High-risk flood zones, also known as Special Flood Hazard Areas (SFHAs), are designated by FEMA based on their susceptibility to flooding. These areas are prone to flooding due to their proximity to bodies of water or their location in floodplains. FEMA provides flood maps that identify these high-risk zones, and it's essential for lenders to refer to these maps when assessing the flood risk of a property.

Lender Requirements for Flood Insurance

Factors Affecting Flood Insurance Premiums

When assisting borrowers in obtaining flood insurance, it's important to understand the factors that influence premium costs. Flood insurance premiums can vary significantly, depending on the location of the property, its elevation, and the flood zone designation. The type of structure, its age, and the coverage amounts selected also impact the premium. Homeowners can reduce premiums by obtaining elevation certificates or implementing flood mitigation features.

Protecting Your Clients' Investments

As a lender, it is your responsibility to inform loan applicants of any flood insurance requirements for their specific properties. By understanding the lender's requirements and securing appropriate flood insurance coverage, borrowers can navigate the mortgage process smoothly while safeguarding their homes and belongings from potential flood damage. It is advisable to encourage borrowers to consult with insurance providers to determine the necessary coverage and associated costs.

Understanding Insurance: Why You Still Owe Money

You may want to see also

Explore related products

![]()

Building construction

The National Flood Insurance Program (NFIP) provides flood insurance to property owners, renters, and businesses. The NFIP works with communities to adopt and enforce floodplain management regulations that help mitigate flooding effects.

NFIP's building performance requirements are contained in Title 44 of the U.S. Code of Federal Regulations at Section 60.3 Floodplain Management Criteria for Flood-prone Areas. These regulations help state and local officials interpret the NFIP regulations and are useful resources for homeowners, insurance agents, building professionals, and designers.

NFIP regulations for new construction generally apply to new and substantially improved accessory structures. The NFIP provides guidance on the required use of flood-damage-resistant construction materials for building components located below the Base Flood Elevation in Special Flood Hazard Areas (both A and V zones).

NFIP also provides guidance on the installation of elevators below the Base Flood Elevation in Special Flood Hazard Areas (A and V zones). In addition, the NFIP outlines the need for, selection of, and use of corrosion-resistant metal connectors for the construction of buildings in coastal areas.

When determining the flood insurance rate, three factors are considered: where the property is built, how it's built, and what it would cost to replace it. The risk is greater for foundations underground or at ground level than for those elevated above the ground. Buildings with more floors spread flood risk over a larger area. Individual units on a building's higher floors have a lower risk of flooding than units on lower floors. Masonry walls perform better in flooding events than wood frame walls. A building with flood openings can lower flood risk by allowing floodwaters to flow through the structure. Moving or raising heating and cooling systems, water heaters, electrical panels, and other utilities can also reduce the risk of flood damage.

Allstate Insurance: Saving Money with Smart Strategies

You may want to see also

Explore related products

![]()

Flood risk factors

One key factor is the elevation of the building relative to the surrounding area and nearby water sources. Foundations that are underground or at ground level have a higher risk of flooding compared to those that are elevated. The number of floors in a building also plays a role, as more floors distribute the flood risk across a larger area. The construction materials of a building can impact its resilience to flooding; masonry walls, for instance, perform better than wood frames. Additionally, buildings with flood openings can reduce the risk by allowing water to flow through the structure.

The location of a property is also a significant factor. FEMA identifies areas with varying flood risks using Flood Insurance Rate Maps (FIRMs). These maps help determine flood insurance pricing and guide floodplain management regulations. FEMA's high-risk flood zones, also known as Special Flood Hazard Areas (SFHAs), are designated by the letters "A" or "V". Properties in these zones have a higher risk of flooding and are typically required to have flood insurance, especially if they have government-backed mortgages.

Other location-based risk factors include proximity to rivers or other flood sources, the effectiveness of the local drainage system, and the presence of natural infrastructure that can mitigate flooding, such as levees. It is worth noting that flooding can occur anywhere, and even areas outside of high-risk zones can experience flooding. Factors such as summer storms, melting snow, neighborhood construction, and broken water mains can contribute to flooding.

The cost of flood insurance is influenced by the property's location within a flood zone and the likelihood of flooding. FEMA's Risk Rating 2.0 approach considers these factors to set flood insurance rates. Properties in high-risk areas may incur higher premiums, and additional factors such as the presence of a basement or the elevation of utilities can impact the cost of insurance.

Understanding these flood risk factors is essential for property owners to make informed decisions about flood insurance and implement appropriate mitigation measures to reduce potential flood damage.

Contractor Additional Insured: Builders Risk Protection

You may want to see also

Explore related products

![]()

Insurance costs

The National Flood Insurance Program (NFIP) is managed by FEMA and delivered by a network of more than 47 insurance companies. The NFIP provides flood insurance to property owners, renters, and businesses, helping them recover after flood events.

The NFIP's pricing approach uses the best available flood risk data to set premiums based on each property's individual risk. This includes the likelihood of different types of flooding, the characteristics of the building, elevation, distance from flooding sources, and the replacement cost value of the building.

The cost of flood insurance varies depending on several factors, with location being a primary consideration. Homes in high-risk flood zones, known as Special Flood Hazard Areas (SFHAs), are more likely to pay higher premiums. These areas have a 26% chance of flooding over a 30-year period, and lenders generally require homeowners in these zones to have flood insurance. For example, in Texas, homeowners in coastal counties can expect to pay higher premiums, with average NFIP policy costs of $992 to $1,029 per year.

The level of coverage also influences the cost. The more coverage you need, the higher the insurance cost will be. The type of policy, such as contents-only or building-only, also affects the rate. Additionally, the age of the home, its design, and materials used are considered when determining rates.

The NFIP introduced Risk Rating 2.0 to set flood insurance rates, which incorporates multiple variables to determine a property's flood risk. This includes the property's replacement value, the likelihood of different types of flooding, and the home's proximity to flooding sources. As a result of Risk Rating 2.0, approximately 77% of existing NFIP policies experienced increased costs.

It's important to note that flood insurance rates are not static and can change over time as flood risks evolve. While flood insurance may be an additional cost for homeowners, it provides financial protection in the event of flooding, which is becoming increasingly common.

Navigating the Claims Process: Understanding the Role of an Insurance Adjuster During Times of Grief

You may want to see also

Frequently asked questions

The NFIP is a federal program that provides flood insurance to property owners, renters, and businesses. The program is managed by FEMA and delivered by a network of insurance companies.

FEMA uses Flood Insurance Rate Maps (FIRMs) to identify areas of varying flood risk. FEMA maps the areas with a 1% annual chance of flooding, known as Special Flood Hazard Areas (SFHAs). FEMA's high-risk flood zones begin with the letters "A" or "V".

The NFIP considers various factors, including the ground elevation of the building relative to the surrounding area, the number of floors in the building, and the construction materials used.

Flood insurance is mandatory for properties located in high-risk flood zones if the mortgages are government-backed. However, it is important to note that flood insurance is not required in low or moderate-risk zones.

You can enter your address into the Federal Emergency Management Agency's Flood Map Service Center to determine your home's flood risk and the corresponding insurance rates.