When it comes to health insurance, understanding which company provides your coverage is essential for managing your healthcare needs effectively. Whether you're seeking medical treatment, filing a claim, or simply want to review your policy details, knowing your health insurance provider is the first step. In many cases, this information can be found on your insurance card, through your employer's benefits portal if you have employer-sponsored insurance, or by contacting your insurance agent or broker. Additionally, you may receive correspondence or statements from your insurance company that include this information. It's important to keep your health insurance details up to date and easily accessible to ensure you can make informed decisions about your healthcare and financial well-being.

| Characteristics | Values |

|---|---|

| Insurance Type | Health |

| Company Name | [Your Insurance Company Name] |

| Policy Number | [Your Policy Number] |

| Coverage Period | [Start Date] - [End Date] |

| Premium Amount | [Premium Amount] |

| Deductible | [Deductible Amount] |

| Co-pay | [Co-pay Amount] |

| Network Type | [In-network/Out-of-network] |

| Coverage Details | [Description of Coverage] |

| Contact Information | [Customer Service Phone Number], [Website URL] |

Explore related products

$49.18 $233.95

What You'll Learn

- Identifying Insurance Provider: Steps to find out which company provides your health insurance coverage

- Understanding Policy Details: Key aspects to know about your health insurance policy, including coverage and exclusions

- Network of Providers: Information on the healthcare providers and facilities included in your insurance network

- Premium and Cost Sharing: Details about your monthly premium, deductible, copayments, and coinsurance responsibilities

- Customer Service and Support: How to contact your insurance company for assistance, file claims, or resolve issues

![]()

Identifying Insurance Provider: Steps to find out which company provides your health insurance coverage

To identify your health insurance provider, begin by examining any insurance cards or documents you have. These typically include the name and logo of the insurance company, along with your policy number and other relevant details. If you don't have physical copies, check your email or online accounts where such documents might be stored electronically.

If you're still unable to locate your insurance information, contact your employer's human resources department. They can provide details about the company's health insurance plan and the provider. Alternatively, if you've recently received medical care, the billing department at the healthcare facility may be able to tell you which insurance company they've billed for your services.

Another option is to check with state insurance regulators. Many states have online databases where you can search for insurance companies and verify their licensure status. You can also contact your state's insurance department directly for assistance.

In some cases, you may need to conduct a more thorough search. This could involve reviewing your bank statements for any automatic payments to an insurance provider or checking with previous employers if you've changed jobs recently. It's also a good idea to keep track of any correspondence related to your health insurance, as this may contain important information about your provider.

Once you've identified your health insurance provider, make sure to keep this information in a safe and accessible place. It's essential to have this data readily available when seeking medical care or dealing with insurance-related matters.

Understanding Monthly Tax Credits for Health Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Understanding Policy Details: Key aspects to know about your health insurance policy, including coverage and exclusions

To understand the intricacies of your health insurance policy, it's crucial to delve into the details of coverage and exclusions. This involves scrutinizing the policy document to identify what medical services and treatments are covered, as well as those that are not. Covered services typically include doctor visits, hospital stays, prescription medications, and preventive care, but the specifics can vary widely depending on the policy. Exclusions, on the other hand, are conditions or treatments that the insurance company will not pay for, such as cosmetic procedures, alternative therapies, or certain pre-existing conditions.

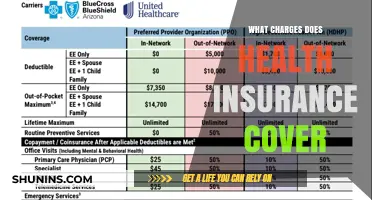

One key aspect to consider is the concept of in-network versus out-of-network providers. In-network providers are those who have a contract with your insurance company, which generally means you'll pay less out of pocket for their services. Out-of-network providers, however, may charge higher rates, and your insurance may cover a smaller portion of the costs. Understanding which providers are in your network can help you make informed decisions about your healthcare and avoid unexpected expenses.

Another important detail to examine is the policy's deductible, copayments, and coinsurance. The deductible is the amount you must pay out of pocket before your insurance coverage kicks in, while copayments are fixed amounts you pay for each service or prescription. Coinsurance, on the other hand, is a percentage of the cost that you're responsible for after meeting your deductible. These financial details can significantly impact your overall healthcare costs, so it's essential to be familiar with them.

Additionally, it's wise to review the policy's limitations on certain treatments or medications. For example, some policies may have restrictions on the number of therapy sessions covered or may require prior authorization for certain medications. Being aware of these limitations can help you plan your healthcare needs accordingly and avoid potential denials of coverage.

Lastly, don't overlook the importance of understanding your policy's appeals process. If you disagree with a coverage decision made by your insurance company, you have the right to appeal. Familiarizing yourself with the steps involved in the appeals process can be invaluable if you ever need to challenge a denial of coverage.

By thoroughly examining these key aspects of your health insurance policy, you can gain a clearer understanding of your coverage and make more informed decisions about your healthcare.

Unemployed? Here’s How to Secure Affordable Health Insurance Coverage

You may want to see also

Explore related products

![]()

Network of Providers: Information on the healthcare providers and facilities included in your insurance network

Understanding the network of providers associated with your health insurance is crucial for maximizing your coverage and minimizing out-of-pocket expenses. The network typically includes a range of healthcare professionals and facilities, such as primary care physicians, specialists, hospitals, and outpatient clinics. These providers have agreed to offer services at negotiated rates, which can significantly reduce your healthcare costs.

To navigate your network effectively, it's essential to familiarize yourself with the different types of providers available. Primary care physicians (PCPs) serve as the first point of contact for most health concerns and can refer you to specialists when necessary. Specialists focus on specific areas of healthcare, such as cardiology, dermatology, or orthopedics, and often require a referral from a PCP. Hospitals within the network provide inpatient care for more severe conditions, while outpatient clinics offer services like lab tests, imaging, and minor procedures.

When selecting a provider, consider factors such as location, hours of operation, and patient reviews. Many insurance companies offer online directories or mobile apps that allow you to search for in-network providers based on these criteria. Additionally, some plans may offer telemedicine options, which can be convenient for minor illnesses or follow-up appointments.

It's also important to understand the different levels of coverage provided by your insurance plan. Some services, like preventive care, may be fully covered, while others, such as prescription medications or physical therapy, may require copays or coinsurance. Reviewing your plan's summary of benefits and coverage (SBC) can help you understand what services are covered and at what cost.

Finally, be aware of any network limitations or exclusions. Some plans may have narrow networks, which can restrict your choice of providers, or may exclude certain types of care, such as mental health services or alternative treatments. Understanding these limitations can help you make informed decisions about your healthcare and avoid unexpected costs.

Insurance Companies: Uncovering Deceptive Practices and Hidden Profits

You may want to see also

Explore related products

![Catalogue of Insurance Publications, American and Foreign: a Comprehensive List of Works Upon All Classes of Insurance, by Well Known Authors of All Countries 1911 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Premium and Cost Sharing: Details about your monthly premium, deductible, copayments, and coinsurance responsibilities

Understanding your health insurance plan's premium and cost-sharing components is crucial for managing your healthcare expenses effectively. Your monthly premium is the fixed amount you pay to maintain your insurance coverage, and it's typically deducted from your paycheck or billed directly to you. This premium grants you access to a network of healthcare providers and facilities, and it's essential to pay it on time to avoid any lapses in coverage.

In addition to your premium, you'll also need to be familiar with your deductible, which is the amount you must pay out-of-pocket for covered services before your insurance plan begins to pay. Deductibles can vary widely depending on your plan, so it's important to review your policy documents to understand your specific deductible requirements. Once you've met your deductible, your insurance plan will typically cover a percentage of your healthcare costs, while you'll be responsible for the remaining amount, known as your copayment or coinsurance.

Copayments are fixed amounts you pay for specific services, such as doctor's visits or prescription medications, while coinsurance is a percentage of the cost of a service that you're responsible for. For example, if your plan covers 80% of the cost of a hospital stay, you'll be responsible for the remaining 20% as coinsurance. It's important to note that copayments and coinsurance can add up quickly, so it's essential to budget for these expenses when planning your healthcare costs.

To minimize your out-of-pocket expenses, it's a good idea to choose healthcare providers and facilities within your insurance plan's network, as these providers have agreed to accept the plan's negotiated rates. Additionally, many plans offer preventive care services, such as annual check-ups and screenings, at no additional cost to you, so taking advantage of these services can help you save money in the long run.

In conclusion, understanding your health insurance plan's premium and cost-sharing components is essential for managing your healthcare expenses effectively. By reviewing your policy documents and familiarizing yourself with your deductible, copayments, and coinsurance requirements, you can make informed decisions about your healthcare and avoid unexpected costs.

Supplementing Work Insurance: Can Medicaid Help?

You may want to see also

Explore related products

![]()

Customer Service and Support: How to contact your insurance company for assistance, file claims, or resolve issues

To effectively navigate customer service and support with your health insurance company, it's crucial to understand the various channels available for assistance. Most health insurance providers offer multiple contact methods, including phone, email, and online chat. When reaching out, ensure you have your policy number and relevant details handy to expedite the process.

Filing claims can often be done online through the insurance company's portal, which may require creating an account if you haven't already. This portal typically allows you to submit necessary documentation, track the status of your claim, and view your benefits. If you prefer a more traditional approach, many companies also accept claims via mail or fax.

Resolving issues may involve appealing a denied claim or addressing billing concerns. In such cases, it's important to follow the company's specific appeals process, which is usually outlined on their website or in your policy documents. Keep detailed records of all communications, including dates, times, and the names of representatives you speak with, to ensure a clear paper trail.

Many health insurance companies also offer additional support services, such as 24/7 nurse lines or wellness programs. These resources can provide valuable guidance and assistance beyond just claims and billing. Familiarize yourself with the full range of services offered by your provider to make the most of your coverage.

In summary, effective communication with your health insurance company involves understanding the available contact methods, properly filing claims, and knowing how to resolve issues. By staying informed and organized, you can ensure a smoother experience and better outcomes when dealing with customer service and support.

Does Your Health Insurance Cover COVID-19 Testing? Find Out Now

You may want to see also

Frequently asked questions

You can typically find this information on your insurance card, through your employer's benefits portal, or by contacting your HR department directly.

Reach out to your insurance company's customer service department. They can assist you with claims, explain your coverage, and help you understand your benefits.

Check your insurance card or documentation. Private insurance usually lists a specific company name, while government programs like Medicare or Medicaid will indicate that they are government-sponsored.