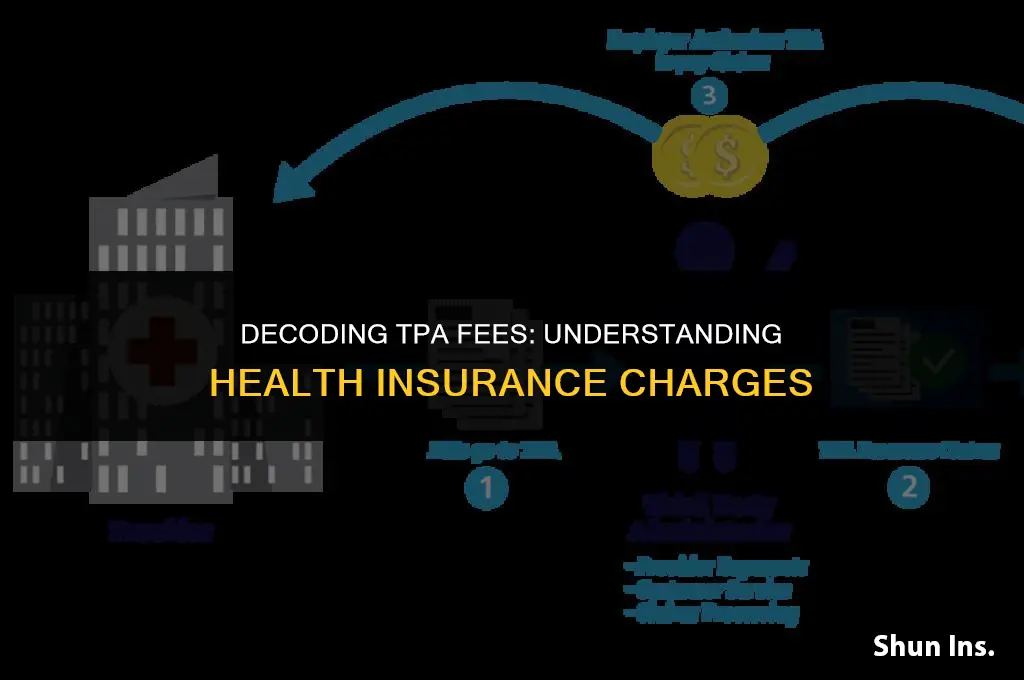

Third-Party Administrators (TPAs) play a crucial role in managing health insurance claims and related administrative tasks for insurance companies and employers. When it comes to charging for health insurance, TPAs typically do not directly charge policyholders. Instead, they charge fees to insurance companies or employer-sponsored health plans for their administrative services. These fees can vary widely depending on the scope of services provided, the size of the plan, and the complexity of the claims being processed. TPAs may charge per claim, per member, or a flat fee for their services. Understanding these fee structures is essential for stakeholders in the healthcare industry to ensure transparency and efficiency in health insurance administration.

| Characteristics | Values |

|---|---|

| Coverage Type | Individual, Family, Group |

| Network | In-network, Out-of-network |

| Deductible | $500, $1000, $2000 |

| Co-insurance | 80/20, 70/30, 60/40 |

| Co-pay | $20, $30, $40 |

| Annual Limit | $1,000,000, $2,000,000 |

| Prescription Coverage | Yes, No |

| Dental Coverage | Yes, No |

| Vision Coverage | Yes, No |

| Mental Health Coverage | Yes, No |

| Wellness Programs | Yes, No |

| Telemedicine | Yes, No |

| Premiums | Monthly, Quarterly, Annually |

| Payment Options | Online, Mail, Automatic Withdrawal |

| Customer Service | Phone, Email, Chat |

Explore related products

What You'll Learn

- Premiums: Monthly or annual fees paid to maintain health insurance coverage

- Deductibles: Amounts paid out-of-pocket before insurance coverage begins

- Co-payments: Fixed fees paid for each healthcare service or prescription

- Co-insurance: Percentage of healthcare costs shared with the insurer after deductible

- Out-of-pocket maximums: Limits on total annual out-of-pocket expenses for covered services

![]()

Premiums: Monthly or annual fees paid to maintain health insurance coverage

Health insurance premiums are a critical component of maintaining coverage, and understanding how they work is essential for policyholders. These premiums are the monthly or annual fees paid to keep a health insurance policy active. They are calculated based on various factors, including the policyholder's age, health status, and the level of coverage desired.

One of the key aspects of premiums is that they are typically paid in advance. This means that policyholders must pay for their coverage before they can use it. For example, if someone chooses to pay their premium annually, they will need to pay the full amount upfront to ensure they have coverage for the entire year.

Premiums can vary significantly depending on the type of plan chosen. For instance, a high-deductible health plan (HDHP) may have lower premiums than a low-deductible plan, but the policyholder will pay more out-of-pocket when receiving medical care. Conversely, a plan with a lower deductible may have higher premiums but provide more immediate coverage.

It's also important to note that premiums can increase over time. This can happen due to inflation, changes in healthcare costs, or the policyholder's age and health status. Insurers may also adjust premiums based on the overall health of the insured population or changes in government regulations.

Policyholders can often choose how frequently they pay their premiums. While monthly payments are common, some insurers offer the option to pay quarterly, semi-annually, or annually. Choosing the right payment frequency can depend on individual financial situations and preferences.

In conclusion, health insurance premiums are a fundamental part of maintaining coverage. By understanding how they are calculated, when they are paid, and how they can change, policyholders can make informed decisions about their health insurance plans.

Understanding Permanent Health Insurance: Long-Term Coverage and Benefits Explained

You may want to see also

Explore related products

![]()

Deductibles: Amounts paid out-of-pocket before insurance coverage begins

In the realm of health insurance, deductibles represent the initial financial hurdle that policyholders must clear before their insurance coverage springs into action. This out-of-pocket expense is a critical component of health insurance plans, as it directly impacts the cost-sharing dynamics between the insured individual and the insurance provider. Deductibles can vary widely in amount, depending on the specific insurance plan and the level of coverage desired.

For instance, a high-deductible health plan (HDHP) typically requires policyholders to pay a significant amount out-of-pocket before their insurance coverage begins. This can range from a few hundred to several thousand dollars. In contrast, a low-deductible plan may have a much lower threshold, potentially as little as $50 or $100. The choice between a high or low deductible plan often depends on the individual's financial situation, their expected healthcare needs, and their willingness to assume a greater share of the healthcare costs in exchange for lower monthly premiums.

It's important to note that deductibles are not the only out-of-pocket costs associated with health insurance. Policyholders may also be responsible for copayments, coinsurance, and other expenses, even after they have met their deductible. Therefore, when evaluating the overall cost of a health insurance plan, it's essential to consider the full range of potential out-of-pocket costs, not just the deductible amount.

When selecting a health insurance plan, individuals should carefully consider their healthcare needs and budget to determine the most appropriate deductible amount. Those who anticipate frequent medical expenses may benefit from a lower deductible, while those who are generally healthy and wish to minimize their monthly premiums may opt for a higher deductible. By understanding the role of deductibles in health insurance and carefully weighing the options, policyholders can make informed decisions that best suit their individual circumstances.

Star Health Insurance: Claiming Medical Expenses Simplified

You may want to see also

Explore related products

![]()

Co-payments: Fixed fees paid for each healthcare service or prescription

Co-payments, or co-pays, are a common feature of many health insurance plans. They represent a fixed fee that an insured individual must pay out-of-pocket for each healthcare service or prescription they receive. This fee is typically a small percentage of the total cost of the service or medication, but it can add up over time, especially for those with chronic conditions or who require frequent medical attention.

One of the key aspects of co-payments is that they are usually predetermined and outlined in the insurance policy's benefits schedule. This means that the insured individual knows exactly how much they will need to pay for each type of service or medication. For example, a policy might specify a co-pay of $20 for a doctor's visit, $50 for a specialist consultation, and $10 for a generic prescription medication.

Co-payments serve several purposes in the healthcare system. Firstly, they help to control costs by discouraging unnecessary or excessive use of healthcare services. By requiring a small payment for each service, individuals are more likely to think carefully about whether they really need to see a doctor or fill a prescription. Secondly, co-payments help to ensure that the insured individual has some "skin in the game," which can lead to more responsible healthcare decisions.

However, co-payments can also have some negative consequences. For those with low incomes or high healthcare needs, the cumulative cost of co-payments can be a significant financial burden. This can lead to individuals delaying or forgoing necessary medical care, which can ultimately result in worse health outcomes and higher overall healthcare costs.

In recent years, there has been a trend towards higher co-payments, particularly for brand-name medications and specialty services. This is often done in an effort to control rising healthcare costs, but it can also make it more difficult for individuals to access the care they need. As a result, it is important for individuals to carefully review their insurance policies and understand their co-payment obligations before enrolling in a plan.

Should You Enroll in Health Insurance? Pros, Cons, and Key Considerations

You may want to see also

Explore related products

$49.18 $233.95

![]()

Co-insurance: Percentage of healthcare costs shared with the insurer after deductible

After meeting your deductible, you'll typically encounter co-insurance, which is the percentage of healthcare costs you share with your insurer. This co-insurance rate varies widely depending on your specific health insurance plan. For example, a plan with an 80/20 co-insurance split would mean your insurer covers 80% of the costs, leaving you responsible for the remaining 20%. Understanding your co-insurance rate is crucial for budgeting healthcare expenses, as it directly impacts how much you'll pay out-of-pocket for medical services.

Co-insurance rates can differ significantly between plans, ranging from 50/50 splits to 90/10 splits. The lower your co-insurance percentage, the more comprehensive your coverage, but typically, the higher your premium will be. Conversely, a higher co-insurance rate means lower premiums but higher out-of-pocket costs when you need medical care. When selecting a health insurance plan, it's essential to consider your expected healthcare needs and budget to choose a co-insurance rate that balances affordability with adequate coverage.

It's also important to note that co-insurance applies only after you've met your deductible. Until your deductible is satisfied, you'll be responsible for the full cost of your healthcare services. Once your deductible is met, your co-insurance kicks in, and you'll start sharing the costs with your insurer. Additionally, some plans may have separate deductibles and co-insurance rates for different types of care, such as in-network versus out-of-network services, or medical care versus prescription drugs.

When comparing health insurance plans, pay close attention to the co-insurance rates, as they can have a significant impact on your overall healthcare costs. If you anticipate frequent medical visits or have chronic conditions requiring ongoing treatment, a plan with a lower co-insurance rate may be more cost-effective in the long run. On the other hand, if you're generally healthy and don't expect to need much medical care, a plan with a higher co-insurance rate and lower premiums might be more suitable.

In summary, co-insurance is a critical component of health insurance that determines how much you'll pay for healthcare services after meeting your deductible. By understanding your co-insurance rate and how it applies to your specific healthcare needs, you can make informed decisions when selecting a health insurance plan and better manage your healthcare expenses.

Mastering Cold Calls: Effective Strategies for Health Insurance Prospects

You may want to see also

Explore related products

![]()

Out-of-pocket maximums: Limits on total annual out-of-pocket expenses for covered services

Out-of-pocket maximums are a critical component of health insurance plans, designed to protect policyholders from excessive financial burdens due to medical expenses. These limits cap the total amount an individual must pay annually for covered services, providing a safety net against catastrophic health costs. Typically, once a policyholder's out-of-pocket expenses reach the maximum threshold, the insurance plan covers 100% of eligible medical costs for the remainder of the year.

The specific out-of-pocket maximum varies depending on the insurance plan and can range from a few thousand to several tens of thousands of dollars. Factors influencing these limits include the type of plan (e.g., HMO, PPO, EPO), the insurance provider, the policyholder's age, and the level of coverage selected. For instance, plans with lower premiums often have higher out-of-pocket maximums, while more expensive plans may offer lower limits, providing greater financial protection.

It's essential for policyholders to understand their out-of-pocket maximums and how they apply. This knowledge can help individuals make informed decisions about their healthcare, such as whether to seek treatment for a condition or delay non-urgent medical procedures until the next plan year. Additionally, understanding out-of-pocket limits can aid in budgeting for healthcare expenses and selecting the most appropriate insurance plan during open enrollment periods.

Policyholders should also be aware of the differences between out-of-pocket maximums and deductibles. While deductibles are the initial amounts paid by the policyholder before insurance coverage kicks in, out-of-pocket maximums represent the total financial burden a policyholder will face annually for covered services. Some plans may have separate out-of-pocket maximums for in-network and out-of-network care, further complicating the decision-making process.

In conclusion, out-of-pocket maximums play a vital role in health insurance, safeguarding policyholders from exorbitant medical costs. By understanding these limits and how they interact with other plan features, individuals can make more informed choices about their healthcare and insurance coverage, ultimately leading to better financial and health outcomes.

Understanding Out-of-Pocket Medical Costs: Part B Supplemental Insurance

You may want to see also

Frequently asked questions

Third-Party Administrators (TPAs) typically charge a fee for processing health insurance claims. This fee can vary depending on the complexity of the claim and the specific services provided by the TPA.

TPA fees are usually factored into the overall cost of health insurance premiums. Insurers may pass on these administrative costs to policyholders, which can contribute to higher premium rates.

Yes, TPA charges are often subject to regulatory oversight. Insurance departments and other regulatory bodies may set guidelines or caps on the fees that TPAs can charge to ensure fairness and transparency in the health insurance market.

Policyholders typically do not negotiate TPA fees directly. Instead, these fees are negotiated between the insurer and the TPA as part of their contractual agreement. However, policyholders can shop around for health insurance plans with lower administrative costs by comparing different insurers and their TPA arrangements.