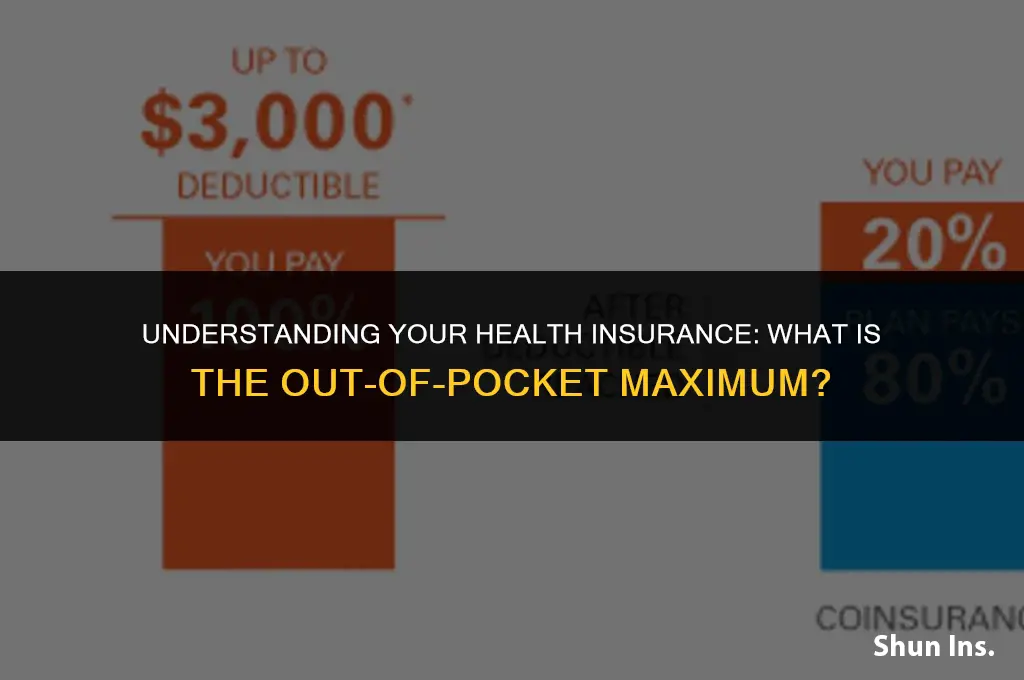

The out-of-pocket maximum is a crucial aspect of health insurance plans that determines the most a policyholder will have to pay for covered medical expenses within a given period, typically a year. Once this limit is reached, the insurance company covers 100% of the remaining eligible costs. This provision helps protect individuals from financial ruin due to high medical bills and is an essential consideration when choosing a health insurance plan. Understanding the out-of-pocket maximum involves grasping various components such as deductibles, copays, and coinsurance, as well as how these costs accumulate towards the maximum limit.

Explore related products

What You'll Learn

- Definition: The maximum amount an insured person pays annually for healthcare expenses not covered by insurance

- Calculation: Typically calculated as a percentage of the total healthcare costs or a fixed dollar amount

- Impact: Helps in limiting the financial burden on the insured, ensuring affordability of healthcare services

- Variations: Differs by insurance plan, with some offering lower out-of-pocket maximums for in-network services

- Importance: Essential for comparing insurance plans and understanding potential healthcare costs for the insured

![]()

Definition: The maximum amount an insured person pays annually for healthcare expenses not covered by insurance

The out-of-pocket maximum is a critical component of health insurance plans, representing the highest amount an insured individual will have to pay for healthcare costs not covered by their insurance policy within a given year. This financial threshold is designed to protect policyholders from excessive medical expenses, ensuring that their financial burden is capped regardless of the total cost of their healthcare needs.

Understanding the out-of-pocket maximum is essential for consumers when selecting a health insurance plan. It helps them anticipate their potential financial exposure and plan accordingly. For instance, individuals with chronic conditions or those who anticipate needing extensive medical care may opt for plans with lower out-of-pocket maximums to minimize their expenses. Conversely, healthier individuals might choose plans with higher maximums to benefit from lower premiums.

The calculation of the out-of-pocket maximum typically includes deductibles, copayments, and coinsurance, but excludes premiums. Once an insured person's out-of-pocket expenses reach the maximum limit, the insurance company covers 100% of the remaining eligible expenses for the remainder of the year. This can provide significant financial relief, especially in cases of unexpected or catastrophic illnesses.

It's important to note that the out-of-pocket maximum can vary widely among different insurance plans and providers. Some plans may have separate maximums for different types of care, such as in-network versus out-of-network services, or prescription drugs versus other medical expenses. Additionally, family plans often have a combined out-of-pocket maximum that applies to all covered family members, which can be more cost-effective than individual plans.

When comparing health insurance options, it's crucial to consider not only the out-of-pocket maximum but also other factors such as the plan's coverage, network, and overall cost. By carefully evaluating these aspects, individuals can choose a plan that best fits their healthcare needs and financial situation, ensuring they have adequate protection against unforeseen medical expenses.

Average Health Insurance Costs for Individuals in 2009 Revealed

You may want to see also

Explore related products

![]()

Calculation: Typically calculated as a percentage of the total healthcare costs or a fixed dollar amount

The calculation of out-of-pocket maximums in health insurance is a critical component for policyholders to understand. Typically, this figure is calculated as a percentage of the total healthcare costs incurred by the insured individual or family. For instance, if a policy states an out-of-pocket maximum of 20% of total healthcare costs, and the total costs amount to $10,000, the policyholder would be responsible for paying $2,000 out of pocket. This calculation method helps to cap the financial burden on the insured, ensuring that they do not face exorbitant expenses in the event of significant healthcare needs.

Alternatively, some health insurance plans may calculate the out-of-pocket maximum as a fixed dollar amount. In this scenario, regardless of the total healthcare costs, the policyholder would only be required to pay up to the specified dollar limit. For example, if the out-of-pocket maximum is set at $5,000, the insured individual would not have to pay more than this amount, even if their healthcare costs exceed $20,000. This fixed amount approach provides a clear and predictable financial exposure for the policyholder, which can be particularly beneficial for budgeting and financial planning purposes.

Understanding how the out-of-pocket maximum is calculated is essential for individuals and families when selecting a health insurance plan. It allows them to assess the potential financial impact of their healthcare expenses and make informed decisions about their coverage. Moreover, being aware of this calculation method can help policyholders to better navigate the complexities of their health insurance benefits and ensure that they are maximizing their coverage while minimizing their out-of-pocket expenses.

In addition to the calculation method, it is also important for policyholders to be aware of any exclusions or limitations that may apply to their out-of-pocket maximum. For instance, certain plans may exclude specific types of healthcare services or treatments from the out-of-pocket maximum calculation, which could result in higher expenses for the insured individual. By carefully reviewing the terms and conditions of their health insurance policy, policyholders can gain a comprehensive understanding of their financial responsibilities and make the most of their coverage.

Overall, the calculation of out-of-pocket maximums in health insurance plays a vital role in determining the financial obligations of policyholders. Whether calculated as a percentage of total healthcare costs or a fixed dollar amount, this figure provides a crucial safeguard against excessive medical expenses, enabling individuals and families to manage their healthcare costs effectively and maintain financial stability.

Understanding Insurance Denials and Your Options

You may want to see also

Explore related products

![]()

Impact: Helps in limiting the financial burden on the insured, ensuring affordability of healthcare services

The out-of-pocket maximum in health insurance plays a crucial role in safeguarding the financial well-being of the insured. By capping the amount an individual must pay for healthcare expenses out of their own pocket, this provision helps prevent catastrophic financial burdens that can arise from unexpected medical costs. This is particularly important for those facing chronic illnesses or requiring extensive medical treatments, as it ensures that they can access necessary care without depleting their savings or incurring substantial debt.

One of the key benefits of the out-of-pocket maximum is its ability to make healthcare services more affordable. When individuals know that their expenses will be limited, they are more likely to seek timely medical attention, adhere to treatment plans, and utilize preventive care services. This can lead to better health outcomes and reduced overall healthcare costs, as early intervention and management of health conditions can prevent more serious and expensive complications down the line.

Moreover, the out-of-pocket maximum can provide a sense of security and peace of mind to the insured. Knowing that there is a limit to their financial exposure can help alleviate the stress and anxiety associated with medical bills, allowing individuals to focus on their health and recovery rather than worrying about the financial implications of their care. This psychological benefit should not be underestimated, as financial stress can have a significant impact on both mental and physical health.

In addition to its direct financial benefits, the out-of-pocket maximum can also influence the behavior of healthcare providers and insurers. By setting a clear limit on the costs that can be passed on to patients, this provision can incentivize providers to be more mindful of their billing practices and encourage insurers to negotiate more favorable rates with healthcare facilities. This can lead to a more efficient and cost-effective healthcare system, ultimately benefiting both patients and providers.

Overall, the out-of-pocket maximum is a critical component of health insurance that helps ensure the affordability and accessibility of healthcare services. By limiting the financial burden on the insured, this provision can improve health outcomes, reduce overall healthcare costs, and provide a sense of security to individuals and families. As such, it is an essential consideration for anyone evaluating health insurance options and seeking to protect their financial well-being.

Re-enrolling in Apple Health Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Variations: Differs by insurance plan, with some offering lower out-of-pocket maximums for in-network services

The out-of-pocket maximum in health insurance is a critical component that can significantly impact the financial burden on policyholders. While it is a standard feature across many plans, there are notable variations that can affect how much an individual might pay out of pocket for their healthcare services.

One key variation lies in the differentiation between in-network and out-of-network services. Some insurance plans offer lower out-of-pocket maximums for services received within the plan's network. This incentivizes policyholders to utilize healthcare providers that are part of the network, potentially reducing their overall healthcare costs. For example, a plan might have an out-of-pocket maximum of $5,000 for in-network services but $10,000 for out-of-network services.

Another variation is the presence of separate out-of-pocket maximums for different types of services. For instance, some plans might have distinct maximums for medical services, prescription drugs, and mental health services. This can be particularly important for individuals with specific healthcare needs, as it can affect the overall affordability of their care.

Furthermore, some plans may offer additional protections or benefits that can help reduce out-of-pocket expenses. For example, certain plans might provide a deductible waiver for in-network services or offer a coinsurance reduction for preventive care. These features can help policyholders save money and make their healthcare more affordable.

When selecting a health insurance plan, it is essential to carefully review the out-of-pocket maximums and any variations that might apply. Understanding these details can help individuals choose a plan that best meets their healthcare needs and financial situation. By comparing different plans and their out-of-pocket maximums, policyholders can make informed decisions and potentially save money on their healthcare costs.

Get Free Medical Insurance in California: A Step-by-Step Guide

You may want to see also

Explore related products

$16.89 $28.99

![]()

Importance: Essential for comparing insurance plans and understanding potential healthcare costs for the insured

Understanding the out-of-pocket maximum in health insurance is crucial for individuals and families when comparing different insurance plans. This figure represents the total amount an insured person will have to pay for healthcare expenses within a given year before the insurance company starts covering 100% of the costs. It's a critical component in assessing the financial burden that could be placed on the insured in the event of significant medical expenses.

When evaluating health insurance options, the out-of-pocket maximum can help in determining the potential financial risk exposure. Plans with lower out-of-pocket maximums generally offer more financial protection but may come with higher premiums. Conversely, plans with higher out-of-pocket maximums might have lower premiums but could lead to substantial expenses if healthcare needs are extensive. Therefore, it's essential to balance the premium cost with the out-of-pocket maximum to find a plan that best fits one's financial situation and healthcare needs.

Moreover, the out-of-pocket maximum is particularly important for those with chronic conditions or who anticipate needing frequent medical care. For these individuals, reaching the out-of-pocket maximum could mean the difference between manageable healthcare costs and financial strain. It's also a key consideration for families, as the out-of-pocket maximum can apply individually or cumulatively, affecting the overall financial planning for healthcare expenses.

In conclusion, the out-of-pocket maximum is a vital aspect of health insurance that should not be overlooked. It plays a significant role in comparing insurance plans and understanding the potential healthcare costs that the insured might face. By carefully considering the out-of-pocket maximum, individuals can make informed decisions about their health insurance, ensuring they have adequate coverage and financial protection.

Health Insurance Essentials for Your Cuban Adventure: What You Need to Know

You may want to see also

Frequently asked questions

The out-of-pocket maximum is the most you will have to pay for covered medical expenses in a given year. Once you reach this limit, your health insurance will cover 100% of your eligible expenses for the remainder of the year.

The out-of-pocket maximum works by accumulating your payments for deductibles, copays, and coinsurance throughout the year. Once your total out-of-pocket spending reaches the maximum limit set by your insurance plan, you are considered to have met your out-of-pocket maximum, and your insurance will cover all eligible expenses for the rest of the year.

Expenses that count towards the out-of-pocket maximum typically include deductibles, copays, and coinsurance for covered medical services. However, premiums, balance bills from out-of-network providers, and expenses for non-covered services usually do not count towards the out-of-pocket maximum.

The out-of-pocket maximum is important because it provides financial protection to policyholders by limiting their annual spending on medical expenses. This can help individuals and families budget for healthcare costs and avoid significant financial burdens in the event of unexpected medical emergencies or chronic health conditions.