Missing the deadline for health insurance enrollment can have significant consequences, as it often results in a coverage gap that leaves you financially vulnerable to unexpected medical expenses. Most health insurance plans, including those offered through the Affordable Care Act (ACA) marketplace, have specific open enrollment periods, and failing to sign up during this time typically means you’ll have to wait until the next enrollment period unless you qualify for a special enrollment period due to a qualifying life event, such as marriage, the birth of a child, or loss of other coverage. Without insurance, you may face high out-of-pocket costs for medical care, prescription medications, and preventive services, and you could also be subject to penalties or taxes in some states. Additionally, going without coverage increases the risk of delaying necessary medical treatment, which can lead to more serious health issues and higher long-term costs. It’s crucial to understand your options, such as short-term health plans or state-specific programs, and to plan ahead to avoid missing future enrollment deadlines.

| Characteristics | Values |

|---|---|

| Loss of Coverage | If you miss the Open Enrollment deadline, you may lose health insurance coverage unless you qualify for a Special Enrollment Period (SEP). |

| Special Enrollment Period (SEP) | You may qualify for SEP if you experience a qualifying life event (e.g., marriage, birth of a child, loss of job-based coverage). |

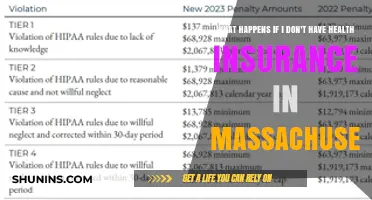

| Penalty (if applicable) | In some regions (e.g., Massachusetts, New Jersey, California), missing the deadline may result in a tax penalty for not having coverage. |

| Limited Coverage Options | Outside Open Enrollment, you may only access short-term health plans or private insurance, which often have limited benefits and exclusions. |

| No Access to Subsidies | Missing the deadline means you cannot apply for premium tax credits or cost-sharing reductions available through the Health Insurance Marketplace. |

| Waiting Period | If you qualify for SEP, there may be a waiting period before your new coverage begins. |

| No Retroactive Coverage | Coverage typically starts prospectively from the date of enrollment, not retroactively to the missed deadline. |

| State-Specific Rules | Some states have extended enrollment periods or additional protections, so outcomes vary by location. |

| Medicaid/CHIP Enrollment | Medicaid and CHIP have year-round enrollment, so missing the health insurance deadline does not affect eligibility for these programs. |

| Short-Term Plan Limitations | Short-term plans (available year-round) do not cover pre-existing conditions and may exclude essential health benefits. |

Explore related products

What You'll Learn

![]()

Late Enrollment Penalties

Missing the health insurance enrollment deadline can trigger late enrollment penalties, a consequence often overlooked until it’s too late. These penalties are not just financial inconveniences; they are deliberate measures designed to encourage timely enrollment and maintain the stability of insurance pools. For example, under the Affordable Care Act (ACA), individuals who go without qualifying health coverage for more than three consecutive months may face a penalty, calculated as the greater of a flat fee ($750 per adult and $375 per child in 2023) or a percentage of household income (2.5% above the tax filing threshold). Understanding these penalties is crucial for avoiding unnecessary costs and ensuring continuous coverage.

The mechanics of late enrollment penalties vary depending on the type of insurance. For Medicare, missing the initial enrollment period (typically around your 65th birthday) can result in permanent surcharges on Part B premiums. These surcharges increase by 10% for each 12-month period you delay enrollment, a penalty that lasts as long as you have Medicare. Similarly, employer-sponsored plans may impose waiting periods for late enrollees, leaving individuals uninsured for several months. To mitigate these risks, mark your calendar for open enrollment periods and set reminders well in advance.

A common misconception is that late enrollment penalties are universal across all insurance types. In reality, they are more prevalent in government-regulated plans like Medicare and ACA Marketplace coverage. Private insurance plans outside these frameworks may not impose penalties but often have stricter underwriting processes for late applicants, potentially leading to higher premiums or denied coverage due to pre-existing conditions. This disparity highlights the importance of researching your specific insurance type and its associated rules.

Practical steps can help minimize the impact of late enrollment penalties. First, explore special enrollment periods (SEPs) triggered by life events such as marriage, job loss, or relocation. These windows allow you to enroll outside the standard open enrollment period without penalties. Second, if you’ve missed a deadline, consider short-term health plans or health-sharing ministries as temporary coverage options, though these alternatives often lack comprehensive benefits. Finally, consult a licensed insurance broker who can navigate your options and identify potential exemptions or reductions in penalties.

The takeaway is clear: late enrollment penalties are avoidable with proactive planning and awareness. By understanding the specific rules of your insurance type, leveraging special enrollment periods, and seeking expert guidance, you can sidestep these costly consequences. Treat enrollment deadlines as non-negotiable to protect both your health and your finances.

UVMMC: Understanding Employee Insurance Benefits

You may want to see also

Explore related products

![]()

Loss of Coverage Options

Missing the health insurance enrollment deadline can leave you in a precarious situation, particularly if you're transitioning between coverage options. Once the deadline passes, you typically lose the opportunity to enroll in a marketplace plan until the next open enrollment period, unless you qualify for a special enrollment period due to a life event like marriage, divorce, or loss of job-based coverage. This gap in coverage can expose you to financial risks if unexpected medical expenses arise. For instance, a single emergency room visit can cost thousands of dollars without insurance, and chronic conditions requiring ongoing treatment can become financially crippling.

If you find yourself without coverage, explore alternative options to bridge the gap. Short-term health insurance plans, though limited in scope and often excluding pre-existing conditions, can provide temporary protection for up to 364 days in many states. These plans are not required to comply with Affordable Care Act (ACA) regulations, so they may not cover essential health benefits like prescription drugs or maternity care. Another option is to join a health-sharing ministry, which pools members’ contributions to cover medical expenses. However, these ministries are not insurance and may impose religious or lifestyle requirements for membership.

For those who miss the deadline due to job loss, COBRA (Consolidated Omnibus Budget Reconciliation Act) allows you to continue your employer-sponsored health insurance for a limited time, typically up to 18 months. While COBRA ensures continuity of coverage, it’s often expensive since you’re responsible for the full premium plus an administrative fee. If COBRA is unaffordable, consider Medicaid, which provides coverage for low-income individuals and families. Eligibility varies by state, but the program covers essential health services, including doctor visits, hospital stays, and preventive care.

A less conventional but practical approach is to negotiate directly with healthcare providers or hospitals. Many offer sliding-scale fees or payment plans for uninsured patients, particularly for routine care or elective procedures. Additionally, community health clinics and federally qualified health centers provide low-cost or free services based on income. These options, while not comprehensive, can help manage costs until you regain full coverage.

Ultimately, missing the health insurance deadline underscores the importance of proactive planning. If you anticipate a coverage gap, research your options well in advance and set reminders for enrollment periods. While alternatives exist, they often come with limitations or higher costs, making timely enrollment the most reliable way to secure comprehensive, affordable coverage.

Does Health Insurance Save Lives? Exploring the Critical Impact

You may want to see also

Explore related products

![]()

Limited Plan Availability

Missing the health insurance enrollment deadline often restricts you to limited plan availability, a consequence that can significantly impact your healthcare options. During the open enrollment period, insurers typically offer a wide range of plans, including HMOs, PPOs, and high-deductible health plans (HDHPs), often paired with Health Savings Accounts (HSAs). However, once this window closes, your choices shrink dramatically. Outside of open enrollment, you may only qualify for short-term health plans, which are not required to cover essential health benefits like prescription drugs, maternity care, or mental health services. These plans often exclude pre-existing conditions and cap coverage at amounts as low as $2,000,000, leaving you vulnerable to high out-of-pocket costs.

To navigate limited plan availability, consider the following steps. First, determine if you qualify for a Special Enrollment Period (SEP), which allows you to enroll in a comprehensive plan if you experience a qualifying life event, such as losing job-based coverage, getting married, or having a child. Second, research state-specific options; some states, like California and New York, offer extended enrollment periods or state-run marketplaces with more flexibility. Third, evaluate short-term plans carefully, focusing on their exclusions and coverage limits. For instance, if you’re under 30 and generally healthy, a short-term plan might suffice for catastrophic coverage, but it’s not a substitute for comprehensive insurance.

The takeaway is clear: limited plan availability outside the enrollment period forces you into a corner, often leaving you with inadequate or incomplete coverage. For example, a short-term plan might cover emergency room visits but exclude preventive care, which is crucial for long-term health. This gap can lead to delayed diagnoses and higher costs down the line. If you’re over 50 or have chronic conditions, the risks are even greater, as limited plans rarely cover the specialized care you may need.

Persuasively, it’s worth noting that limited plan availability isn’t just an inconvenience—it’s a financial and health risk. Without access to comprehensive plans, you’re more likely to skip necessary care due to cost, which can exacerbate health issues. For instance, forgoing a $300 specialist visit could lead to a $30,000 hospital stay later. To mitigate this, set calendar reminders for open enrollment, typically from November 1 to January 15, and explore all possible avenues for coverage, including employer-sponsored plans, Medicaid, or COBRA if applicable. Proactive planning is your best defense against the pitfalls of limited plan availability.

Are Spouses Considered Dependents for Health Insurance Coverage?

You may want to see also

Explore related products

![]()

Higher Premium Costs

Missing the health insurance enrollment deadline can trigger a cascade of financial consequences, with higher premium costs being a significant and immediate penalty. When you fall outside the designated enrollment period, insurers often view you as a higher-risk applicant. This perception stems from the assumption that individuals who delay coverage may be doing so due to pre-existing health conditions or a higher likelihood of needing medical care. As a result, insurers may charge you a higher premium to offset the anticipated costs of your care. This increase can be substantial, often ranging from 10% to 50% more than what you would have paid if you had enrolled on time.

For example, consider a 35-year-old individual in good health who misses the Open Enrollment Period (OEP) for health insurance. If the standard monthly premium for their age group is $300, they might find themselves facing a premium of $350 to $450 when they finally secure coverage. This higher cost isn’t just a one-time fee; it’s a recurring expense that can strain your budget for the entire coverage period. Moreover, if you’re self-employed or don’t have access to employer-sponsored insurance, this financial burden falls entirely on you, making it even more critical to avoid missing deadlines.

To mitigate the risk of higher premiums, it’s essential to understand the enrollment periods and plan accordingly. The Annual Open Enrollment Period (OEP) typically runs from November 1 to December 15, though this can vary by state. If you miss this window, you may qualify for a Special Enrollment Period (SEP) if you experience a qualifying life event, such as losing job-based coverage, getting married, or having a child. However, not all life events trigger an SEP, and even when they do, the window to enroll is usually limited to 60 days from the event date. Failing to act within this timeframe leaves you vulnerable to higher premiums when you eventually secure coverage.

Another practical tip is to explore short-term health plans or health-sharing ministries as temporary alternatives if you miss the OEP. While these options don’t offer the comprehensive coverage of ACA-compliant plans, they can provide a financial safety net until the next enrollment period. However, be cautious: short-term plans often exclude pre-existing conditions and may not cover essential health benefits like prescription drugs or maternity care. Always weigh the trade-offs and ensure the plan meets your immediate needs without exposing you to excessive out-of-pocket costs.

In conclusion, missing the health insurance deadline can lead to higher premium costs that significantly impact your financial stability. By understanding enrollment periods, exploring temporary alternatives, and acting promptly during Special Enrollment Periods, you can minimize the risk of paying more for coverage. Proactive planning and awareness of your options are key to avoiding this costly consequence.

Medical and Health Insurance: Are They Synonymous?

You may want to see also

Explore related products

![The Penalty [Blu-ray]](https://m.media-amazon.com/images/I/91fZ8MEHZ4L._AC_UY218_.jpg)

![The Penalty (Silent) [DVD]](https://m.media-amazon.com/images/I/6109T6eX3wL._AC_UY218_.jpg)

![]()

Grace Period Exceptions

Missing the health insurance enrollment deadline can feel like a costly mistake, but not all hope is lost. Many insurance providers and government-run marketplaces offer grace periods, allowing you to enroll or make payments after the official deadline without penalties. However, these grace periods aren’t universal, and their duration varies widely—typically ranging from 10 to 90 days depending on the plan or state regulations. Understanding these exceptions is crucial, as they can provide a safety net for those who face unforeseen circumstances.

One common grace period exception is for individuals experiencing qualifying life events, such as losing job-based coverage, getting married, having a baby, or moving to a new state. In these cases, you’re granted a Special Enrollment Period (SEP), which typically lasts 60 days from the date of the event. For example, if you lose your job and employer-sponsored insurance on March 15, you have until mid-May to enroll in a new plan without facing a coverage gap. It’s essential to act promptly, as delaying enrollment could result in being uninsured during critical times.

Another exception arises in states with extended enrollment periods or those that operate their own health insurance marketplaces. For instance, California and New York often provide longer enrollment windows than the federal marketplace, sometimes extending into early January for coverage starting the same year. Additionally, some states offer short-term grace periods for premium payments, allowing policyholders an extra 10 to 30 days to pay overdue premiums before coverage is canceled. Always check your state’s specific rules, as they can significantly differ from federal guidelines.

For those on Medicaid or CHIP, grace period exceptions are more flexible. These programs often allow continuous enrollment for eligible individuals, especially children and pregnant women, regardless of the standard open enrollment period. If your income fluctuates or you experience a change in household size, you may qualify for immediate coverage or a grace period to reapply without losing benefits. This ensures that vulnerable populations remain protected even if they miss traditional deadlines.

Practical tip: Keep detailed records of any qualifying life events or extenuating circumstances, such as medical emergencies or natural disasters, that may warrant a grace period exception. Contact your insurance provider or marketplace immediately to explain your situation and request an extension. Being proactive and informed can make the difference between securing coverage and facing a gap in health insurance.

Adding Your Newborn to Health Insurance: Timely Steps for Coverage

You may want to see also

Frequently asked questions

If you miss the Open Enrollment Period for health insurance, you may not be able to enroll in a plan unless you qualify for a Special Enrollment Period due to a qualifying life event, such as marriage, birth of a child, or loss of other coverage.

If you miss the deadline and don’t qualify for a Special Enrollment Period, you may need to explore alternative options like short-term health plans, Medicaid (if eligible), or health-sharing ministries, though these may not offer the same comprehensive coverage as ACA-compliant plans.

There is no federal penalty for missing the health insurance enrollment deadline, but some states (like California, New Jersey, and Massachusetts) have their own mandates and may impose penalties for not having coverage. Always check your state’s specific rules.