Estimating income incorrectly when applying for health insurance can have significant financial and coverage-related consequences. If you overestimate your income, you may end up paying higher premiums than necessary, while underestimating it could result in receiving less financial assistance than you qualify for, such as reduced premiums or cost-sharing subsidies. Additionally, if your actual income differs significantly from your estimate, you may face repayment of excess subsidies during tax season or, conversely, miss out on benefits you were entitled to. These discrepancies can also affect your eligibility for certain plans or programs, such as Medicaid, leading to gaps in coverage or unexpected out-of-pocket costs. Accurate income estimation is therefore crucial to ensure you receive the appropriate level of assistance and maintain continuous, affordable health insurance coverage.

| Characteristics | Values |

|---|---|

| Overestimation of Income | If you estimate your income higher than your actual income, you may receive less financial assistance (e.g., premium tax credits or cost-sharing reductions) than you qualify for. This could result in higher monthly premiums and out-of-pocket costs during the year. |

| Underestimation of Income | If you estimate your income lower than your actual income, you may receive more financial assistance than you qualify for. This could lead to having to pay back the excess assistance when you file your taxes the following year. |

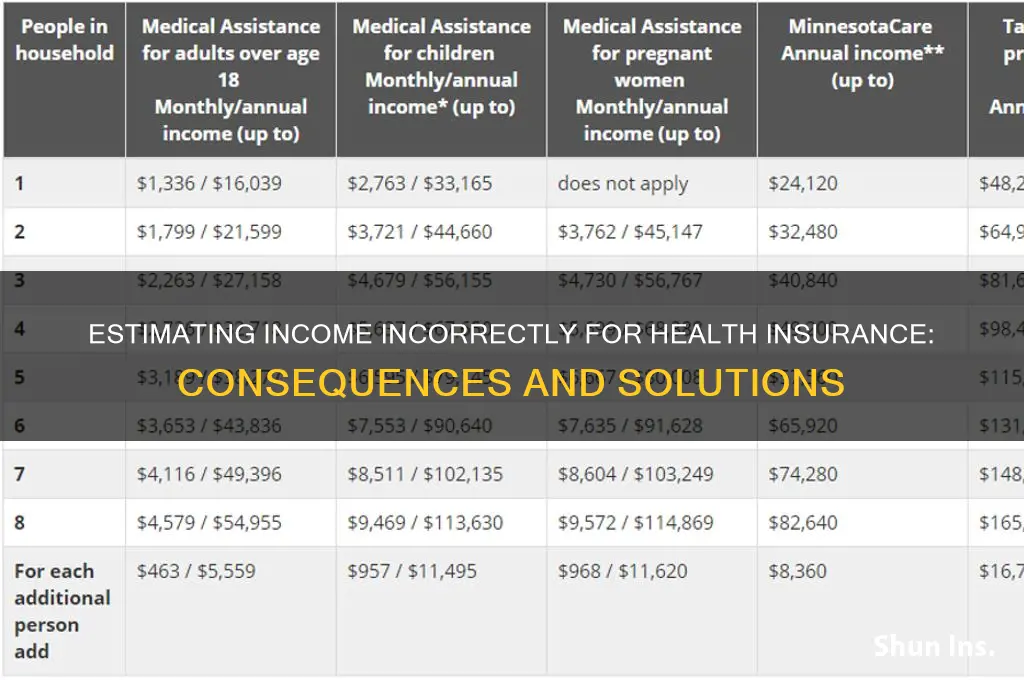

| Repayment Limits (2023 Data) | For individuals with incomes below 200% of the federal poverty level (FPL), repayment limits apply. As of 2023, the maximum repayment amounts are: $325 (income below 150% FPL), $800 (150-200% FPL), and $1,600 (200-250% FPL) for single filers. For families, the limits are higher. |

| Reconciliation Process | At the end of the tax year, you must reconcile your estimated income with your actual income on Form 8962 (Premium Tax Credit). This determines if you owe money or will receive a refund based on the difference between the assistance you received and what you qualified for. |

| Impact on Coverage | Estimating income incorrectly does not affect your eligibility for health insurance coverage through the Marketplace. However, it impacts the amount of financial assistance you receive. |

| Mid-Year Income Changes | If your income changes during the year, you should update your information on Healthcare.gov to adjust your financial assistance accordingly. Failure to do so may result in repayment or reduced assistance at tax time. |

| Penalties for Intentional Misreporting | Intentionally providing false income information can result in penalties, including fines or legal consequences, as it is considered fraud. |

| Retroactive Adjustments | If you underestimate your income, you may not be able to retroactively increase your premiums to avoid repayment. Conversely, if you overestimate, you cannot retroactively claim additional assistance. |

| State-Specific Rules | Some states may have additional rules or programs that affect how income estimation errors are handled, particularly in states that expanded Medicaid. |

| Appeals Process | If you disagree with the repayment amount or other determinations, you can appeal the decision through the Marketplace or IRS, depending on the issue. |

Explore related products

What You'll Learn

- Overestimating income: Higher premiums, potential repayment of excess subsidies at tax time

- Underestimating income: Lower premiums, risk of owing money at tax time

- Mid-year income changes: Adjustments needed to avoid penalties or unexpected costs

- Impact on subsidies: Incorrect estimates reduce or eliminate premium tax credits

- Verification process: Inaccurate estimates trigger audits, requiring proof of income

![]()

Overestimating income: Higher premiums, potential repayment of excess subsidies at tax time

Estimating your income accurately when applying for health insurance is crucial, as overestimating can lead to higher premiums and unexpected financial burdens. When you predict your earnings on the higher side, the health insurance marketplace calculates your eligibility for subsidies based on this inflated figure. As a result, you might end up paying more in monthly premiums than necessary, since subsidies are designed to reduce costs for those with lower incomes. For instance, if you estimate an annual income of $60,000 but actually earn $50,000, you could miss out on hundreds of dollars in premium savings each month.

The repercussions of overestimating income don’t stop at higher premiums; they extend to tax season, where you may face the unpleasant task of repaying excess subsidies. The Advanced Premium Tax Credit (APTC) is paid directly to your insurer to lower your monthly premiums, but it’s based on your estimated income. If your actual income falls below your estimate, the IRS will reconcile the difference when you file taxes. For example, if you received $3,000 in subsidies based on an overestimated income, you might owe that amount back if your actual earnings qualify you for a smaller subsidy or none at all. This can be a significant financial shock, especially if you’re living paycheck to paycheck.

To avoid these pitfalls, take a proactive approach to income estimation. Start by reviewing your previous year’s tax returns and factoring in any anticipated changes, such as a new job, reduced hours, or side income. If you’re self-employed or have variable income, conservatively estimate your earnings by averaging the past two years’ income or consulting a financial advisor. Tools like the IRS’s Tax Withholding Estimator can also help you project your income more accurately. Remember, it’s better to underestimate slightly and pay a small difference later than to overestimate and face higher premiums and repayment obligations.

If you realize mid-year that your income estimate was too high, act quickly to update your information on the health insurance marketplace. Reporting income changes promptly can adjust your subsidy amount and reduce the risk of overpayment. For example, if you lose a job or experience a significant drop in income, notify the marketplace within 30 days to recalculate your eligibility. While this won’t erase past overpayments, it can minimize future financial strain and ensure your premiums align with your current earnings.

In summary, overestimating your income for health insurance can lead to higher premiums and the potential repayment of excess subsidies at tax time. By carefully projecting your earnings, using available tools, and promptly reporting changes, you can avoid these costly mistakes. While it’s impossible to predict your income with absolute precision, a thoughtful and conservative approach can protect you from financial surprises and ensure you receive the appropriate level of assistance.

Understanding Ambetter Health Insurance: Coverage, Benefits, and Enrollment Guide

You may want to see also

Explore related products

![]()

Underestimating income: Lower premiums, risk of owing money at tax time

Estimating your income accurately when applying for health insurance is crucial, as it directly impacts the subsidies you receive and, consequently, your monthly premiums. Underestimating your income might seem like a strategic move to secure lower premiums, but it’s a risky gamble. Here’s why: when you report lower income, the government may provide you with advanced premium tax credits (APTCs) to reduce your monthly costs. However, if your actual income exceeds the estimate, you’ll be required to repay some or all of those subsidies when you file your taxes. For example, if you estimate an income of $40,000 but earn $50,000, you could owe hundreds or even thousands of dollars at tax time.

Let’s break down the mechanics. The Affordable Care Act (ACA) uses your modified adjusted gross income (MAGI) to determine eligibility for subsidies. If your income falls below 400% of the federal poverty level (FPL), you qualify for APTCs. For 2023, 400% of the FPL is approximately $54,360 for an individual and $111,000 for a family of four. Underestimating your income to fall within this range might temporarily lower your premiums, but it’s a short-term gain with potential long-term pain. The IRS will reconcile your actual income with your estimated income during tax season, and any discrepancy will result in a bill for the excess subsidies received.

To avoid this pitfall, take a proactive approach to income estimation. Start by reviewing your previous year’s tax return and consider any anticipated changes in your financial situation. If you’re self-employed or have variable income, average your earnings over the past few years to create a more accurate projection. Tools like the Healthcare.gov subsidy calculator can help you estimate your eligibility for APTCs based on your income. Additionally, if your income fluctuates during the year, report changes to the marketplace promptly to adjust your subsidies and avoid repayment surprises.

A common misconception is that underestimating income is a victimless error, but it can lead to financial strain and stress. For instance, a family of three earning $70,000 might underestimate their income to $60,000 to qualify for higher subsidies. If their actual income remains at $70,000, they could owe $2,000 or more in repaid subsidies. This scenario underscores the importance of honesty and precision in income reporting. While lower premiums are enticing, the risk of owing money at tax time far outweighs the temporary benefit.

In conclusion, underestimating your income for health insurance may yield lower premiums initially, but it’s a risky strategy with significant financial consequences. Accurate income reporting ensures you receive the appropriate subsidies without facing unexpected repayment demands. By taking the time to project your income thoughtfully and using available tools, you can avoid this common trap and maintain financial stability throughout the year. Remember, honesty in estimation isn’t just a best practice—it’s a safeguard for your wallet.

Insurance PI Ethics: Sexual Advances and Professional Boundaries Explored

You may want to see also

Explore related products

![]()

Mid-year income changes: Adjustments needed to avoid penalties or unexpected costs

Estimating your income accurately for health insurance is crucial, but life happens—jobs change, bonuses arrive, or side hustles flourish. Mid-year income fluctuations can throw off your initial estimate, potentially leading to penalties or unexpected costs if left unaddressed. The Affordable Care Act (ACA) ties premium tax credits and subsidies to your income, so overestimating or underestimating can have tangible consequences. For instance, if you earn more than anticipated, you might owe money at tax time for excess subsidies received. Conversely, underestimating could mean missing out on financial assistance you’re entitled to.

To avoid these pitfalls, proactively report income changes to the health insurance marketplace as soon as they occur. This triggers a review of your eligibility for subsidies, ensuring your premiums align with your current financial situation. For example, if you receive a $10,000 raise mid-year, updating your income could reduce your monthly premium tax credit, preventing a surprise repayment demand during tax season. Conversely, if your income drops—say, due to reduced work hours—promptly reporting this change could increase your subsidy, lowering your monthly premiums immediately.

While adjusting your income estimate is straightforward, timing matters. Life events like marriage, divorce, or the birth of a child qualify for a special enrollment period, allowing immediate updates. However, general income changes don’t always trigger this option, so annual open enrollment becomes your next opportunity to correct your estimate. To stay ahead, monitor your income monthly and use tools like the IRS’s tax withholding estimator to gauge potential changes.

A practical tip: keep detailed records of income shifts, including pay stubs, freelance invoices, or bonus documentation. This not only aids in accurate reporting but also serves as proof if discrepancies arise. Additionally, consider consulting a tax professional or insurance navigator to navigate complex scenarios, such as fluctuating self-employment income or multiple household earners. By staying vigilant and proactive, you can minimize financial surprises and ensure your health insurance remains affordable and aligned with your income reality.

Understanding Medicare: Co-Insurance Percentage Explained

You may want to see also

Explore related products

![]()

Impact on subsidies: Incorrect estimates reduce or eliminate premium tax credits

Estimating your income accurately when applying for health insurance is crucial, especially if you’re counting on premium tax credits to make coverage affordable. These subsidies, calculated based on your projected income, can significantly reduce your monthly premiums. However, an incorrect estimate can lead to unexpected financial consequences. If you overestimate your income, you may receive less in subsidies than you’re entitled to, paying more out of pocket each month. Conversely, underestimating your income can result in receiving more subsidies upfront, but you’ll face a repayment obligation when you file taxes. This delicate balance underscores the importance of precision in your income projections.

Consider a scenario where a 35-year-old individual estimates their annual income at $40,000 but actually earns $50,000. Based on the lower estimate, they qualify for a premium tax credit of $300 per month, reducing their premium from $500 to $200. However, at tax time, the discrepancy is reconciled, and they must repay the excess subsidies—in this case, $3,600. This repayment can strain finances, especially if the individual hasn’t budgeted for it. Conversely, if they had overestimated their income at $60,000, they might only receive a $100 monthly subsidy, paying $400 out of pocket, despite being eligible for the full $300 credit. Both errors highlight the financial risks of inaccurate income estimates.

To avoid these pitfalls, follow a structured approach when estimating your income. Start by reviewing your previous year’s tax return and factoring in any anticipated changes, such as raises, bonuses, or side income. Use pay stubs, contracts, or other documentation to project earnings accurately. If you’re self-employed, analyze past income trends and consider consulting a tax professional for a more precise estimate. Tools like the Health Insurance Marketplace’s income estimator can also provide guidance. Remember, updating your income information during the year if circumstances change can prevent surprises at tax time.

While precision is ideal, it’s also important to understand the flexibility built into the system. If your income fluctuates unexpectedly, the IRS allows for a repayment cap based on your income level. For example, individuals earning up to 200% of the federal poverty level (FPL) in 2023 may only need to repay $600 for excess subsidies, while those earning between 300% and 400% of the FPL face a $2,700 cap. However, relying on these caps isn’t advisable, as they don’t apply if you fail to file taxes or reconcile subsidies. The takeaway? Accuracy is your best defense against financial surprises.

Finally, treat income estimation as an ongoing process rather than a one-time task. Life events like job changes, marriage, or the birth of a child can alter your financial landscape. Regularly review and update your income information on the Marketplace to ensure your subsidies remain aligned with your actual earnings. This proactive approach not only maximizes your benefits but also minimizes the risk of repayment obligations. In the complex world of health insurance, precision in income estimation isn’t just a detail—it’s a cornerstone of financial stability.

Classifying Health Insurance in QuickBooks: A Comprehensive Step-by-Step Guide

You may want to see also

Explore related products

![]()

Verification process: Inaccurate estimates trigger audits, requiring proof of income

Estimating income inaccurately for health insurance can lead to unexpected complications, particularly when it comes to the verification process. If your reported income doesn’t align with actual earnings, it triggers an audit, requiring you to provide detailed proof of income. This process isn’t just a formality—it’s a critical step to ensure fairness in subsidy calculations and prevent fraud. For example, if you estimated an income of $40,000 but earned $60,000, you may have received higher subsidies than you were entitled to, necessitating repayment and potential penalties.

The verification process typically begins with a notice from the health insurance marketplace or your state’s Medicaid office. This notice will outline the discrepancies found and request specific documentation, such as tax returns, pay stubs, or bank statements. For self-employed individuals, this might include profit and loss statements or 1099 forms. Failing to provide this proof within the given timeframe—usually 30 to 90 days—can result in the loss of subsidies, retroactive premium adjustments, or even policy cancellation. It’s crucial to respond promptly and accurately to avoid further complications.

One common pitfall is underestimating income due to fluctuating earnings, such as those from freelance work or seasonal jobs. For instance, a freelancer who estimates $30,000 annually but earns $50,000 due to unexpected projects could face significant repayment demands. To mitigate this, keep detailed records of all income sources throughout the year and update your estimates if your financial situation changes. Tools like income tracking apps or quarterly reviews can help maintain accuracy and reduce audit risks.

Audits aren’t just about correcting errors—they also serve as a deterrent for intentional misrepresentation. Penalties for deliberate income falsification can include fines, legal action, or exclusion from future subsidies. For example, knowingly underreporting income to qualify for Medicaid could result in a fraud investigation. Transparency is key; if you’re unsure about your income projections, consult a tax professional or use the marketplace’s estimation tools to make an informed guess.

In conclusion, the verification process for inaccurate income estimates is rigorous but fair, designed to protect both consumers and the healthcare system. By understanding the triggers for audits and preparing the necessary documentation, you can navigate this process with confidence. Always aim for precision in your income estimates, and if in doubt, err on the side of caution to avoid unforeseen financial burdens.

Understanding Aetna Health Insurance Rates: Factors, Costs, and Coverage

You may want to see also

Frequently asked questions

If you overestimate your income, you may end up paying higher premiums than necessary, as your subsidy or tax credit eligibility is based on your estimated income. However, if your actual income turns out to be lower, you may be eligible for a refund or additional tax credits when you file your taxes.

Underestimating your income can result in receiving more subsidies or tax credits than you're actually eligible for. If this happens, you may have to pay back some or all of the excess amount when you file your taxes, which could result in a surprise tax bill.

Yes, you can report income changes to the health insurance marketplace throughout the year. It's essential to update your income information as soon as possible after a significant change, such as a job loss or increase in income. This will help ensure that your premiums and subsidies are adjusted accordingly, minimizing the risk of owing money or receiving an incorrect subsidy amount.