The question of what income level prevents individuals from having health insurance is a critical issue that intersects with broader socioeconomic and policy concerns. In many countries, particularly those without universal healthcare, access to health insurance is often tied to employment or income thresholds. For instance, in the United States, individuals with incomes below the federal poverty level (FPL) may qualify for Medicaid, while those earning slightly above this threshold might fall into the coverage gap, where they earn too much for Medicaid but too little to afford private insurance. Similarly, in other nations, low-income earners may struggle to afford premiums, copays, or deductibles, effectively preventing them from accessing adequate healthcare. This disparity highlights the need for policies that address affordability and ensure that income does not become a barrier to essential health coverage.

Explore related products

What You'll Learn

- Eligibility for Medicaid: Income limits vary by state, affecting access to affordable health coverage

- ACA Subsidies: Higher incomes reduce premium tax credits, increasing out-of-pocket insurance costs

- Employer Coverage: Low-wage jobs often lack health benefits, leaving workers uninsured

- Medicare Limits: Early retirees with moderate incomes face gaps in coverage before eligibility

- Coverage Gap: In some states, incomes too high for Medicaid but too low for subsidies

![]()

Eligibility for Medicaid: Income limits vary by state, affecting access to affordable health coverage

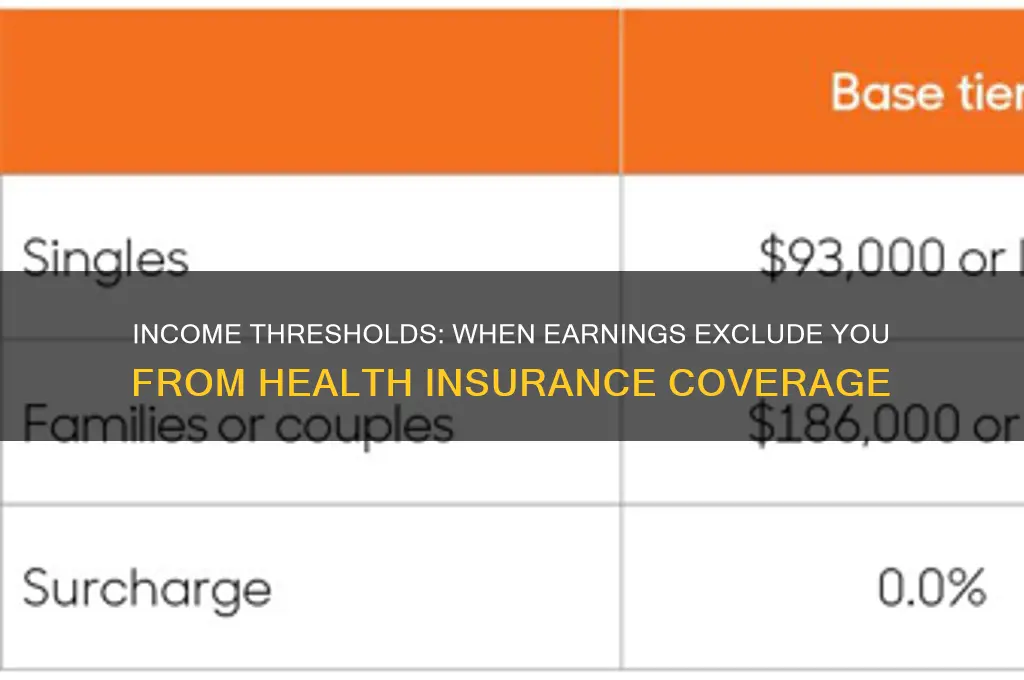

In the United States, Medicaid serves as a critical safety net for millions, offering health coverage to those with limited income and resources. However, eligibility for this program is not uniform across the country. Each state sets its own income limits, creating a patchwork of access that can leave some individuals and families in a coverage gap. For instance, in Texas, a family of three must earn no more than 17% of the federal poverty level (FPL) to qualify, while in New York, the threshold is 138% of the FPL. This disparity means that a family earning the same income could be eligible in one state but ineligible in another, highlighting the profound impact of state-specific policies on healthcare access.

Understanding these income limits requires a closer look at how they are calculated. Most states use the Modified Adjusted Gross Income (MAGI) method, which considers taxable income, deductions, and certain exclusions. For example, in California, a single adult can earn up to $18,754 annually (138% of the FPL) and still qualify for Medicaid, known there as Medi-Cal. In contrast, Alabama’s limit for the same individual is significantly lower, at $4,560 (18% of the FPL). These variations underscore the importance of checking your state’s specific guidelines, as they directly determine whether you fall above or below the eligibility threshold.

For families, the income limits become even more complex, as they scale with household size. In Washington State, a family of four can earn up to $38,295 (138% of the FPL) and qualify for Medicaid, while in Florida, the limit drops to $11,538 (30% of the FPL). This discrepancy can force families in certain states to choose between forgoing health insurance or paying premiums they cannot afford. Practical tips for navigating this include using online eligibility calculators provided by state Medicaid agencies and consulting with local healthcare navigators who can help interpret the rules.

The expansion of Medicaid under the Affordable Care Act (ACA) aimed to standardize eligibility by setting the threshold at 138% of the FPL nationwide. However, not all states have adopted this expansion, further exacerbating the divide. As of 2023, 10 states have yet to expand Medicaid, leaving an estimated 2.2 million people in the coverage gap—earning too much to qualify for traditional Medicaid but too little to afford private insurance. Advocacy efforts in these states continue, but for now, residents must navigate the stricter, pre-ACA income limits, which often exclude childless adults entirely.

In conclusion, while Medicaid is designed to provide affordable health coverage to low-income individuals and families, the varying income limits by state create significant disparities in access. Whether you qualify depends not just on your income but on where you live. To determine eligibility, start by identifying your state’s specific income threshold, consider household size, and explore resources like healthcare.gov or your state’s Medicaid website. Understanding these nuances is the first step toward securing the coverage you need.

Top Health Insurance Providers Offering Coverage in Pennsylvania: A Comprehensive Guide

You may want to see also

Explore related products

![]()

ACA Subsidies: Higher incomes reduce premium tax credits, increasing out-of-pocket insurance costs

The Affordable Care Act (ACA) provides premium tax credits to help lower-income individuals and families afford health insurance. However, as income rises, these subsidies decrease, leading to a sharp increase in out-of-pocket costs for premiums. This phenomenon, often referred to as the "subsidy cliff," creates a financial strain for those earning just above the eligibility threshold. For example, in 2023, a family of four earning up to $100,000 annually may qualify for reduced subsidies, but once their income exceeds this level, they could face a sudden jump in insurance costs, sometimes by thousands of dollars. This dynamic highlights the delicate balance between income and affordability in the ACA framework.

To understand the impact, consider a single individual earning $50,000 a year. At this income level, they might receive a substantial premium tax credit, reducing their monthly premium to a manageable amount. However, if their income increases to $52,000, they could lose a significant portion of that subsidy, causing their premium to spike. This scenario illustrates how modest income increases can disproportionately affect health insurance affordability. It’s not just about crossing the eligibility threshold but also about the incremental reductions in subsidies as income climbs.

For those nearing the subsidy cliff, strategic financial planning can mitigate the impact. One approach is to maximize pre-tax contributions to retirement accounts, such as a 401(k) or IRA, which can lower taxable income and potentially preserve subsidy eligibility. Another tactic is to explore health savings accounts (HSAs) if enrolled in a high-deductible health plan, as contributions reduce taxable income while offering tax-free savings for medical expenses. Additionally, individuals should carefully review their income projections annually during open enrollment to anticipate changes in subsidy eligibility and plan accordingly.

A comparative analysis reveals that the subsidy cliff disproportionately affects middle-income households, who may earn too much for substantial subsidies but not enough to comfortably afford unsubsidized premiums. For instance, a family of three earning $80,000 might face a premium increase of $300 or more per month if their income rises just $5,000. This contrasts with lower-income households, who receive more generous subsidies, and higher-income households, who can absorb the full cost of premiums. Policymakers have proposed solutions, such as smoothing the subsidy phase-out or raising income thresholds, but these changes remain under debate.

In practical terms, individuals should use the ACA’s subsidy calculator during open enrollment to estimate their eligibility and potential costs based on projected income. If nearing the subsidy cliff, they might consider part-time work or consulting arrangements to cap income temporarily. Alternatively, exploring employer-sponsored insurance, if available, can bypass ACA subsidies altogether. While these strategies require careful planning, they underscore the importance of understanding how income fluctuations directly impact health insurance affordability under the ACA.

Aspen Dental: EmblemHealth Medicaid Insurance Coverage Options

You may want to see also

Explore related products

![]()

Employer Coverage: Low-wage jobs often lack health benefits, leaving workers uninsured

Low-wage workers in the United States face a stark reality: their jobs often exclude them from employer-sponsored health insurance, the most common coverage source for Americans. This exclusion isn’t merely a gap in benefits—it’s a systemic barrier that traps millions in financial vulnerability. Consider this: nearly 28% of workers in the bottom income quartile lack employer-sponsored insurance, compared to just 8% in the top quartile, according to the Kaiser Family Foundation. Industries like retail, food service, and hospitality, which dominate the low-wage sector, offer health benefits to fewer than 40% of their employees. For a worker earning $15 per hour, the cost of contributing to an employer plan—often $300 to $500 monthly for individual coverage—can consume over 10% of their gross income, making it unaffordable.

The absence of employer coverage forces low-wage workers into a precarious position. Without access to subsidized plans through work, they must navigate the individual market, where premiums average $456 per month for a benchmark plan. For a family of four earning $30,000 annually, this expense is unsustainable, especially when coupled with high deductibles averaging $4,000. Medicaid, while a lifeline, isn’t universally available; in states that haven’t expanded Medicaid under the Affordable Care Act, workers earning above the poverty line ($14,580 for an individual in 2023) but below the subsidy threshold ($20,385) fall into the "coverage gap," leaving them uninsured. This gap disproportionately affects workers in Southern states, where 9% of adults are uninsured due to restrictive Medicaid policies.

Employers often justify excluding health benefits by citing profit margins, but this rationale overlooks the long-term costs of an unhealthy workforce. Turnover rates in low-wage jobs average 73% annually, partly due to inadequate benefits. A study by the National Bureau of Economic Research found that offering health insurance reduces turnover by 25%, increasing productivity and saving employers up to $1,200 per retained worker annually. Yet, only 35% of firms with fewer than 50 employees provide health benefits, compared to 96% of large firms. Policymakers could incentivize coverage by expanding tax credits for small businesses or mandating benefits for part-time workers, but such measures remain politically contentious.

For low-wage workers, the lack of employer coverage demands proactive strategies. First, understand eligibility for Medicaid or Affordable Care Act subsidies; households earning up to 400% of the poverty line ($55,960 for an individual) qualify for premium tax credits. Second, explore health sharing ministries or short-term plans as temporary alternatives, though these lack comprehensive coverage. Third, negotiate with employers for non-insurance benefits like health savings account contributions or wellness programs. Finally, advocate for policy changes at the state level, such as Medicaid expansion or mandated benefits for part-time workers. While systemic change is slow, individual action can mitigate immediate risks.

The exclusion of low-wage workers from employer-sponsored health insurance isn’t just an economic issue—it’s a moral one. A society that allows essential workers to go uninsured undermines its own stability. Until employers and policymakers address this disparity, millions will remain one illness away from financial ruin. The solution requires a dual approach: incentivizing businesses to provide benefits and expanding public coverage options. Without both, the cycle of poverty and poor health will persist, costing us all more in the long run.

Top Indian Insurance Companies: A Comprehensive Guide to the Best Providers

You may want to see also

Explore related products

![]()

Medicare Limits: Early retirees with moderate incomes face gaps in coverage before eligibility

Early retirees often find themselves in a precarious position when it comes to health insurance. Those who leave the workforce before age 65, when Medicare eligibility begins, must navigate a complex landscape of private insurance options, often at a higher cost than employer-sponsored plans. For individuals with moderate incomes—typically between $40,000 and $75,000 annually—this transition can be particularly challenging. They earn too much to qualify for Medicaid in most states but not enough to comfortably afford private insurance premiums, deductibles, and out-of-pocket costs. This income bracket creates a coverage gap that leaves early retirees vulnerable to financial strain or inadequate care.

Consider the case of a 60-year-old who retires early with an annual income of $55,000. In states that haven’t expanded Medicaid, this individual may fall into the "coverage gap," earning too much for Medicaid but too little to afford private insurance without significant financial burden. Premiums for individual plans on the Affordable Care Act (ACA) marketplace can easily exceed $800 per month, and high-deductible plans often require thousands of dollars in out-of-pocket spending before coverage kicks in. Even with ACA subsidies, which phase out for individuals earning above 400% of the federal poverty level (approximately $56,000 for a single person in 2023), the cost remains prohibitive for many in this income range.

The problem is compounded by the fact that early retirees are more likely to have chronic health conditions that require ongoing care. For example, a 62-year-old with hypertension or diabetes may face annual out-of-pocket costs exceeding $5,000, even with insurance. Without employer-subsidized coverage, these expenses can quickly erode savings intended for retirement. Moreover, COBRA continuation coverage, which allows individuals to stay on their employer’s plan for up to 18 months, is often cost-prohibitive, as the individual must pay the full premium plus an administrative fee.

To mitigate these challenges, early retirees should explore all available options. First, carefully evaluate ACA marketplace plans during open enrollment, paying close attention to subsidies and cost-sharing reductions. Second, consider health savings accounts (HSAs) if eligible, as they offer tax advantages for medical expenses. Third, investigate spousal coverage if a partner remains employed, though this may still be costly. Finally, part-time work with health benefits or relocating to a state with expanded Medicaid could provide temporary relief. While these strategies can help, they underscore the need for policy reforms to address the coverage gap for this demographic.

The takeaway is clear: early retirees with moderate incomes face a unique and often overlooked challenge in securing affordable health insurance. Without targeted solutions, this group will continue to struggle with financial insecurity and limited access to care during a critical transition period. Policymakers, employers, and individuals must work together to bridge this gap and ensure that health coverage remains accessible for all, regardless of retirement timing or income level.

After a Minor Accident: Is Insurance Info Enough?

You may want to see also

Explore related products

![]()

Coverage Gap: In some states, incomes too high for Medicaid but too low for subsidies

In the United States, individuals and families with incomes between 100% and 400% of the federal poverty level (FPL) are eligible for premium tax credits through the Affordable Care Act (ACA) marketplace. However, a significant coverage gap emerges for those with incomes below 100% of the FPL in states that have not expanded Medicaid. For example, in Texas, a single adult earning $13,590 annually (100% FPL in 2023) would qualify for Medicaid if the state had expanded it. Instead, they fall into the gap: too "wealthy" for Medicaid but too poor to afford ACA plans without subsidies, which begin at 100% FPL. This leaves them uninsured, often relying on emergency care or forgoing treatment altogether.

Consider a working parent in Florida earning $15,000 a year—above the state’s strict Medicaid eligibility threshold (roughly 30% FPL for parents) but below the subsidy threshold. ACA plans in their area might cost $300–$400 monthly, an impossible expense on their income. This gap disproportionately affects low-wage workers in industries like retail or food service, where employer-sponsored insurance is rare. The result? A paradox where earning slightly "too much" traps individuals in a no-coverage zone, exacerbating health disparities and financial instability.

To navigate this gap, affected individuals should first confirm their state’s Medicaid expansion status using tools like the Kaiser Family Foundation’s interactive map. If their state has not expanded Medicaid, they can explore local clinics offering sliding-scale fees or community health programs. For instance, Federally Qualified Health Centers (FQHCs) provide care on a pay-what-you-can basis, though this doesn’t replace comprehensive insurance. Additionally, tracking legislative updates on Medicaid expansion in their state could open future eligibility opportunities.

Advocacy is another critical step. Organizations like the Center on Budget and Policy Priorities provide resources for urging state lawmakers to close the coverage gap. Sharing personal stories through platforms like social media or local news outlets can humanize the issue, pressuring policymakers to act. While systemic change is slow, collective action has already spurred expansions in states like Missouri and Oklahoma, offering hope for those currently excluded.

Ultimately, the coverage gap is a policy failure, not a personal one. It highlights the fragmented nature of the U.S. healthcare system, where geography determines access. Until federal or state action bridges this divide, millions will remain uninsured, underscoring the need for both individual resilience and systemic reform. Practical steps, paired with advocacy, can mitigate but not eliminate the harm of this gap—a reminder that health coverage should be a right, not a privilege.

Dental Insurance for Me, Medical for My Wife: Can We?

You may want to see also

Frequently asked questions

There is no specific income level that inherently prevents someone from having health insurance. Eligibility for health insurance depends on factors like the type of insurance (e.g., employer-based, private, or government-funded), geographic location, and available subsidies or assistance programs.

High-income earners are generally not denied health insurance based on income alone. However, they may not qualify for government-subsidized plans like Medicaid or Affordable Care Act (ACA) marketplace subsidies, as these programs have income limits.

Earning a low income does not disqualify you from health insurance. In fact, individuals with lower incomes may qualify for Medicaid or receive premium tax credits through the ACA marketplace to make coverage more affordable.

Yes, Medicaid and ACA subsidies have income limits based on the Federal Poverty Level (FPL). For example, Medicaid eligibility typically caps at 138% of the FPL in states that expanded the program, while ACA subsidies are available for those earning up to 400% of the FPL.