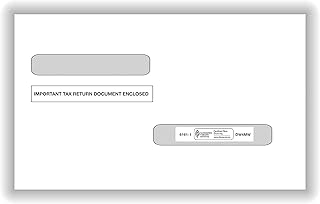

A 1099-R is a tax form sent out by insurance companies when a potentially taxable event occurs, such as a full surrender of a life insurance policy, a partial withdrawal, a loan, or a dividend transaction. The form is used to report how much income was earned from an annuity. It is important to note that while life insurance proceeds received as a beneficiary due to the death of the insured person are generally not taxable, any interest received is taxable and should be reported. The 1099-R form includes information such as the net cash surrender value, premiums paid, and the resulting taxable amount. This form can have implications for taxes, and it is recommended to consult a tax advisor before taking any action.

| Characteristics | Values |

|---|---|

| What is Form 1099-R? | A tax form sent out by insurance companies due to a potentially taxable event |

| Who does it apply to? | Life insurance policy and annuity contract owners |

| When is it sent? | By January 31 for the previous year |

| Why is it sent? | Due to a potentially taxable event, such as a full surrender, partial withdrawal, loan, or dividend transaction |

| What does it look like? | The form includes the applicable year and boxes for the taxable amount and other relevant information |

| How to access it? | Through an online account or by requesting it by mail |

Explore related products

What You'll Learn

![]()

Surrendering a life insurance policy

Whole and universal policies accrue cash value, making them the most likely option for surrender. The cash surrender value will depend on the type and age of the policy. Older policies are likely to have accrued significant cash value, while newer policies may not have accrued much at all. Surrendering a life insurance policy can rid you of the burden of a monthly premium and potentially net a fair amount of money for other investments or necessities.

There are a few things to consider before surrendering a life insurance policy. Firstly, if your policy isn't very old, you may incur surrender fees, which will reduce the amount of cash you receive. Secondly, the gain on your policy, however much it may be, will be taxed as income. While death benefits are tax-exempt, the cash received from surrendering a policy is taxable. It is important to consult a tax professional before making any decisions.

It is important to weigh the pros and cons of surrendering a life insurance policy before making a decision. Some pros include the ease and speed of the process, as well as the ability to get some money back. On the other hand, cons include minimal return, surrender fees, and limited options when it comes to negotiating the offer from the insurance company.

Tax Documents: Life Insurance Beneficiaries' Rights and Responsibilities

You may want to see also

Explore related products

![]()

Taxable events

Life insurance payouts are generally not taxable, but there are some circumstances in which they can be. Here are some examples of taxable events:

Term Life Insurance

- Interest on Installments: If the death benefit is paid out in installments, any interest that accumulates on those payments will be taxed as regular income.

- The Goodman Triangle: If three different individuals are involved in a life insurance policy (one person is the policy owner, another is the insured, and a third is the beneficiary), the IRS could view the death benefit as a gift from the policy owner to the beneficiary, triggering a gift tax if the amount exceeds the annual exclusion limit.

- Selling the Policy: If you sell your policy for more than what you've paid in premiums, the gain on that amount could be taxed.

- Death Benefit and Estate Taxes: If you own a term life insurance policy when you pass away, the death benefit becomes part of your taxable estate. This could push your estate's total value above the federal estate tax exemption, triggering estate taxes.

Permanent Life Insurance

- Withdrawing More Than Your Cost Basis: Withdrawing more than the total amount of premiums you've paid into the policy is considered taxable income and will need to be reported.

- Policy Lapse with Outstanding Loans: If your policy lapses and there are any outstanding loan amounts that exceed what you've paid into the policy, this will be treated as taxable income by the IRS.

- Surrendering the Policy: If the cash surrender value of the policy is higher than the amount of premiums you've paid, the excess is taxable as ordinary income.

- Participating Whole Life Policy: If you have a participating whole life insurance policy that pays dividends, any interest earned on those dividends is considered taxable income and must be reported.

Whole Life Insurance Dividends: Annual or Monthly Payouts?

You may want to see also

Explore related products

![]()

Calculating taxable amounts

The 1099-R form is used to report distributions from profit-sharing or retirement plans, individual retirement arrangements (IRAs), annuities, pensions, insurance contracts, survivor income benefit plans, permanent and total disability payments under life insurance contracts, and charitable gift annuities. This form is typically sent out by January 31 for the previous year.

Box 1: Gross Distribution

This box shows the total amount of the distribution before any deductions for loans or loan interest. This number may differ from the policy's net surrender value. It includes:

- Full surrenders of life insurance policies or annuity contracts

- Partial withdrawals from life insurance policies or annuity contracts

- Loans taken out against life insurance policies or annuity contracts

- Dividends received from life insurance policies or annuity contracts

Box 2a: Taxable Amount

To calculate the taxable amount, subtract the employee contributions or insurance premiums (Box 5) from the gross distribution (Box 1). This will give you the total earnings or profits on the insurance policy or annuity contract for that year. It's important to note that this amount may be 0, as not all distributions are taxable.

Box 5: Employee Contributions or Insurance Premiums

For traditional products, this is the difference between the amount of premiums paid into the policy/contract and the value of the dividends credited. If the dividends credited exceeded the premiums paid, this box will show a negative amount. For variable products, this box will show the total amount paid into the policy/contract, excluding any rider premiums.

Box 7: Distribution Code(s)

This box contains one or more codes that identify the type of distribution the policy/contract owner received. Each type of distribution will be reported on a separate Form 1099-R.

Other Boxes

- Box 3 reports interest income earned during the previous year.

- Box 4 reports any early withdrawal penalty.

- Box 6 reports federal income tax withheld.

- Box 10 reports the amount allocable to an in-plan Roth rollover within the past 5 years.

Life Insurance Options After Skin Cancer

You may want to see also

Explore related products

![]()

Interest income

If you own a life insurance policy, the receipt of a 1099-R form typically indicates a taxable event, such as a full surrender, partial withdrawal, loan, or dividend transaction. In the context of life insurance, interest income refers to the interest earned on the cash value of the policy. This interest income is taxable and must be reported to the Internal Revenue Service (IRS).

The 1099-R form helps you calculate the taxable amount associated with these events. It includes information such as the gross distribution (Box 1) and any employee contributions or insurance premiums (Box 5). By subtracting Box 5 from Box 1, you can determine the taxable amount (Box 2a). This calculation allows you to identify the portion of the distribution that is subject to taxation.

It's important to note that life insurance proceeds received as a beneficiary due to the death of the insured person are generally not considered taxable income and don't need to be reported. However, any interest income accrued on the life insurance policy is taxable. This distinction is crucial, as it ensures that the beneficiary is not burdened with taxes on the actual insurance payout but is responsible for paying taxes on any interest earned.

Additionally, the 1099-R form also captures other relevant information related to the life insurance policy or annuity contract. This includes details such as distribution codes, early withdrawal penalties, federal income tax withheld, and backup withholding information. These elements provide a comprehensive overview of the taxable events and associated calculations for the policyholder or contract owner.

Whole Life Insurance: Halal or Haram?

You may want to see also

Explore related products

![]()

Required distribution

Form 1099-R is used to report the distribution of retirement benefits such as pensions and annuities. If you received a distribution of $10 or more from your retirement plan, you should receive a copy of Form 1099-R.

Required Minimum Distributions (RMDs)

The age for RMDs was increased to 73 by the SECURE 2.0 Act of 2022. For more information, see RMDs.

Automatic Rollovers

Beginning January 1, 2024, the automatic rollover amount has increased from $5,000 to $7,000.

Corrective Distributions

Certain corrective distributions are not subject to a 10% early distribution tax. Beginning on December 29, 2022, the 10% additional tax on early distributions does not apply to an IRA distribution made pursuant to the rules of section 408(d)(4), which consists of a contribution for that year and any earnings allocable to the contribution, as long as the distribution is made on or before the due date (including extensions) of the income tax return.

Distributions for Emergency Personal Expenses

For distributions made after December 31, 2023, an emergency personal expense distribution may be made from a 403(b) plan and is not subject to the 10% additional tax on early distributions. An emergency personal expense distribution is a distribution made from your applicable eligible retirement plan that is used for purposes of meeting unforeseeable or immediate financial needs relating to necessary personal or family emergency expenses. There are certain limits that apply for emergency personal expense distributions (one per calendar year, dollar limits of generally not more than $1,000, and limits on subsequent distributions). You may repay emergency personal expense distributions at any time during the 3-year period beginning on the day after the date on which you received the distribution.

Distributions to a Domestic Abuse Victim

For distributions made after December 31, 2023, a distribution to a domestic abuse victim may be made from a 403(b) plan and is not subject to the 10% additional tax on early distributions. A distribution to a domestic abuse victim is a distribution made from your applicable eligible retirement plan that is no greater than $10,000 (indexed for inflation) and is made during the 1-year period beginning on any date on which you are the victim of domestic abuse by a spouse or domestic partner. You may repay this distribution at any time during the 3-year period beginning on the day after the date on which you received the distribution.

Distributions to Terminally Ill Individuals

The exception to the 10% additional tax for early distributions is expanded to apply to distributions made to terminally ill individuals on or after December 30, 2022.

How to Cancel Your Aviva Life Insurance Policy

You may want to see also

Frequently asked questions

A 1099-R is a tax form sent out by insurance companies when a potentially taxable event occurs, such as a full surrender of a life insurance policy, a partial withdrawal, a loan, or a dividend transaction.

The 1099-R form will have the applicable year on it.

Surrendering a life insurance policy means that you have agreed to take a cash payout instead of the death benefit. The insurance company assigns a value to your policy, which is the amount you will receive upon surrender.

You can generally expect a tax on the amount of money received minus the policy basis. These taxable gains can add to your tax burden, so consult a tax advisor before surrendering your policy.

The taxable amount will be reflected on the form, but if you want to calculate it beforehand, the formula is: (Net cash surrender value) – (premiums you paid) = (taxable amount).