An auto insurance referral is when an existing client of an insurance company provides the name and contact information of a potential customer who may be interested in purchasing insurance. This is a powerful tool for insurance companies to generate new business from an existing pool of customers. Referral programs can be applied to any form of insurance, including auto insurance. These programs are a great way to encourage and track word-of-mouth recommendations, which are highly trusted by consumers. Auto insurance companies may offer incentives such as cash, gift cards, or discounts to encourage referrals.

| Characteristics | Values |

|---|---|

| Definition | When an existing client of an insurance company provides the name and contact information of a potential customer who may be interested in purchasing insurance from the company |

| How it works | The level of service creates a great experience for customers, prompting them to tell their friends about it. Insurance companies can also motivate customers to refer new clients by offering incentives such as gift cards, bonuses, or finder's fees. |

| Benefits | Referrals are a coveted way to gain business as they are powered by word-of-mouth and have a higher chance of becoming customers. Referrals can also lead to multi-line policies, resulting in more value and income for the insurance agency. |

| Referral fee | A bonus, finder's fee, or other types of payment offered to customers for sending new referrals. |

| Referral form | A way to track incoming leads referred by existing customers, which can be done through a free Google Form or a spreadsheet program like Excel or Google Sheets. |

| Tools for referral programs | Spreadsheet programs, calendar platforms, social media, email signatures, and newsletters. |

| Best practices | Providing excellent customer service, showing a genuine interest in clients, and regularly checking in with them. |

Explore related products

What You'll Learn

![]()

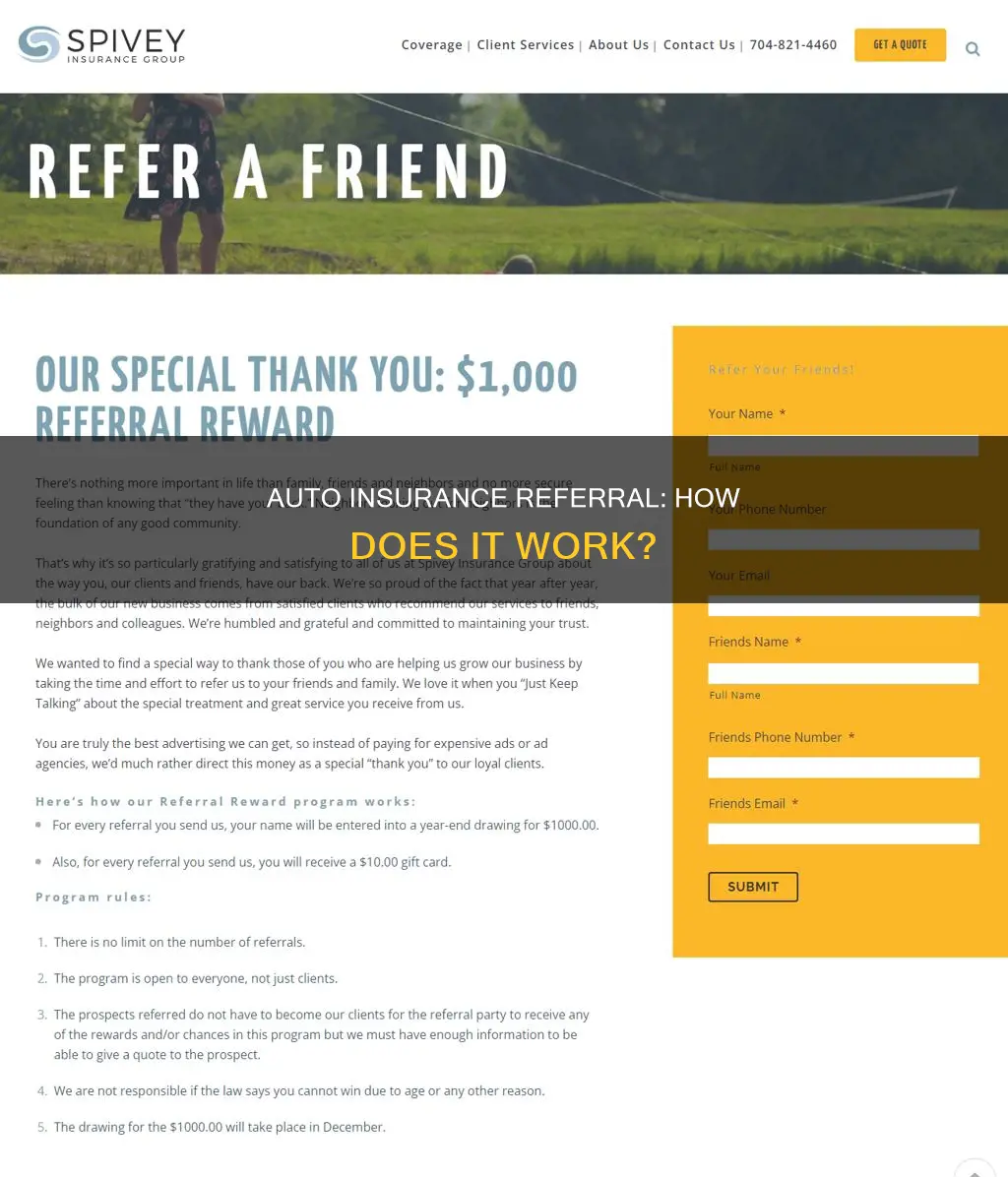

Referral reward programs

An auto insurance referral, or simply a "referral" in the insurance industry, occurs when an existing client provides the name and contact information of a potential customer who may be interested in purchasing insurance from the same company. Insurance companies incentivize customers to make referrals by offering rewards, such as gift cards, monetary bonuses, or discounts.

- Build Trust: The foundation of a successful referral program is built on trust and positive customer experiences. Insurance companies must provide excellent service, expertise, and customer support to encourage clients to recommend their services to others.

- Motivate Customers: Happy and satisfied customers are more likely to spread the word about their positive experiences. However, it is essential to provide additional incentives to motivate customers to actively refer their friends and family.

- Recognize Efforts: Rewarding customers for their referrals is a crucial aspect of the program. Rewards can vary, including gift cards, monetary bonuses, discounts on future purchases, or other incentives. Some companies may even offer rewards to both the referrer and the person being referred.

- Digital Automation: Developing a digital component to the referral program can streamline the process. This could include creating a dedicated webpage or landing page on the company's website, where clients can submit referrals online. Additionally, utilizing tools like QR codes can bridge the gap between physical marketing materials and the digital world, making it convenient for customers to provide referrals.

- Recapture Time: By automating the referral process and utilizing digital tools, insurance companies can free up time for their staff. This allows them to focus on more complex tasks, such as relationship-building and providing personalized insurance experiences, which can further enhance their referral network.

It is important to note that the value and structure of the referral rewards program should be customized based on the company's business objectives, cost per acquisition (CPA) benchmarks, and local laws regarding referral payments.

South Carolina Auto Insurance Requirements: Understanding the Law

You may want to see also

Explore related products

![]()

Referral fees

In most states, insurance agents can offer referral fees or gifts, such as gift cards, cash, or event tickets, to customers for referring new business. These referral incentives are typically allowed as long as they comply with state laws and do not affect the client's policy. The National Association of Insurance Commissioners (NAIC) has adopted the Producer Licensing Model Act (PLMA), which provides uniformity in statutory language related to agent and broker conduct. The PLMA allows insurers or insurance producers to pay commissions, service fees, or other valuable consideration to persons who do not sell, solicit, or negotiate insurance in a particular state, as long as it does not violate any applicable state laws.

It is important to note that paying referral fees to another licensed agent is generally not permitted, as it would be considered "commission splitting." Additionally, unlicensed individuals must not "solicit" insurance, which means they cannot attempt to sell insurance or urge a prospect to apply for coverage from a particular company.

The specific regulations and laws regarding referral fees can differ from state to state. For example, in New York and Texas, referral fees are allowed as long as they are not contingent on the sale of a policy, and the referring party does not discuss specific policy terms and conditions. In Pennsylvania, referral fees for insurance for personal, family, or household use are limited to a one-time, nominal fee that is not dependent on the actual sale of insurance.

Overall, referral fees are a common practice in the insurance industry, but it is crucial for agents to be aware of and comply with the relevant laws and regulations in their state to avoid any legal issues.

Kayak Conundrum: Unraveling Auto Insurance Coverage for Strapped Watercraft

You may want to see also

Explore related products

$10.6 $15.95

$18.43 $19.95

![]()

Referral forms

Understanding Referral Forms

Components of a Referral Form

A typical referral form will include fields for the referrer's information, such as their name, contact details, and policy number. It will also have sections for the prospect's details, including their full name, phone number, email address, and any other relevant information that can help the insurance company initiate contact. Some referral forms may also include additional fields to capture the prospect's insurance needs, vehicle information, or other specifics that can aid in tailoring the insurance offering to their requirements.

Benefits of Using Referral Forms

- Systematic Lead Tracking: Referral forms provide a structured approach to gathering and organizing lead information. This helps insurance agents stay organized and efficiently follow up with potential new customers.

- Streamlined Data Management: By using referral forms, insurance companies can easily manage and store customer data in digital formats, such as Google Forms and spreadsheets, eliminating the need for cumbersome paper trails.

- Enhanced Customer Experience: Referral forms demonstrate a commitment to serving both existing and potential customers. They show that the insurance company values the referrals provided by existing customers and is proactive in reaching out to prospects.

- Improved Lead Conversion: Referral forms enable insurance agents to receive warm leads, as the prospects have been introduced through existing customers. This increases the likelihood of converting these leads into actual policyholders.

Best Practices for Referral Forms

To maximize the effectiveness of referral forms, consider the following best practices:

- Simplicity and Convenience: Keep the referral form concise and straightforward. Make it easily accessible through digital channels, such as your website or mobile app, to encourage customers to submit referrals without hassle.

- Clear Instructions: Provide clear and concise instructions on how to fill out the referral form. Ensure that customers understand the purpose of the form and the benefits of providing referrals.

- Incentives and Rewards: Consider implementing a referral reward program to motivate customers to submit referral forms. This could be in the form of gift cards, account credits, or other incentives to show your appreciation for their referrals.

- Regular Follow-up: Stay in touch with your existing customers and gently remind them about the referral program. This can be done through email newsletters, social media campaigns, or even personal phone calls to show your appreciation and encourage their continued support.

In conclusion, referral forms are a crucial component of a well-structured auto insurance referral program. They facilitate lead generation, streamline customer data management, and strengthen relationships with existing customers. By implementing best practices and utilizing digital tools effectively, insurance companies can optimize their referral processes and drive sustainable business growth.

Foremost Auto Insurance: The Good, the Bad, and the Unique

You may want to see also

Explore related products

![]()

Referral marketing techniques

An auto insurance referral is when an existing client of an insurance company provides the name and contact information of a potential customer who may be interested in purchasing insurance from them. This is a powerful strategy that encourages existing customers to promote a brand within their networks, turning them into advocates for the business.

- Asking for Referrals at the Right Time: Asking for referrals when customers are happiest with your products or services is key. This could be right after checkout, after a repeat purchase, or when a customer gives direct positive feedback.

- Exceeding Customer Expectations: Going beyond customer expectations can help to generate more referrals. For instance, sending a surprise gift on a customer's birthday or performing an act of kindness in their time of need.

- Building a Brand Community: Creating a community around your brand can foster a sense of belonging and encourage customers to share their positive experiences with others. This can be done through social media content, user-generated content contests, or establishing an online group or forum.

- Offering Strategic Incentives: Incentives can be a powerful motivator for customers to refer others. These don't have to be expensive; they can include early access to new products, exclusive invites to webinars, store credits, discount coupons, or branded swag.

- Leveraging Social Media: With the average internet user spending up to 145 minutes on social media daily, tapping into this platform is crucial. Make it easy for customers to share your brand on social media and consider providing referral links that can be easily copied and pasted.

- Using Email Marketing: Email is a more personal and reliable way to promote your referral program and rewards. Include referral links or banners in your email signatures, thank-you confirmation emails, or company newsletters.

- Streamlining the Referral Process: Make sure the referral process is simple and easy for customers to complete. Break it down into a few easy steps and provide multiple referral options, such as via email and social media.

- Using Referral Links: Referral links are crucial for a successful referral program. They allow customers to easily share your website with their network and help you track referrals back to the person who made them.

- Considering Other Types of Referral Programs: In addition to customer referral programs, you can also explore employee referral programs or influencer/ambassador programs to reach a wider audience.

- Using Referral Software: Utilizing referral software can help automate and streamline your referral program. It makes it easier to design a trackable referral experience, distribute referral links, and instantly reward successful referrals.

By implementing these referral marketing techniques, you can effectively grow your auto insurance referral program and turn your customers into brand advocates.

Senior Auto Insurance: Getting Affordable Coverage

You may want to see also

Explore related products

![]()

Underwriting referrals

An underwriting referral is a regular part of auto insurance. It occurs when an insurance company needs more information before making a decision on whether to accept or deny coverage for a potential policyholder. This usually happens when the applicant presents a higher level of risk than what the company typically insures. The company will then request additional information or documentation to assess the risk before making a decision.

The underwriting team will review the policy, conduct an investigation, and assess whether the changes made to the policy align with the policy agreement. This process involves gathering information about the insured, such as the mileage of the vehicle, the number of drivers with access to it, the primary purpose of the vehicle, and any damage sustained during the year. The new information is then plugged into a computer that assesses risk and generates new rates.

Travelers 12-Month Auto Insurance: Year-Round Coverage and Peace of Mind

You may want to see also

Frequently asked questions

An auto insurance referral is when an existing client of an insurance company provides the name and contact information of a potential customer who may be interested in purchasing insurance from them.

Ideally, your level of service creates a great experience for customers, who then want to tell their friends about it. Sometimes, even with amazing service and happy customers, you still have to motivate current customers to refer you to their peers.

Referrals are the most coveted way to gain business in the sales world. They are powered by word-of-mouth, so they can be a cost-effective way to grow your business. Referred leads also have a higher chance of becoming customers.

An insurance referral fee is a way to motivate customers to send new referrals your way. This can be in the form of a bonus, finder's fee, or other types of payment, such as gift cards.

An insurance referral form is a way to track incoming leads referred from existing customers. It can be a free Google Form that clients fill out.