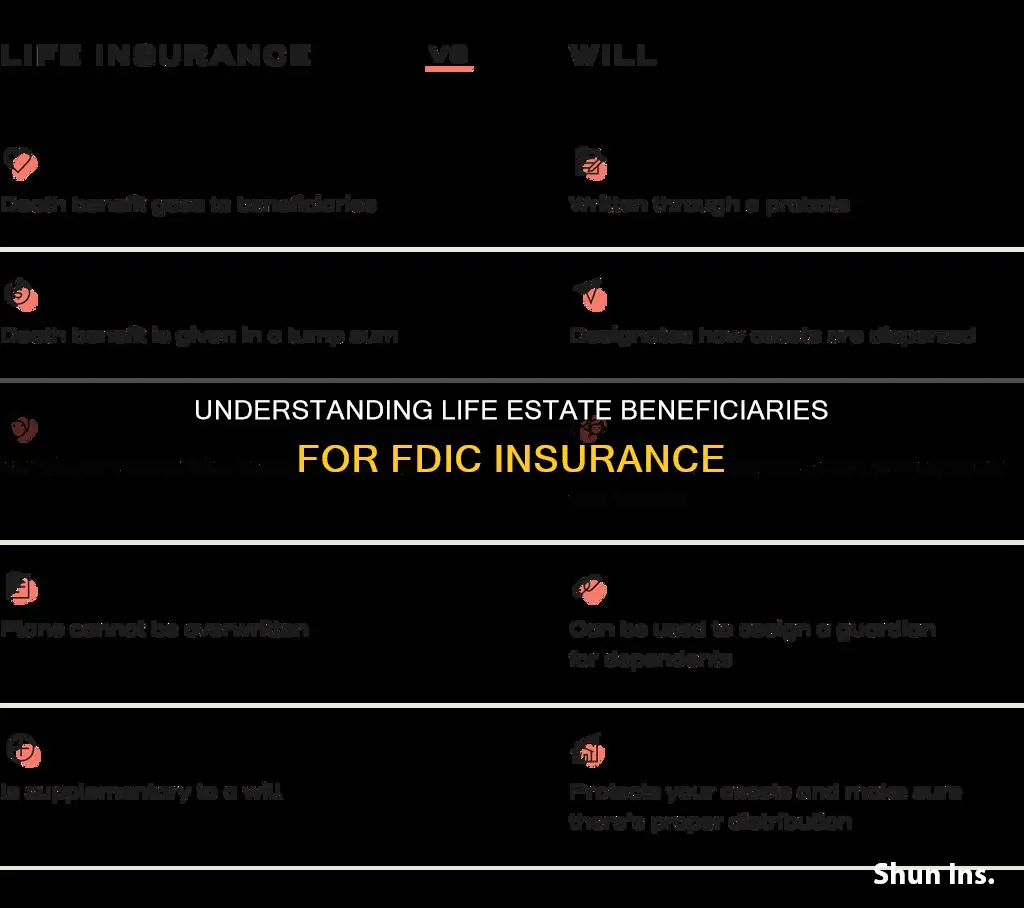

The Federal Deposit Insurance Corporation (FDIC) is an independent federal agency that protects depositors' funds in the event of a bank failure. FDIC insurance covers up to $250,000 per depositor, per insured bank, for each account ownership category. FDIC insurance does not cover investments such as stocks, bonds, or mutual funds. When it comes to Payable on Death (POD) accounts, also known as Totten trusts or informal trust accounts, FDIC insurance coverage is determined by the number of beneficiaries and the amount of money in the account. Each beneficiary is insured up to $250,000, and this coverage is separate from the account holder's other accounts at the same bank.

| Characteristics | Values |

|---|---|

| Type of beneficiary | Life estate beneficiary |

| Definition | A beneficiary who has the right to receive income from the trust or to use trust deposits during their lifetime, with the remaining trust deposits going to other beneficiaries after their death |

| Insurance coverage | Up to $250,000 for each unique beneficiary |

| Maximum insurance coverage | $1,250,000 for five or more unique beneficiaries |

Explore related products

$17.54 $19.99

What You'll Learn

- Life estate beneficiaries are entitled to insurance coverage of up to $250,000

- The FDIC covers up to $250,000 per depositor

- FDIC insurance covers checking accounts, savings accounts, money market deposit accounts, and more

- FDIC insurance does not cover investments in stocks, bonds, or mutual funds

- FDIC-insured institutions include most US banks and savings associations

![]()

Life estate beneficiaries are entitled to insurance coverage of up to $250,000

The FDIC recognises different ownership categories, which can impact insurance coverage. For instance, a single account is owned by one person with no beneficiaries, while a joint account is owned by two or more people with no beneficiaries. In the case of a trust account, the owner can be insured for up to $250,000 per unique eligible beneficiary, with a maximum of $1,250,000 for five or more beneficiaries.

A life estate beneficiary is a specific type of beneficiary within the trust account ownership category. They are beneficiaries who have the right to receive income from the trust or use trust deposits during their lifetime, after which the remaining trust deposits are passed on to other beneficiaries. For example, in the case of a living trust, a husband can set up a trust that gives his wife a life estate interest in the trust deposits, with their children receiving the remaining deposits after the wife's death. In this scenario, the maximum insurance coverage would be calculated as 1 owner x $250,000 x 3 different beneficiaries = $750,000.

It is important to note that FDIC insurance does not cover investments such as stocks, bonds, mutual funds, life insurance policies, or annuities. Additionally, the coverage is provided per depositor, per insured bank, so deposits in different banks are insured separately.

Understanding PA's Tax on Employer-Provided Group Term Life Insurance

You may want to see also

Explore related products

![]()

The FDIC covers up to $250,000 per depositor

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that protects bank depositors against the loss of their insured deposits in the event that an FDIC-insured bank or savings association fails. FDIC insurance is backed by the full faith and credit of the United States government. Since the FDIC began operations in 1934, no depositor has ever lost a penny of their FDIC-insured deposits.

The standard maximum deposit insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. This means that if you have deposits in different account categories at the same FDIC-insured bank, your insurance coverage may be more than $250,000, if all requirements are met.

The FDIC does not insure all financial products at a bank. FDIC deposit insurance only covers certain deposit products, such as checking and savings accounts, money market deposit accounts (MMDAs), and certificates of deposit (CDs).

The FDIC does not insure:

- Life insurance policies

- Municipal securities

- Safe deposit boxes or their contents

- US Treasury bills, bonds, or notes

The FDIC covers up to at least $250,000 per depositor. FDIC insurance covers the traditional types of bank deposit accounts: checking accounts, savings accounts, money market deposit accounts, certificates of deposit, and certain retirement accounts.

FDIC insurance does not cover investments in stocks, bonds, mutual funds or money market mutual funds, life insurance policies, or annuities.

If you have accounts at different FDIC-insured banks, the limit applies at each bank: $250,000 per depositor for each account ownership category.

Adjustable Life Insurance: Cash Value and Benefits Explained

You may want to see also

Explore related products

![]()

FDIC insurance covers checking accounts, savings accounts, money market deposit accounts, and more

A life estate beneficiary is a beneficiary who has the right to receive income from a trust or to use trust deposits during their lifetime, while other beneficiaries receive the remaining deposits after the life estate beneficiary dies.

The Federal Deposit Insurance Corporation (FDIC) provides deposit insurance to protect your money in the event of a bank failure. FDIC insurance covers various types of deposit accounts held at an insured bank, including checking accounts, savings accounts, money market deposit accounts, and certificates of deposit (CDs). Each depositor is insured up to at least $250,000 per insured bank and ownership category.

Here's a more detailed overview of what FDIC insurance covers:

- Checking Accounts: FDIC insurance covers funds held in checking accounts at insured banks.

- Savings Accounts: Your savings deposits are protected by FDIC insurance at insured banks.

- Money Market Deposit Accounts (MMDAs): These accounts are included in the FDIC coverage, offering protection for your deposits.

- Certificates of Deposit (CDs): FDIC insurance also covers your investments in certificates of deposit at insured banks.

By insuring these types of accounts, the FDIC provides protection for a wide range of depositors, ensuring that their money is safe even in the unlikely event of a bank failure. It's important to note that FDIC insurance does not cover all financial products, such as investments in stocks, bonds, mutual funds, or life insurance policies. However, by understanding what is covered, depositors can have peace of mind knowing that their money is protected up to the specified limits.

Terminal Diagnosis: Life Insurance Options and Availability

You may want to see also

Explore related products

![]()

FDIC insurance does not cover investments in stocks, bonds, or mutual funds

The Federal Deposit Insurance Corporation (FDIC) is an independent federal agency that ensures the availability of deposited funds after a bank failure. The FDIC covers up to at least $250,000 per depositor, per insured bank, per ownership category.

FDIC insurance covers the following types of bank deposit accounts:

- Checking accounts

- Savings accounts

- Money market deposit accounts

- Certificates of deposit

- Certain retirement accounts

However, FDIC insurance does not cover investments in stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if these investments are purchased at an insured bank. This is because the FDIC only insures deposits, not investments.

- Stocks

- Bonds

- Mutual funds

- Money market mutual funds

- Treasury securities

- Life insurance policies

- Annuities

It is important to note that non-bank companies are never FDIC-insured, even if they partner with insured banks. Therefore, money sent to a non-bank company is not FDIC-insured unless and until the company deposits it in an insured bank.

While FDIC insurance does not cover investments in stocks, bonds, or mutual funds, there are other forms of protection for these types of investments. For example, the Securities Investor Protection Corporation (SIPC) is a non-government entity that protects investors from loss if their brokerage firm fails. The SIPC insures investors up to $500,000, with a $250,000 cash sub-limit. The SIPC covers investments in stocks, bonds, options, Treasury securities, and CDs, in addition to mutual funds.

Understanding Life Insurance: Face Value and Payouts Explained

You may want to see also

Explore related products

![]()

FDIC-insured institutions include most US banks and savings associations

The Federal Deposit Insurance Corporation (FDIC) is an independent agency created by the US Congress to maintain stability and public confidence in the nation's financial system. The FDIC insures deposits and covers up to at least $250,000 per depositor, per bank, per ownership category. FDIC-insured institutions include most US banks and savings associations.

The FDIC covers the traditional types of bank deposit accounts: checking accounts, savings accounts, money market deposit accounts, certificates of deposit, and certain retirement accounts. It does not cover brokerage firms, investments in stocks, bonds, mutual funds or money market mutual funds, life insurance policies, or annuities.

The FDIC provides deposit insurance to protect your money in the event of a bank failure. Your deposits are automatically insured to at least $250,000 at each FDIC-insured bank. Coverage is automatic when you open one of the types of accounts mentioned above at an FDIC-insured bank.

The FDIC directly supervises more than 5,000 banks and savings associations. Since the FDIC began operations in 1934, no depositor has ever lost a penny of FDIC-insured deposits.

Trusts and Life Insurance: California's Unique Rules

You may want to see also

Frequently asked questions

A life estate beneficiary is a beneficiary who has the right to receive income from a trust or to use trust deposits during their lifetime. Other beneficiaries receive the remaining trust deposits after the life estate beneficiary dies.

The FDIC calculates insurance coverage for a trust with a life estate beneficiary by multiplying the number of owners by the number of beneficiaries by $250,000. The maximum insurance coverage per owner for all trust accounts is $1,250,000.

Yes, you can have multiple life estate beneficiaries. However, if you have more than five beneficiaries, the maximum insurance coverage will still be $1,250,000 per owner.

If a life estate beneficiary dies, there may be a successor beneficiary who will receive the remaining trust deposits. The FDIC will consider this successor beneficiary when calculating deposit insurance coverage.

To be considered an eligible beneficiary for FDIC insurance purposes, the beneficiary must be a living person, a charitable organization, or a non-profit entity recognized by the Internal Revenue Code.