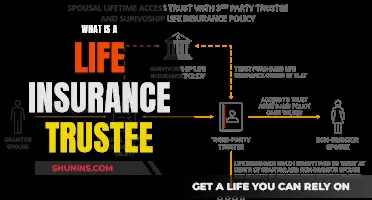

A life insurance trust is a legal agreement that allows a third party to manage the death benefit from a life insurance policy. A trust ensures that the policy's death benefit is distributed to beneficiaries according to the policyholder's wishes. It also exempts the funds from probate and may reduce any estate tax owed. Life insurance trusts are commonly used by individuals with a high net worth, as well as parents who want to structure the benefit payments made to their children.

Explore related products

$24.95 $24.95

What You'll Learn

![]()

Irrevocable Life Insurance Trusts (ILITs)

With an ILIT, a trustee (someone other than the insured) takes ownership of the policy and pays the premiums, usually with funds contributed to the ILIT by the grantor. Upon the death of the insured, the life insurance proceeds will be paid to the ILIT, to be held and distributed to the beneficiaries according to the terms of the trust document.

One of the key advantages of an ILIT is estate tax reduction. By keeping the insurance proceeds out of the insured's estate, there is typically no estate tax liability associated with those proceeds. ILITs also provide liquidity for the payment of estate taxes, debts, and administration expenses. In addition, ILITs offer protection from the grantor's creditors, ex-spouses, or bankruptcy situations.

It is important to note that an ILIT is irrevocable, meaning the grantor cannot easily change the terms of the trust. Contributions to the ILIT may also constitute reportable gifts, which could result in gift tax consequences. Another consideration is the loss of policy control and access; once a grantor transfers an existing life insurance policy to an ILIT, they give up control over the policy and can no longer make withdrawals or borrow against its cash value.

Overall, ILITs can be a valuable tool for individuals with substantial wealth who are seeking to reduce estate taxes and preserve their legacy for future generations.

Understanding Taxable Benefits for Life Insurance

You may want to see also

Explore related products

![]()

Revocable Life Insurance Trusts (RLITs)

RLITs are also beneficial if you have a child with special needs who will require long-term care. A revocable special needs trust holds funds for your child and defines when and how that money should be spent. Life insurance proceeds aren't taxed as they go into the trust, and the trustee manages those funds (along with any other assets in the trust) and pays money out according to your wishes.

RLITs can be funded with various assets, including cash, stocks, bonds, and other investments. However, permanent life insurance policies such as whole life or universal life are often preferred as they provide a guaranteed death benefit and can accumulate cash value over time, making them a more reliable choice for funding a trust.

It is important to note that setting up a life insurance trust is much more complicated than writing a will, and it is recommended to hire an attorney who specializes in trusts to set one up.

Credit Card Debt: Impact on Life Insurance Beneficiaries?

You may want to see also

Explore related products

![]()

Tax advantages

A life insurance trust agreement is a legal agreement that allows a third party to manage the death benefit from a life insurance policy. It ensures that the death benefit is distributed to beneficiaries according to the wishes of the insured. It also exempts the funds from probate and may reduce any estate tax owed.

Life insurance trusts can have significant tax advantages, both during the grantor's lifetime and after their death. Here are some key tax advantages of life insurance trust agreements:

- Mitigating Estate Taxes: The trust owns the insurance policy, so it can be excluded from the taxable estate, thereby reducing or eliminating federal estate taxes.

- Eliminating Gift Taxes: A life insurance trust agreement allows the trust transfer to be treated as a present gift, which may not be taxed, as opposed to a future gift, which could be taxed.

- Preserving Government Benefits: Life insurance trust agreements can help preserve eligibility for beneficiaries who receive asset-dependent benefits from the state or federal government.

- Shielding from Tax Penalties: The policy's cash value and death benefits may not be taxed when placed in a life insurance trust.

- Income Tax Exemption: Beneficiaries typically receive the insurance proceeds from a life insurance policy income tax-free. However, the payout may be subject to estate tax. By placing the policy in a trust, the proceeds can be sheltered from estate taxes, preventing them from pushing the estate value over the exemption threshold.

- Reduced Estate Tax: The death benefit of the life insurance policy may be subject to estate tax after the grantor's death. However, if the trust is properly structured, the death benefit can be excluded from the grantor's estate, reducing the tax liability.

Life Insurance: Group Policies and Estate Tax Implications

You may want to see also

Explore related products

![]()

Estate planning advantages

A life insurance trust agreement is a legal arrangement where a third party, known as a trustee, holds and manages the death benefit from a life insurance policy on behalf of the beneficiaries. The two basic types of life insurance trusts are irrevocable and revocable.

Mitigating Estate Taxes:

The trust owns the insurance policy, excluding it from your taxable estate and shielding your beneficiaries from estate taxes on the proceeds. This is especially beneficial for high-net-worth individuals whose estates exceed the federal estate tax threshold.

Eliminating Gift Taxes:

The trust transfer can be treated as a present gift, which may not be taxed, whereas a future gift likely would be.

Preserving Government Benefits:

An ILIT can help preserve eligibility for beneficiaries receiving asset-dependent benefits from the government.

Protecting Assets:

An ILIT can limit the amount of funds that creditors can pursue, protecting your assets.

Controlling Distributions:

Life insurance trusts allow the grantor to control when and how beneficiaries receive assets, ensuring your loved ones are taken care of per your wishes. For example, you can structure the release of funds to beneficiaries as they reach certain milestones.

Planning for Generational Legacies:

A life insurance trust can provide for future generations, including those not yet born, helping them inherit wealth in a tax-efficient manner.

Shielding from Tax Penalties:

The policy's cash value and death benefits may not be taxed when placed in a life insurance trust.

Probate Exemption:

Assets in a life insurance trust, including life insurance proceeds, are exempt from probate, avoiding delays and uncertainty in estate administration.

Special Needs Planning:

A revocable special needs trust can hold funds for a child with special needs, preserving their eligibility for essential government benefits.

Life Insurance: Asset or Liability?

You may want to see also

Explore related products

![]()

Disadvantages of Life Insurance Trusts

Life insurance trusts are a strategic way to manage and distribute life insurance proceeds, reduce taxes, and provide for heirs. However, there are several disadvantages to consider before setting up a life insurance trust.

Complexity and Cost

Setting up and managing a life insurance trust can be complicated and often requires legal assistance. There are also various initial costs associated with establishing a trust, such as legal fees for drafting the trust document and notary fees. Ongoing expenses, such as trustee fees and administrative fees for any updates or changes, may also be incurred.

Loss of Access and Control

Once a life insurance policy is placed in an irrevocable life insurance trust (ILIT), the grantor loses access to the policy's cash value and cannot make changes or cancel the trust. This can be a significant drawback if financial circumstances change and the cash value is needed.

Potential Tax Implications

While life insurance trusts can offer tax advantages, there are also potential tax implications to consider. For example, IRS rules state that if the grantor dies within three years of setting up an irrevocable trust, the trust can still be counted as part of their estate for tax purposes. Additionally, the transfer of the life insurance policy into the trust may be considered a gift and could use up a portion of the grantor's gift tax exemptions.

Limited Flexibility

Life insurance trusts offer less flexibility compared to other options for managing life insurance policies. Once the trust is established, the grantor typically cannot make changes to the beneficiaries or coverage. This lack of flexibility may be a disadvantage for those who prefer to have the option to make changes in the future.

Life Insurance: Legal Fees Coverage and Benefits

You may want to see also

Frequently asked questions

A life insurance trust agreement is a legal arrangement that allows a third party to manage the death benefit from a life insurance policy. It ensures that the benefit is distributed to beneficiaries according to the policyholder's wishes.

A life insurance trust agreement can provide several benefits. It can help shield beneficiaries from estate taxes on life insurance proceeds, preserving family wealth. It also ensures that loved ones are taken care of as intended and provides greater control over the distribution of assets. Additionally, it bypasses the probate process, avoiding delays and uncertainty.

Some potential downsides include the cost and complexity of setting up and maintaining the trust, as well as the loss of control over the policy once it is transferred to an irrevocable trust. There may also be tax implications, such as the three-year lookback period for irrevocable trusts, and the inability to make changes to the policy or trust.