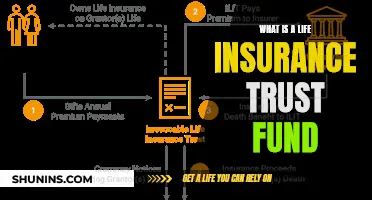

A life insurance trust is a legal agreement that allows a third party to manage the death benefit from a life insurance policy. It is a tool used in estate planning to protect assets and ensure financial security for beneficiaries. On the other hand, an individual retirement account (IRA) is a tax-advantaged savings account that individuals use to save for retirement. Both options offer distinct benefits and considerations for individuals looking to secure their financial future and that of their loved ones.

| Characteristics | Life Insurance Trust | IRA |

|---|---|---|

| Description | A legal vehicle that allows a third party (trustee) to hold and manage assets for beneficiaries. | A long-term, tax-advantaged savings account for individuals with earned income. |

| Purpose | Estate planning and protecting assets and the financial future of beneficiaries. | Saving for retirement with tax advantages. |

| Ownership | The trust owns the insurance policy, and the trustee manages its benefits. | The individual who opens the account owns it. |

| Tax Implications | May be subject to income tax, gift tax, and estate tax. | Contributions may be tax-deductible, and distributions may be tax-free depending on the type of IRA. |

| Types | Irrevocable and revocable. | Traditional, Roth, SEP, and SIMPLE. |

| Beneficiaries | Beneficiaries receive funds according to the rules set in the trust agreement. | The individual who owns the account and, in some cases, their spouse. |

| Access to Funds | Funds are distributed to beneficiaries according to the terms of the trust. | Early withdrawal before a certain age may incur a tax penalty. |

| Ideal For | High-net-worth individuals and parents who want to structure benefit payments for their children. | Self-employed individuals and those who want to supplement their employer-sponsored retirement plans. |

Explore related products

$24.95 $24.95

$8.99

What You'll Learn

![]()

Life insurance trusts can be irrevocable or revocable

Irrevocable Life Insurance Trusts (ILITs):

Irrevocable life insurance trusts are trusts specifically designed to hold life insurance policies. Once you transfer ownership of your life insurance policy to an ILIT, you generally cannot make changes or revoke the trust. This type of trust offers several benefits. First, it removes the life insurance policy from your estate, reducing the value of your estate for tax purposes. This can be advantageous if you have a large estate that may be subject to estate taxes. Additionally, the proceeds from the life insurance policy are not included in the taxable estate of the beneficiary, providing them with a tax-free inheritance. ILITs also offer protection from creditors, ensuring that the death benefit remains secure and intended beneficiaries receive the maximum benefit. While ILITs offer significant advantages, it's important to carefully consider this option as the transfer is irreversible, and you will no longer have direct control over the policy or the trust.

Revocable Life Insurance Trusts:

On the other hand, revocable life insurance trusts offer more flexibility as they can be altered or revoked during the grantor's lifetime. This type of trust allows the grantor to retain control over the trust and make changes as needed. For example, the grantor can change the beneficiaries, adjust the distribution terms, or even dissolve the trust entirely. While the life insurance policy is held in the trust, the grantor can still access the cash value of the policy and borrow against it if needed. One key advantage of revocable trusts is that they provide a level of privacy and protection during the grantor's lifetime. However, it's important to note that revocable trusts do not offer the same level of tax benefits and asset protection as irrevocable trusts. The assets held in a revocable trust, including the life insurance policy, are still considered part of the grantor's taxable estate.

The choice between an irrevocable or revocable life insurance trust depends on your specific needs and goals. If you want to maximize tax benefits and asset protection, an irrevocable trust may be more suitable. On the other hand, if flexibility and control are more important to you, then a revocable trust might be the preferred option. It's always advisable to seek the guidance of a qualified estate planning professional to help you navigate the complexities and ensure your estate plan aligns with your unique circumstances and objectives.

Life Insurance: Your DIY Guide to Peace of Mind

You may want to see also

Explore related products

![]()

Life insurance trusts can reduce estate taxes

Life insurance trusts can be a powerful tool for reducing estate taxes, but it is important to understand the different types of trusts and their implications. The two main types of life insurance trusts are irrevocable life insurance trusts (ILITs) and revocable life insurance trusts (RLITs).

Irrevocable life insurance trusts are the most common type and offer significant tax advantages. When a life insurance policy is placed within an ILIT, the proceeds are excluded from the grantor's taxable estate, reducing potential estate taxes for beneficiaries. This is because the trust owns the insurance policy, and the death benefit is paid directly to the trust, not the grantor's estate. This structure also allows for greater control over how the insurance benefit is distributed to beneficiaries. However, it is important to note that ILITs cannot be changed or terminated once they are established, and there may be gifting implications if the policy has a large accumulated cash value.

On the other hand, RLITs offer more flexibility as they can be changed or cancelled by the grantor. However, assets in this type of trust remain part of the grantor's estate, and therefore, may be subject to federal and state estate taxes. RLITs become irrevocable upon the grantor's death or incapacitation, locking in their wishes at that time.

When deciding between an ILIT and RLIT, it is essential to consider your financial situation, goals, and the size of your estate. ILITs are particularly effective for those with substantial wealth as they provide a way to shield beneficiaries from estate taxes on life insurance proceeds, helping to preserve family wealth across generations. Additionally, ILITs can protect government benefits for beneficiaries and provide liquidity to help pay estate taxes and other debts.

While life insurance trusts offer tax advantages and estate planning benefits, there are also some potential drawbacks to consider. These include the cost of setting up and maintaining the trust, the complexity of the process, and the loss of control over the policy once it is transferred to an ILIT. It is always recommended to seek professional guidance from attorneys and financial advisors when considering a life insurance trust to ensure it aligns with your specific goals and complies with legal and tax requirements.

Life Insurance for Young Adults: What You Need to Know

You may want to see also

Explore related products

![On the Crises of 1837, 1847, and 1857, in England, France, and the United States: an Analysis and Comparison, by Ira Ryner. (In Nebraska. University. University Studies.) 1905 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![[5 Pack] Estate Sale Signs Set - 16 x 12 Inch Double-Sided Yard Signs With Arrows and Metal H Stakes - Property Sale Directional Signs - Weather-Proof](https://m.media-amazon.com/images/I/71vlCeOw-UL._AC_UY218_.jpg)

![]()

Life insurance trusts can avoid gift taxes

Life insurance trusts, specifically irrevocable life insurance trusts (ILITs), can help avoid gift taxes. This is because they allow the trust transfer to be treated as a present gift that may not be taxed, as opposed to a future gift that is.

When setting up an ILIT, the grantor typically creates and funds the trust. Gifts or transfers made to the trust are permanent. The trustee then manages the trust, and the beneficiaries receive the distributions. To avoid gift taxes, it is crucial that the trustee notifies the beneficiaries of the trust of their right to withdraw a share of the contributions for a 30-day period using a Crummey letter. After 30 days, the trustee can then use the contributions to pay the insurance policy premium. The Crummey letter qualifies the transfer for the annual gift tax exclusion by making the gift a present rather than a future interest, thus avoiding the need in most cases to file a gift tax return.

In 2025, an individual can give up to $19,000 a year to another individual without reporting it to the Internal Revenue Service (IRS). A married couple filing jointly can give an individual a combined $38,000 in 2025 without reporting it to the IRS. Anything more, and one must report the gift via Form 709. However, one does not need to pay taxes on the gifts unless the gift exceeds the lifetime gift exemption amount, which is $13.99 million in 2025.

It is important to note that the grantor should avoid any incident of ownership in the life insurance policy. Any premium paid should come from a checking account owned by the ILIT. If the grantor transfers an existing life insurance policy to the ILIT, there is a three-year lookback period in which the death benefit could be included in the grantor's estate.

Dementia and Life Insurance: What Are Your Options?

You may want to see also

Explore related products

![]()

Life insurance trusts can preserve government benefits

Life insurance trusts can be a critical component in estate planning, helping to protect assets and secure the financial future of loved ones. Trusts can be particularly beneficial for those with young or special-needs children, as they allow for control over how and when funds are distributed to beneficiaries. This can ensure that children receive financial support in a way that is in their best interests and help prevent them from spending their entire inheritance all at once.

One important advantage of life insurance trusts is their ability to preserve government benefits for beneficiaries. When a life insurance policy is owned by an irrevocable life insurance trust (ILIT), the proceeds from the death benefit are not considered part of the insured's estate. This means that the funds from the life insurance policy are not included when calculating the beneficiary's income for government benefit eligibility purposes. As a result, beneficiaries can continue to receive essential government aid, such as Social Security disability income or Medicaid, without interruption.

The trustee of an ILIT has the discretion to control distributions and ensure that they do not interfere with the beneficiary's eligibility for government assistance. This feature is especially relevant for beneficiaries who rely on means-tested government programs, as it allows them to maintain their eligibility while still having access to additional financial resources from the life insurance trust.

In addition to preserving government benefits, life insurance trusts can also provide other advantages, such as mitigating estate taxes, eliminating gift taxes, protecting assets from creditors, and controlling distributions. However, it is important to note that setting up and maintaining a life insurance trust can be complex and expensive, and it may not be the best option for everyone. It is always recommended to consult with an experienced financial professional or estate planning attorney before making any decisions regarding life insurance trusts.

NAFLD: High-Risk Life Insurance and Your Health

You may want to see also

![The Estate [DVD]](https://m.media-amazon.com/images/I/71hfjtYRRrL._AC_UY218_.jpg)

![]()

Life insurance trusts can control distributions

Life insurance trusts can be a powerful tool to control distributions to beneficiaries. The trustee of the trust can be given discretionary powers to make distributions and control when beneficiaries receive proceeds from the trust. This means that the grantor can specify how and when beneficiaries receive distributions, such as when they reach certain milestones like graduating from college, getting married, or having a child. This level of control ensures that the grantor's wishes are respected and that the beneficiaries receive the funds as intended.

For example, the grantor can structure the trust to release funds to beneficiaries as they reach specific ages or life events. This can help to ensure that the beneficiaries do not spend their entire inheritance all at once and provide a level of financial security over time. The trustee manages the trust's benefits and distributes the funds according to the terms outlined in the trust document.

In the case of irrevocable life insurance trusts (ILITs), the trust owns and controls the life insurance policy during the insured's lifetime. The trustee manages the trust and distributes the proceeds upon the insured's death, following the instructions provided by the insured. ILITs can be particularly useful for managing and controlling distributions to beneficiaries.

Revocable life insurance trusts (RLITs), on the other hand, offer more flexibility as they can be changed or cancelled by the grantor. However, assets in RLITs remain part of the grantor's estate and may be subject to estate taxes.

Overall, life insurance trusts provide a way to control distributions to beneficiaries, ensuring that the funds are used as intended and providing financial security for the beneficiaries over time.

Life Insurance Payouts: Lump Sum Benefits Explained

You may want to see also

Frequently asked questions

A life insurance trust is a legal agreement that allows a third party to manage the death benefit from a life insurance policy. It ensures that the policy's death benefit is distributed to your beneficiaries according to your wishes.

An IRA (Individual Retirement Account) allows you to save money for retirement in a tax-advantaged way. You can set up an IRA with a bank or other financial institution, including a life insurance company.

The three main types of IRAs are Traditional IRAs, Roth IRAs, and Rollover IRAs. Each has different tax advantages.

Life insurance trusts can be useful for those with substantial wealth, as they may help shield beneficiaries from estate taxes on life insurance proceeds. They can also be used to structure benefit payments to children and ensure loved ones are taken care of according to your wishes.

IRAs offer tax advantages that allow your savings to grow more quickly than in a taxable account. They also provide access to a wide range of investment choices and can supplement your current savings in employer-sponsored retirement plans.