Alternate funding plans, also known as level-funded plans, are a way for employers to pay for health services and manage costs while helping employees get more value from their benefits. These plans are designed to reduce costs without reducing benefits by finding a different way to pay for them. They are also known as self-funded plans, where the employer assumes the financial risk of providing health services to their employees. With this type of plan, the employer's premium rate is based on the medical claims experience of their workforce. If the costs are higher, the employer pays more; if they are lower, the employer may get money back. This differs from traditional insurance plans, where the employer pays a fixed premium and the insurance company assumes the financial risk.

| Characteristics | Values |

|---|---|

| Traditional plans | Fixed premium paid by the employer |

| Insurance company assumes financial risk | |

| If medical claims are higher, insurer pays; if lower, insurer keeps the difference | |

| Alternate funding plans | Employer assumes financial risk |

| Costs may vary month-to-month | |

| If medical claims are lower, employer may get money back | |

| Customizable health benefit packages | |

| May provide surplus refund to employers | |

| Self-insured plans | Employer's premium rate is based on the medical claims experience of their workforce |

| Level-funded plans | Hybrid arrangement combining fully insured and self-insured models |

| Fixed monthly payment | |

| Protection from large, catastrophic medical claims with stop-loss insurance | |

| May be exempt from state premium taxes and Affordable Care Act (ACA) regulations | |

| Alternative Funding Programs (AFPs) | Third-party, for-profit vendors |

| Control access to specialty medicine not covered by an insurance plan |

Explore related products

What You'll Learn

![]()

Self-funded medical benefits plans

Self-funded plans give employers more flexibility to customize plans to meet their business goals and employees' needs. This is because most state benefit mandates do not apply, allowing employers to design coverage that drives affordability and can be modified to change with the variable demographics of those covered under the health plan. Self-funded employers also receive detailed reporting that can help them make the best decisions for their plan, including exactly where their money is going.

There are a few different options for how self-funded plans can be structured. Firstly, businesses can choose to pay medical claims as they are incurred, or deposit expected costs each month. If there are funds left over after all claims are paid, companies can keep the difference. Secondly, employers can choose to include a stop-loss insurance policy as part of their self-funded plan. This provides coverage for large, catastrophic medical claims by a single, covered individual and provides overall coverage in the event that all medical claims go beyond a certain dollar limit. Finally, a third-party claims administration agreement can be included, where an administrator provides claims processing, billing, customer service, and other services.

Self-funded plans are not right for every employer, but they can provide many benefits for certain companies. For example, in most states, there is no premium tax applied to claims funded directly by an employer, giving employers who have self-funded health plans lower taxes than a traditional insured policy. Additionally, with traditional plans, the employer pays a fixed premium and the insurance company assumes the financial risk. If the actual medical claims are higher than expected, the insurer pays them, but if they are lower, the insurer keeps the difference. With self-funded plans, employers can keep this difference, potentially resulting in a surplus.

Understanding Auto Insurance: Medical Expense Coverage

You may want to see also

Explore related products

$199.95 $245.95

![]()

Stop-loss insurance policies

Alternate funding plans, also known as "level-funded" plans, offer employers new ways to pay for health services, manage costs, and help employees get more value from their benefits. One such plan is a stop-loss insurance policy.

Stop-loss insurance is designed for employers who self-fund their health benefit plans but want to protect themselves from assuming full liability for losses from catastrophic claims. With a self-funded stop-loss employee health insurance policy, insurers are liable for any losses that exceed the employer's deductible limit. This limit can be as low as $10,000 for small and midsize businesses. Stop-loss insurance coverage helps employers protect their financial reserves and bottom line.

There are two types of stop-loss insurance: specific stop-loss and aggregate stop-loss. Specific stop-loss insurance, also known as individual stop-loss, provides coverage against high-value claims from a single employee. It protects employers from an unusually high claim from an individual, rather than an atypical number of claims. On the other hand, aggregate stop-loss insurance puts a ceiling on the dollar amount of eligible expenses that an employer would pay during a contract period. It protects against increases in individual and group-level costs by safeguarding against the combined cost of everyone's claims over a set amount within the policy year.

The role of stop-loss coverage is to cover claims above the plan's specified limit. The claims fund of a self-funded employer will pay claims up to the predetermined deductible for each covered employee, and the stop-loss coverage will kick in for claims above these deductible levels. Stop-loss coverage is typically written through a trust, where the trustee (a bank) acts as the policyholder. The employer's plan document, which defines the benefits offered to employees, is critical in determining liability under the stop-loss coverage. Any changes to the plan document after its initial approval must be approved before their inclusion in the stop-loss coverage.

In summary, stop-loss insurance policies are an essential component of self-funded health insurance plans, allowing employers to manage their financial risks and protect their bottom line by covering losses from high-value or catastrophic claims.

Occupational Therapy: Is Medical Insurance Enough?

You may want to see also

Explore related products

![]()

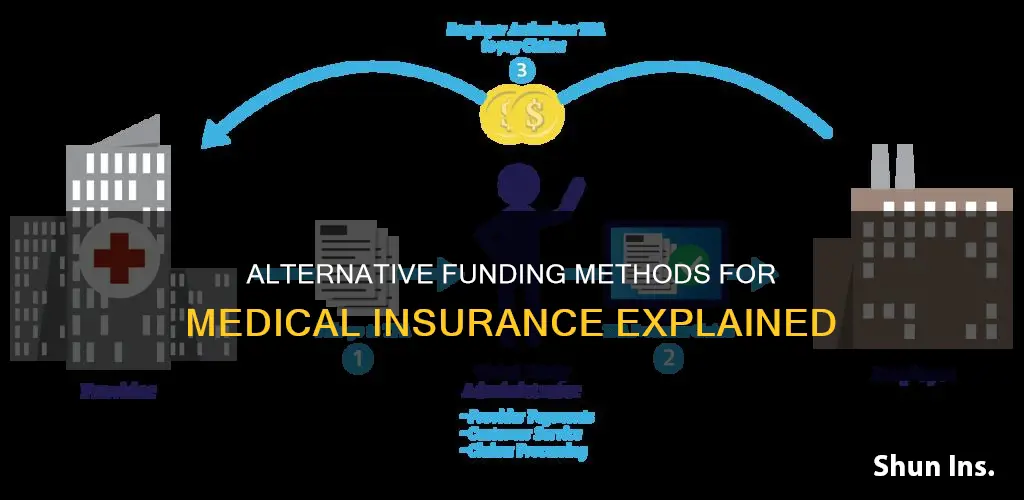

Third-party claims administration

A third-party administrator (TPA) is an organisation that provides operational services such as claims processing, billing, customer service, and other day-to-day operations for self-funded health plans. They are commonly used by health insurance providers who outsource many of their administrative functions. When companies transition from a traditional fully insured model of healthcare to a self-funded plan, they often bring in a TPA to handle the ongoing administration. This is because self-funding employee healthcare can help employers reduce costs, and a growing number of employers have opted for this approach.

A TPA does not provide insurance or assume financial risk for claims; instead, it acts as a service provider, supporting the self-funded health plan. The level of services offered by a TPA can vary, from simply processing claims to providing a comprehensive health plan solution that includes direct primary care and transparent pharmacy benefits. TPAs can also help employers implement employee benefit plans and provide valuable insights into healthcare options.

By partnering with a TPA, companies can gain more coverage, funding, and reimbursement options. TPAs can also maintain relationships with insurers, allowing employers to access specialised insurance coverage, such as stop-loss insurance, which limits the risk of high claims. This type of insurance is particularly relevant in the context of alternate funding plans, where the employer assumes the financial risk of providing health services.

In summary, third-party claims administration plays a crucial role in alternate funding plans by providing administrative support, improving cost efficiency, and enhancing coverage and funding options for self-funded health plans.

Selling Medical Devices: Strategies Without Insurance Coverage

You may want to see also

Explore related products

![]()

Managed risk

Alternative funding plans work by managing financial risk differently from traditional plans. In a traditional plan, the employer pays a fixed premium and the insurance company assumes the financial risk of providing health services, as well as covering administrative costs and taxes. If the actual medical claims are higher than expected, the insurer pays them; if they are lower, the insurer keeps the difference.

With an alternative funding plan, the employer assumes the financial risk of providing health services to their employees. This cost may vary from month to month. The employer still pays a fixed cost for administrative fees, the stop-loss premium, and the monthly maximum claim liability. At the end of the plan year, if the total medical claims are lower than anticipated, the employer may receive money back, depending on state law. This type of plan is also known as a "self-funded" plan.

With alternative funding plans, there is an opportunity for annual refunds or dividends. If a company's employees incur fewer claims than expected and there are claims-allocated funds remaining at the end of the benefit period, a refund for some portion of the unused funds will be returned or credited to the company. This is similar to traditional plans, where insurers keep the difference if claims are lower than expected.

Alternative funding plans provide greater transparency for employers, allowing them to see where their medical premium dollars are being spent. These plans also reduce costs without reducing benefits by finding different ways to pay for those benefits. For example, many employers have raised deductibles and implemented high-deductible plans and tax-advantaged savings accounts.

Terminating Medicare Part B: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Customised health benefit packages

The shift towards customised benefits is driven by several factors, including the ever-increasing rates of traditional insurance plans, the shrinking group health insurance market, and the rise of healthcare consumerism. The COVID-19 pandemic has also played a role, as businesses now prioritise attracting and retaining top talent.

Additionally, customised packages can include wellness stipends, which empower employees to take charge of their physical and mental health. These stipends can be used to reimburse employees for expenses such as gym memberships, fitness classes, yoga, and meditation apps.

By offering customised health benefit packages, employers can stabilise costs while providing attractive benefits that cater to the diverse needs and preferences of their workforce.

Applying for Medical Insurance in NJ: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Alternative funding plans, also known as "level-funded" plans, are a way for employers to pay for health services and manage costs. They are designed to reduce costs without reducing benefits.

With a traditional plan, the employer pays a fixed premium and the insurance company assumes the financial risk. With an alternative funding plan, the employer assumes the financial risk and pays for health services to the employer group. If costs are lower, the employer may get money back.

Alternative funding plans allow employers to manage financial risk differently and provide greater transparency into where their medical premium dollars are being spent. They also allow employers to customise their benefits package.

Alternative funding programs (AFPs) are third-party, for-profit vendors that provide access to specialty medicine not covered by an insurance plan. AFPs are designed to save the insurance company money.

A self-insured plan moves the financial risk to the employer but also provides the greatest opportunity for savings. Level-funded plans are a hybrid of fully-insured and self-insured models, allowing employers to pay fixed premiums while also being exempt from certain taxes.