An insurance annuity is a financial product offered by insurance companies that provides a steady stream of income in exchange for a lump-sum payment or a series of premiums. Designed to offer financial security, particularly during retirement, annuities guarantee regular payments over a specified period or for the lifetime of the annuitant. They come in various forms, such as fixed, variable, or indexed annuities, each with different features and risk levels. By combining elements of investment and insurance, annuities help individuals manage longevity risk and ensure a stable income in their later years, making them a popular tool for retirement planning.

Explore related products

![The Utility and Application of Insurances on Lives and Life Annuities Briefly Explained : with Tables, Showing Their Relative Values for Different Ages / by J. Meyer 1811 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

What You'll Learn

- Definition: An insurance annuity is a contract offering regular payments in exchange for a lump sum or premiums

- Types: Fixed, variable, and indexed annuities cater to different financial goals and risk tolerances

- Benefits: Provides guaranteed income, tax-deferred growth, and protection against outliving retirement savings

- Costs: Fees, surrender charges, and potential investment risks are key considerations before purchasing

- Uses: Ideal for retirement planning, legacy building, or ensuring steady income during later years

![]()

Definition: An insurance annuity is a contract offering regular payments in exchange for a lump sum or premiums

An insurance annuity is a financial product that serves as a contract between an individual and an insurance company, designed to provide a steady stream of income over a specified period or for life. At its core, Definition: An insurance annuity is a contract offering regular payments in exchange for a lump sum or premiums. This means the policyholder pays a single large amount (lump sum) or a series of smaller payments (premiums) to the insurance company, which then agrees to make regular payments back to the individual at a later date. This arrangement is particularly appealing for those seeking predictable income during retirement or other long-term financial planning goals.

The structure of an insurance annuity is straightforward yet powerful. Once the contract is in place, the insurance company invests the lump sum or premiums received, allowing the funds to grow over time. This growth is often tax-deferred, meaning taxes are not paid on the earnings until the money is withdrawn. When the annuity payments begin, the individual receives a guaranteed income stream, which can be customized to meet specific needs, such as monthly, quarterly, or annual payments. The regularity and predictability of these payments make annuities a popular tool for managing financial risk and ensuring long-term stability.

There are different types of insurance annuities, each tailored to meet varying financial objectives. Immediate annuities begin payments shortly after the lump sum is paid, often within a year, making them ideal for those needing income right away. Deferred annuities, on the other hand, allow the initial investment to grow over time before payments start, which is beneficial for long-term savings strategies. Additionally, annuities can be categorized as fixed, where payments are guaranteed at a set amount, or variable, where payments fluctuate based on the performance of underlying investments. Understanding these options is crucial for aligning an annuity with one’s financial goals.

One of the key advantages of an insurance annuity is the guarantee it provides. Unlike other investment vehicles that are subject to market volatility, annuities offer a level of security, ensuring that the individual will receive the agreed-upon payments regardless of economic conditions. This makes annuities particularly attractive for risk-averse individuals or those seeking to protect their retirement income. However, it’s important to note that annuities often come with fees and restrictions, such as surrender charges for early withdrawals, which can impact their flexibility.

In summary, Definition: An insurance annuity is a contract offering regular payments in exchange for a lump sum or premiums, and it plays a vital role in financial planning by providing a reliable income stream. Whether used for retirement, wealth preservation, or legacy planning, annuities offer a structured approach to managing money over the long term. By understanding the different types and features of annuities, individuals can make informed decisions to secure their financial future.

Life Insurance Repurchase: Understanding the Renewal Option

You may want to see also

Explore related products

$14.99

$9.99 $9.99

![]()

Types: Fixed, variable, and indexed annuities cater to different financial goals and risk tolerances

An insurance annuity is a financial product offered by insurance companies, designed to provide a steady stream of income in retirement or over a specified period. Annuities are essentially contracts between an individual and an insurer, where the individual pays a lump sum or a series of premiums in exchange for regular payments in the future. When considering annuities, it’s crucial to understand the different types available, as each caters to distinct financial goals and risk tolerances. The three primary types of annuities are fixed, variable, and indexed, each offering unique features and benefits.

Fixed annuities are the most straightforward and conservative option among the three. They guarantee a fixed rate of interest on the premiums paid, providing predictable and stable returns over time. This type of annuity is ideal for risk-averse individuals who prioritize security and steady income. Fixed annuities are not tied to market performance, making them less volatile and a reliable choice for those seeking consistent growth. They are particularly appealing to retirees or those nearing retirement who want to ensure a guaranteed income stream without exposure to market fluctuations. However, the trade-off is that fixed annuities may offer lower returns compared to other types, especially in a rising market.

Variable annuities, on the other hand, are suited for individuals with a higher risk tolerance and a longer investment horizon. Unlike fixed annuities, the returns on variable annuities are tied to the performance of underlying investment portfolios, typically mutual funds. This means the value of the annuity can fluctuate based on market conditions, offering the potential for higher returns but also carrying the risk of losses. Variable annuities are attractive to those who are comfortable with market volatility and are willing to take on more risk for the opportunity to grow their investment more significantly. They often include optional riders, such as guaranteed minimum withdrawal benefits, which can provide a safety net in case of poor market performance.

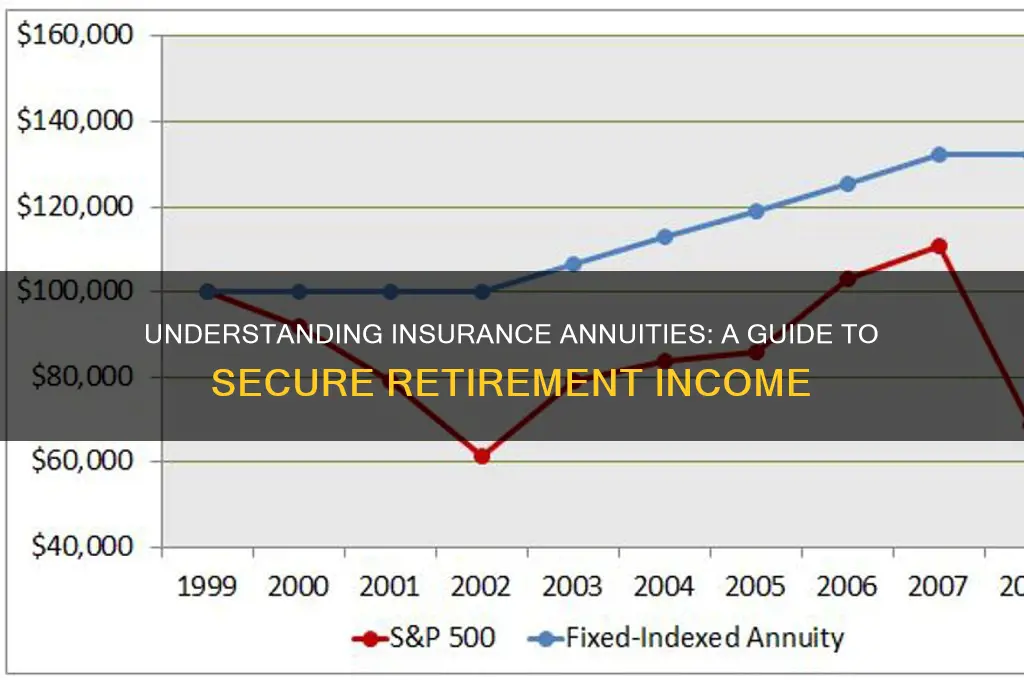

Indexed annuities strike a balance between the stability of fixed annuities and the growth potential of variable annuities. These annuities earn interest based on the performance of a specific market index, such as the S&P 500, but with a floor that protects against negative returns. This means that while the annuity’s value can increase with the index, it will not decrease if the index performs poorly. Indexed annuities are a good fit for individuals who want some exposure to market gains without the full risk of market downturns. They offer a middle ground for those who seek growth but also desire a level of protection for their principal investment.

In summary, the choice among fixed, variable, and indexed annuities depends on an individual’s financial goals, risk tolerance, and investment horizon. Fixed annuities provide security and predictability, making them ideal for conservative investors. Variable annuities offer the potential for higher returns but come with greater risk, suited for those comfortable with market volatility. Indexed annuities combine elements of both, offering growth potential with downside protection, appealing to those seeking a balanced approach. Understanding these differences is essential for selecting the annuity that best aligns with one’s retirement planning and financial objectives.

Tricare for Life: Insurance Card Essentials for Enrollees

You may want to see also

Explore related products

![]()

Benefits: Provides guaranteed income, tax-deferred growth, and protection against outliving retirement savings

An insurance annuity is a financial product offered by insurance companies designed to provide a steady stream of income during retirement. One of its primary benefits is providing guaranteed income, which ensures retirees receive a consistent cash flow for a specified period or even for life. This predictability is particularly valuable in retirement planning, as it helps individuals budget effectively and maintain their standard of living without worrying about market fluctuations. Unlike investments tied to stock market performance, an annuity’s income stream is contractually guaranteed by the insurance company, offering peace of mind and financial stability.

Another significant benefit of insurance annuities is tax-deferred growth. With this feature, the funds within the annuity grow without being subject to annual taxes until withdrawals are made. This allows the investment to compound over time at a faster rate compared to taxable accounts, maximizing the potential for growth. For retirees, this means more of their money remains invested and working for them, which can be especially advantageous when planning for long-term financial needs. Tax-deferred growth also provides flexibility in managing taxable income during retirement, enabling individuals to optimize their tax strategies.

Insurance annuities also offer protection against outliving retirement savings, a critical concern for many retirees. With longevity increasing, there is a growing risk of exhausting savings during retirement. Annuities address this by providing a lifetime income option, ensuring that individuals continue to receive payments as long as they live, regardless of how long that may be. This feature eliminates the fear of running out of money in later years, making annuities a reliable tool for securing long-term financial security.

Additionally, the combination of guaranteed income, tax-deferred growth, and longevity protection makes insurance annuities a versatile retirement planning tool. They can complement other retirement accounts, such as 401(k)s or IRAs, by providing a stable foundation of income. For those seeking to balance growth potential with security, annuities offer a unique solution that caters to both needs. By incorporating an annuity into their retirement strategy, individuals can achieve greater confidence in their financial future.

Lastly, insurance annuities provide a level of simplicity and ease in retirement planning. Once purchased, the annuity contract outlines clear terms for income distribution, removing the need for ongoing investment management. This is particularly appealing for retirees who prefer a hands-off approach or lack the expertise to actively manage their portfolios. With guaranteed income, tax advantages, and protection against longevity risk, insurance annuities stand out as a comprehensive solution for addressing the complexities of retirement planning.

Insured International Shipping: What's Covered?

You may want to see also

Explore related products

![]()

Costs: Fees, surrender charges, and potential investment risks are key considerations before purchasing

When considering an insurance annuity, it's crucial to understand the various costs associated with it, as these can significantly impact your overall returns and financial flexibility. Fees are one of the primary expenses you’ll encounter. Annuities often come with administrative fees, management fees, and mortality and expense (M&E) charges. Administrative fees cover the cost of maintaining your account, while management fees are associated with the investment options within the annuity. M&E charges are unique to insurance products and cover the insurer’s costs for providing death benefits and managing the annuity. These fees can vary widely among providers and annuity types, so it’s essential to compare them carefully to ensure they align with your financial goals.

Another critical cost to consider is surrender charges. These are penalties imposed if you withdraw a significant portion of your annuity funds or terminate the contract before the end of the surrender period, which typically lasts 5 to 10 years. Surrender charges can be substantial, often starting at 7% or more of the withdrawal amount and decreasing annually. They are designed to discourage early withdrawals and protect the insurer’s interests. Before purchasing an annuity, evaluate your liquidity needs and ensure you’re comfortable with the surrender period to avoid unexpected costs.

Potential investment risks are also a key consideration. Unlike guaranteed interest rates in fixed annuities, variable and indexed annuities tie your returns to the performance of underlying investments, such as mutual funds or market indices. This means your principal is not protected, and you could lose money if the investments perform poorly. Additionally, annuities often come with rider fees for optional benefits like guaranteed lifetime income or long-term care coverage. While these riders can provide valuable protection, they add to the overall cost and may reduce your investment returns.

It’s also important to assess the opportunity cost of investing in an annuity. By locking your money into an annuity, you may forgo other investment opportunities with potentially higher returns. Annuities are generally illiquid, and accessing your funds early can be costly. Consider your long-term financial objectives and whether an annuity aligns with your need for growth, income, or both. Consulting a financial advisor can help you weigh these factors and determine if the costs and risks of an annuity are justified for your situation.

Finally, be aware of hidden costs that may not be immediately apparent. Some annuities charge fees for transferring between investment options or for exceeding certain withdrawal limits. Others may have high commissions paid to the salesperson, which can indirectly affect the annuity’s performance. Transparency is key, so request a detailed fee schedule and ask about any potential costs not explicitly stated in the contract. Understanding these expenses upfront will help you make an informed decision and avoid surprises down the line.

Life Insurance ACB: What You Need to Know

You may want to see also

Explore related products

![]()

Uses: Ideal for retirement planning, legacy building, or ensuring steady income during later years

An insurance annuity is a financial product offered by insurance companies, designed to provide a steady stream of income over a specified period, often in retirement. It is a contract between an individual and an insurer, where the individual pays a lump sum or a series of premiums in exchange for regular payments at a later date. This makes annuities an ideal tool for retirement planning, as they offer a reliable income stream that can supplement other retirement savings, such as 401(k)s or IRAs. By converting a portion of your savings into an annuity, you can ensure a consistent paycheck-like income during your later years, reducing the risk of outliving your savings.

Beyond retirement planning, insurance annuities are also valuable for legacy building. Certain types of annuities, such as life annuities with a guaranteed period or joint-and-survivor annuities, ensure that payments continue to a designated beneficiary after the annuitant’s death. This feature allows individuals to leave a financial legacy for their loved ones, providing them with ongoing support even in their absence. Additionally, some annuities offer a death benefit, which returns any remaining value in the contract to the beneficiary, further enhancing their role in estate planning.

For those seeking steady income during later years, annuities provide a level of financial security that is hard to replicate with other investments. Unlike stocks or bonds, which are subject to market volatility, annuities offer guaranteed payments, often for life. This predictability is particularly appealing for retirees who rely on fixed incomes and want to avoid the stress of market fluctuations. Immediate annuities, for example, begin payouts shortly after the initial investment, making them an excellent option for individuals nearing or already in retirement.

Another use of insurance annuities is to protect against longevity risk, the risk of living longer than expected and exhausting your savings. With life expectancy increasing, this is a growing concern for retirees. Annuities, especially lifetime income annuities, address this risk by providing guaranteed payments for as long as you live, regardless of how long that may be. This ensures that you maintain your standard of living without worrying about running out of money.

Lastly, annuities can be tailored to meet specific financial goals, making them versatile for various needs. For instance, deferred annuities allow you to accumulate funds over time, tax-deferred, and then convert them into a steady income stream at a later date. This flexibility makes them suitable for individuals who are still years away from retirement but want to secure future income. Whether for retirement planning, legacy building, or ensuring steady income, insurance annuities offer a structured and reliable solution to meet long-term financial objectives.

Affording Life Insurance: Apollo Astronauts' Dilemma

You may want to see also

Frequently asked questions

An insurance annuity is a financial product offered by insurance companies that provides a steady stream of income in exchange for a lump sum or series of payments. It is designed to help individuals secure a guaranteed income, often during retirement.

An insurance annuity works by having the policyholder pay a lump sum or periodic premiums to an insurance company. In return, the insurer agrees to make regular payments to the annuitant at a future date, either immediately or at a specified time, such as retirement.

There are three main types of insurance annuities: fixed annuities (guaranteed interest rate), variable annuities (investments tied to market performance), and indexed annuities (returns linked to a stock market index).

Benefits include guaranteed income for life or a set period, tax-deferred growth, protection against market volatility (in fixed and indexed annuities), and the ability to provide financial security during retirement.

Drawbacks include high fees, limited liquidity (penalties for early withdrawals), potential loss of principal in variable annuities, and reduced flexibility compared to other investment options.