Medicare Supplement Insurance, also known as Medigap, is an additional insurance plan that can be purchased to supplement Original Medicare (Parts A and B) coverage. Medigap helps to cover out-of-pocket costs such as deductibles, copayments, and coinsurance, which Original Medicare does not cover. While Medigap is supplemental insurance, it is different from Medicare Advantage, which is an alternative way to receive Medicare benefits through private health plans. Medicare Advantage plans may offer additional services bundled with Original Medicare coverage, but they cannot be combined with Medigap plans. Medigap policies are standardized, offering the same basic benefits across different insurance companies, with price being the main differentiator. Understanding the differences between Medigap and other supplemental insurance options is crucial for choosing a plan that meets one's unique healthcare needs and financial situation.

| Characteristics | Values |

|---|---|

| Definition | Medicare Supplement Insurance (Medigap) is extra insurance that helps pay your share of out-of-pocket costs in Original Medicare. |

| Other Names | Medicare Supplement Insurance and Medigap are different names for the same type of health insurance plan. |

| Who Can Buy? | You can only buy Medigap if you have Original Medicare Parts A and B. |

| When to Buy | The best time to enroll in a Medigap plan is during the Medigap Open Enrollment Period, which is a one-time, 6-month period starting the first month you have Medicare Part B and are 65 or older. |

| Number of Plans | There are up to 10 different Medigap plans offered in most states, which are named by letters: A-N (E, H, I, J are no longer sold). |

| Plan Differences | Price is the only difference between plans with the same letter sold by different insurance companies. |

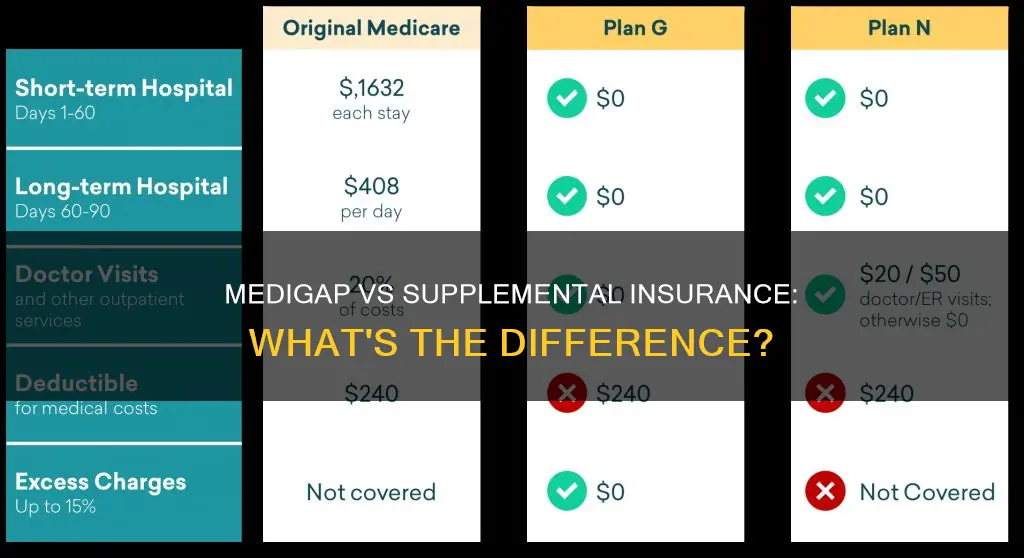

| Exclusions | Medigap generally doesn't cover long-term care, routine vision or dental care, hearing aids, eyeglasses, and private-duty nursing. It also doesn't include prescription drug coverage. |

| Medicare Advantage vs Medigap | Medicare Advantage is an alternative way to get Medicare benefits, while Medigap is purely supplemental. You can't use both at the same time. |

Explore related products

$26.89 $110

What You'll Learn

![]()

Medicare Supplement Insurance (Medigap) is extra insurance

Medicare Supplement Insurance, also known as Medigap, is extra insurance purchased from a private insurance company. It helps cover some costs that Original Medicare doesn't pay, such as copayments, coinsurance, and deductibles. Medigap cannot be combined with most Medicare Advantage plans or Medical Savings Account (MSA) plans.

To be eligible for a Medigap plan, you must be enrolled in both Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). The best time to enroll in a Medigap plan is during the Medigap Open Enrollment Period, which starts on the first day of the month in which you turn 65 and are enrolled in Medicare Part B. During this period, you have guaranteed issue rights, meaning insurance companies cannot deny you coverage or charge you higher premiums based on pre-existing conditions.

There are 10 different types of Medigap plans offered in most states, which are named by letters: A-D, F, G, and K-N. The cost of a Medigap plan can depend on various factors, including the insurance company, the specific plan, your location, and your age. Generally, the more coverage you choose, the more your plan will cost.

Medigap is designed to reimburse you for the costs you pay out of your own pocket. The amount of reimbursement you receive depends on the type of plan you have. It's important to note that Medigap does not cover certain expenses, such as long-term care, routine vision or dental care, hearing aids, eyeglasses, and private-duty nursing.

Understanding Zero Dep Insurance: What, Why, and How?

You may want to see also

Explore related products

![]()

Medigap policies cover benefits not covered by Medicare

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company. It helps cover some costs that Original Medicare doesn't pay, such as copayments, coinsurance, and deductibles. Medigap policies can also provide other benefits that Original Medicare does not cover. For example, certain expenses that Medicare Supplement Insurance plans generally don't cover include long-term care, routine vision or dental care, hearing aids, eyeglasses, and private-duty nursing.

To be eligible for a Medicare Supplement plan, you must be enrolled in both Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). The best time to enroll in a Medigap plan is during the Medigap Open Enrollment Period, which starts on the first day of the month in which you turn 65 and are enrolled in Medicare Part B. During this period, you have guaranteed issue rights, meaning insurance companies cannot deny you coverage based on pre-existing conditions.

Medigap plans are typically offered as monthly premium plans, and you will need to pay the premium in addition to your Medicare Part B premium. The cost of Medicare Supplement plans can vary depending on factors such as the insurance company, the specific plan, your location, and your age. Generally, the more coverage you choose, the higher the cost of the plan.

Medigap policies only cover the insured individual, so you and your spouse must buy separate policies. It's important to note that you cannot combine Medigap with most Medicare Advantage plans or Medical Savings Account (MSA) plans. Additionally, when switching from Medicare Advantage to Original Medicare, you may lose your guaranteed-issue rights for Medigap. Therefore, it is recommended to determine which benefits you want and which plan suits your needs before enrolling.

Maxcare Service Insurance: What You Need to Know

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medigap plans are offered as monthly premiums

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company. Medigap helps cover out-of-pocket costs not covered by Original Medicare, such as copayments, coinsurance, and deductibles. It is important to note that Medigap cannot be combined with most Medicare Advantage plans or Medical Savings Account (MSA) plans.

To be eligible for a Medigap plan, individuals must be enrolled in both Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). The best time to enroll in a Medigap plan is during the Medigap Open Enrollment Period, which begins on the first day of the month in which an individual turns 65 and is enrolled in Medicare Part B. During this period, insurance companies cannot deny coverage or charge higher premiums based on pre-existing conditions. However, outside of the open enrollment period, individuals may face medical underwriting and potentially higher premiums.

Medigap plans are typically offered as monthly premium plans, and the cost of these premiums can vary depending on various factors, including the insurance company, the specific plan, location, and age. For example, the average monthly premium among Medigap policyholders in 2023 was $217, but this varied from a low of around $140 in certain states to $236 in others. Additionally, Medigap policies that include additional benefits may have slightly higher premiums than the standard version. These additional benefits may include coverage for specific dental services, such as diagnostic evaluations and preventive services, which are not typically covered by traditional Medicare.

It is worth noting that Medigap insurers may impose a waiting period of up to six months for services related to pre-existing conditions if the applicant did not have continuous creditable coverage beforehand. Furthermore, rules and requirements may vary when switching from another type of health insurance plan to a Medigap plan, and insurers may require a written health screening questionnaire.

Life Insurance: When to Start?

You may want to see also

Explore related products

![]()

Medigap eligibility requires enrolment in Medicare Part A and Part B

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company. It helps to pay for out-of-pocket costs not covered by Original Medicare, such as copayments, coinsurance, and deductibles. Medigap cannot be combined with most Medicare Advantage plans or Medical Savings Account (MSA) plans.

To be eligible for a Medigap plan, individuals must be enrolled in both Medicare Part A and Part B. The best time to enrol in Medigap is during the Medigap Open Enrollment Period, which begins on the first day of the month in which an individual turns 65 and is enrolled in Medicare Part B. During this period, insurance companies cannot deny coverage or charge higher premiums based on pre-existing conditions. This guaranteed issue right is only available during the open enrolment period and does not repeat annually.

In some states, individuals under the age of 65 with a disability or end-stage renal disease (ESRD) may also be eligible for a Medigap plan. Additionally, there are certain circumstances that guarantee the right to buy a Medigap policy, such as losing previous coverage or having a spouse or dependent who is already enrolled in a Medigap plan.

It is important to note that Medigap plans are standardised, meaning policies with the same letter offer the same basic benefits regardless of the insurance company. The cost of Medigap plans can vary depending on factors such as the insurance company, the specific plan, location, and age. Medigap plans are typically offered as monthly premium plans, paid in addition to the Medicare Part B premium.

Open Enrollment for Health Insurance: When Can You Sign Up?

You may want to see also

Explore related products

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)

![]()

Medigap policies are standardised

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company. It helps to pay for out-of-pocket costs in Original Medicare, such as copayments, coinsurance and deductibles. Medigap policies are standardised, meaning that policies with the same letter offer the same basic benefits, regardless of location or insurance company. There are 10 different types of Medigap plans offered in most states, labelled A-N (E, H, I, and J are no longer sold). The only difference between plans with the same letter sold by different insurance companies is the price.

While the core benefits of Medigap policies are standardised, there may be some variations in additional benefits offered by different insurance companies. These additional benefits can include coverage for services such as vision, dental, or prescription drugs. However, it is important to note that Medigap plans do not typically cover these additional benefits, and consumers should carefully review the specific details of each plan before making a purchase.

In some states, such as Massachusetts, Minnesota, and Wisconsin, Medigap policies are standardised differently. These states have unique Medigap plan names and may offer different sets of benefits. Despite these variations, all Medigap policies must still adhere to federal and state laws designed to protect consumers.

The standardisation of Medigap policies provides a level of consistency and transparency in the healthcare insurance market. It allows consumers to make informed comparisons between plans and choose the option that best suits their needs. This standardisation also helps to ensure that individuals have access to essential healthcare benefits, regardless of their location or insurance provider.

Allstate Insurance: Florida Exodus or Staying Put?

You may want to see also

Frequently asked questions

Medigap, or Medicare Supplement Insurance, is extra insurance that can be purchased from a private insurance company to help pay out-of-pocket costs in Original Medicare (Parts A and B).

Supplemental Insurance, or Medicare Advantage, is an alternative way to receive Medicare benefits. It is not supplemental insurance in the same way as Medigap, but it fills coverage gaps and controls costs.

Medigap is purely supplemental, while Supplemental Insurance (Medicare Advantage) is an alternative way to receive Medicare benefits. Medigap cannot be combined with Medicare Advantage plans, whereas Medicare Advantage fills coverage gaps in Original Medicare.

If you are 65 or older and enrolled in Medicare Parts A and B, you may want to consider Medigap to fill coverage gaps and control out-of-pocket costs. If you are looking for an alternative way to receive your Medicare benefits and potentially bundle additional services, Supplemental Insurance (Medicare Advantage) may be the right choice.