In a growing number of divorce cases, the court will order one or both parties to purchase a life insurance policy as part of the overall divorce settlement. This is known as a divorce decree life insurance policy. If your divorce decree includes child support, alimony, or any other kind of financial support, a judge may also require you to carry a life insurance policy with your ex-spouse as the beneficiary. This is considered court-ordered life insurance since it’s ordered by the judge. The policy is typically meant to serve as financial protection for the ex-spouse and any minor children who depend on the higher-earning spouse for financial support.

| Characteristics | Values |

|---|---|

| Who is it for? | The ex-spouse and any minor children who depend on the higher-earning spouse for financial support |

| Who is the beneficiary? | The ex-spouse |

| Who decides the type of insurance and amount of coverage? | The person who is required to purchase the insurance |

| What is it for? | Financial protection |

| When is it required? | When the divorce decree includes child support, alimony, or any other kind of financial support |

Explore related products

$15.95 $15.95

What You'll Learn

![]()

Divorce decree and child support

A divorce decree may require one or both parties to purchase a life insurance policy as part of the overall divorce settlement. This is especially likely if the divorce decree includes child support, alimony, or any other kind of financial support. In this case, a judge may require the higher-earning spouse to obtain life insurance to protect future child support payments. This is considered court-ordered life insurance.

The type of life insurance and how much coverage you purchase will likely be left up to you to decide. A good place to start is to calculate how much alimony or child support you will owe or be owed until your youngest child is eighteen years old and financially independent. You should make sure that your attorney is aware and approves of any steps you take.

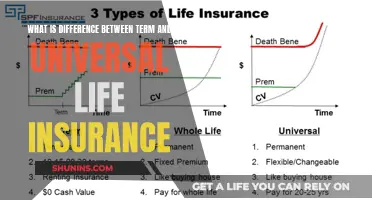

There are many different types of life insurance, but whole life and term life policies are among the most popular options. Whole life insurance policies provide permanent, life-long coverage with the added advantage of cash value. Term life insurance is typically less expensive, but coverage is limited to a specific period of time and these policies don't build cash value.

Life Insurance and Skin Cancer: What's Covered?

You may want to see also

Explore related products

$6.99

![]()

Divorce decree and alimony

A divorce decree may require that you purchase a life insurance policy, although the type of insurance and the amount of coverage you purchase will likely be left up to you to decide. If your divorce decree includes child support, alimony, or any other kind of financial support, a judge may also require you to carry a life insurance policy with your ex-spouse as the beneficiary. This is considered court-ordered life insurance since it’s ordered by the judge.

In a growing number of divorce cases, the court will order one or both parties to purchase a life insurance policy as part of the overall divorce settlement. The policy is typically meant to serve as financial protection for the ex-spouse and any minor children who depend on the higher-earning spouse for financial support. This is especially important if there is a significant income disparity between the two ex-spouses and they share custody of minor children.

If it is known that life insurance will be a requirement for one or both parties in the divorce decree, the parties can each start looking into applying for life insurance. It is extremely important to make sure that attorneys for both parties are aware and approve of any and all steps you take. Prior to divorce proceedings, attorneys will typically take a look at what the financial situations of each person will be. It can be difficult to determine the exact amount necessary in a life insurance policy, but a good place to start could be to look at the amount of alimony and/or child support you will owe or be owed until the youngest child is eighteen years old.

Life Insurance and Welfare Benefits: Compatible or Not?

You may want to see also

Explore related products

![]()

Divorce decree and financial support

If your divorce decree includes child support, alimony, or any other kind of financial support, a judge may require you to carry a life insurance policy with your ex-spouse as the beneficiary. This is considered court-ordered life insurance. In a growing number of divorce cases, the court will order one or both parties to purchase a life insurance policy as part of the overall divorce settlement. The policy is typically meant to serve as financial protection for the ex-spouse and any minor children who depend on the higher-earning spouse for financial support.

If it is known that life insurance will be a requirement for one or both parties in the divorce decree, the parties can each start looking into applying for life insurance. It is extremely important to make sure that attorneys for both parties are aware and approve of any and all steps you take. Prior to divorce proceedings, attorneys will typically take a look at what the financial situations of each person will be. It can be difficult to determine the exact amount necessary in a life insurance policy, but a starting place could be to look at the amount of alimony and/or child support you will owe or be owed until the youngest child is eighteen years old.

While a divorce decree or separation agreement may require that you purchase a policy, the type of life insurance and how much coverage you purchase will likely be left up to you to decide. A good place to start determining how much life insurance you'll actually need is calculating how much alimony or child support you're responsible for until your youngest child is out of the house and financially independent.

Flexible Life Insurance: Is It Worth the Hype?

You may want to see also

Explore related products

![]()

Divorce decree and life insurance policy

In a growing number of divorce cases, the court will order one or both parties to purchase a life insurance policy as part of the overall divorce settlement. This is known as a divorce decree. The policy is typically meant to serve as financial protection for the ex-spouse and any minor children who depend on the higher-earning spouse for financial support.

If your divorce decree includes child support, alimony, or any other kind of financial support, a judge may also require you to carry a life insurance policy with your ex-spouse as the beneficiary. This is considered court-ordered life insurance since it’s ordered by the judge.

While a divorce decree or separation agreement may require that you purchase a policy, the type of life insurance and how much coverage you purchase will likely be left up to you to decide. A good place to start determining how much life insurance you'll actually need is calculating how much alimony or child support you're responsible for until your youngest child is out of the house and financially independent.

If it is known that life insurance will be a requirement for one or both parties in the divorce decree, the parties can each start looking into applying for life insurance. It is extremely important to make sure that attorneys for both parties are aware and approve of any and all steps you take.

Life Insurance Benefits: Taxable in New Jersey?

You may want to see also

Explore related products

![]()

Divorce decree and separation agreement

A divorce decree or separation agreement may require that you purchase a life insurance policy, but the type of life insurance and how much coverage you purchase will likely be left up to you to decide. If your divorce decree includes child support, alimony, or any other kind of financial support, a judge may also require you to carry a life insurance policy with your ex-spouse as the beneficiary. This is considered court-ordered life insurance since it’s ordered by the judge.

In a growing number of divorce cases, the court will order one or both parties to purchase a life insurance policy as part of the overall divorce settlement. The policy is typically meant to serve as financial protection for the ex-spouse and any minor children who depend on the higher-earning spouse for financial support. If there's a significant income disparity between you and your ex and you share custody of minor children, a divorce decree may order the higher-earning spouse to obtain life insurance to protect future child support payments.

It is extremely important to make sure that attorneys for both parties are aware and approve of any and all steps you take. Prior to divorce proceedings, attorneys will typically take a look at what the financial situations of each person will be. It can be difficult to determine the exact amount necessary in a life insurance policy, but a starting place could be to look at the amount of alimony and/or child support you will owe or be owed until the youngest child is eighteen years old.

There are many different types of life insurance, but whole life and term life policies are among the most popular options. Whole life insurance policies provide permanent, life-long coverage with the added advantage of cash value: a tax-efficient asset that can be tapped into during your lifetime. Term life insurance is typically less expensive, but coverage is limited to a specific period of time (terms typically last 10, 15, 20, or 30 years), and these policies don't build cash value.

Retesting for Life Insurance: When and Why You Should

You may want to see also

Frequently asked questions

Divorce decree life insurance is when a court orders one or both parties to purchase a life insurance policy as part of the overall divorce settlement. This is usually to serve as financial protection for the ex-spouse and any minor children who depend on the higher-earning spouse for financial support.

A court may order divorce decree life insurance to protect future child support payments, especially if there is a significant income disparity between the two parties.

There are many different types of life insurance, but whole life and term life policies are among the most popular options. Whole life insurance policies provide permanent, life-long coverage with the added advantage of cash value, while term life insurance is typically less expensive, but coverage is limited to a specific period of time.

The amount of life insurance you need will depend on the amount of alimony and/or child support you will owe or be owed until your youngest child is eighteen years old.