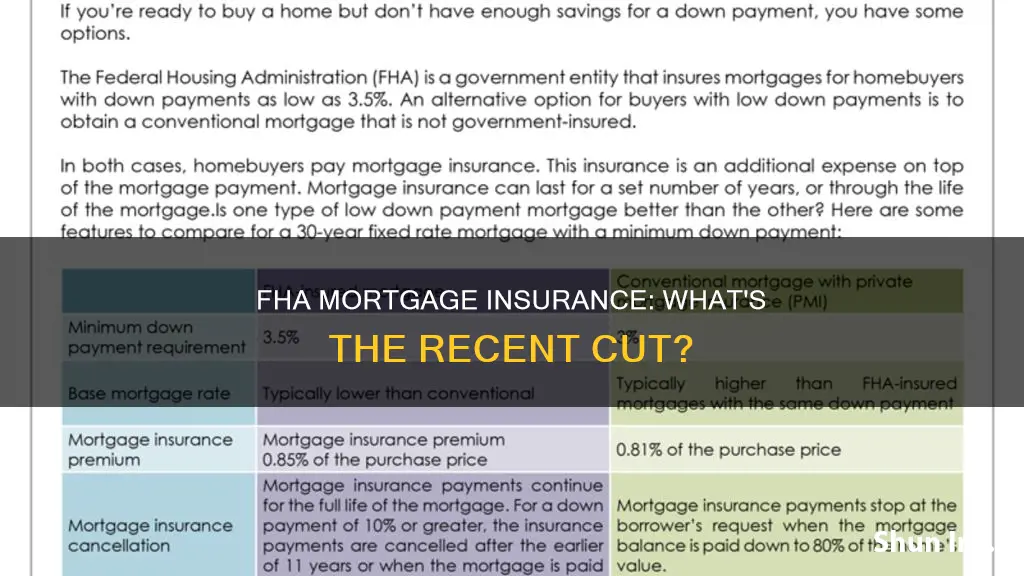

FHA mortgage insurance premiums (MIP) are additional fees that borrowers pay upfront and over the course of the mortgage term, regardless of the down payment amount. Beginning March 20, 2023, FHA mortgage insurance premiums were reduced, making payments more affordable and qualifying easier. This reduction lowered the annual FHA MIP by 30 basis points (BPS), resulting in a decrease from 0.85% to 0.55% for FHA borrowers with loan terms longer than 15 years and a base loan amount of $726,200 or less.

While FHA mortgage insurance provides protection for lenders in the event of borrower default, it can be challenging for borrowers to eliminate these premiums. The options for removing FHA mortgage insurance include automatic termination and refinancing to a conventional loan. Automatic cancellation eligibility is primarily determined by the loan origination date and the down payment amount. On the other hand, refinancing to a conventional loan requires sufficient home equity, a strong credit score, and favourable interest rates.

| Characteristics | Values |

|---|---|

| FHA mortgage insurance reduction | Beginning March 20, 2023, mortgage insurance premiums will be lower on most FHA loans, making payments more affordable and qualifying easier |

| FHA Mortgage Insurance Premium (MIP) | An additional payment the borrower pays to the lender to secure the loan |

| MIP as a way to protect the lender | In case of default on an FHA mortgage, the FHA reimburses the lender the outstanding balance |

| MIP requirements | Both upfront and annual mortgage insurance for all borrowers, regardless of the amount of the down payment |

| MIP as an additional charge | The borrower must pay this on top of monthly principal and interest payments |

| FHA loans | Governed by the Federal Housing Administration and can often accommodate borrowers with lower credit scores, income, and cash-to-close compared to conventional loans |

| Maximum amount for an FHA loan | $472,030 in most areas |

| Maximum loan limit for FHA borrowers in high-cost areas | $1,089,300 |

| Special exception loan limits | In Alaska, Hawaii, Guam, and the U.S. Virgin Islands, single-family home loans are capped at $1,633,950 |

| FHA homebuyers and homeowners expected savings | An average of $800 per year, with borrowers with higher loan amounts expected to save even more |

| FHA borrowers with a loan longer than 15 years | Mortgage insurance premiums will drop from 0.85% to 0.55% with a base loan amount of $726,200 or less |

| FHA borrowers with a 15-year fixed mortgage and a 10% or greater down payment | The MIP will expire after 11 years, and the cost drops from 0.80% to 0.50% |

| FHA borrowers with loan amounts above $726,200 | A 0.75% MIP is now charged, down from a 1.05% MIP previously |

| FHA borrowers with a down payment of 10% or more | The MIP term is 11 years, and the cost ranges from 1% to 0.70% |

| FHA borrowers who don't qualify for automatic MIP cancellation | Refinancing to a conventional loan is usually the best way to remove FHA mortgage insurance |

| Requirements for FHA mortgage insurance removal | The loan must be in good standing, the borrower must have a good payment history, there must be no outstanding FHA loans or past-due federal debt, and the property must be the principal residence |

| Factors to consider when deciding whether to refinance | Equity, credit score, and debt-to-income ratio |

Explore related products

What You'll Learn

![]()

FHA mortgage insurance reduction makes financing more affordable

FHA mortgage insurance, also known as Mortgage Insurance Premium (MIP), is an additional payment made by the borrower to the lender to secure the loan. While MIP is mandatory for all FHA loans, the recent reduction in MIP rates has made FHA loans more affordable.

The FHA Mortgage Insurance Premium (MIP) is a type of insurance that protects the lender in case the borrower defaults on their FHA loan. It is required for all FHA loans, regardless of the down payment amount. The MIP includes an upfront premium, typically paid when the loan is taken out, and annual premiums paid over the life of the loan.

The recent reduction in FHA mortgage insurance premiums, which took effect on March 20, 2023, has made financing more affordable for borrowers. For FHA loans with a term longer than 15 years, the MIP rate has been reduced from 0.85% to 0.55% for loans of $726,200 or less. This reduction translates to significant savings for borrowers, with FHA homebuyers and homeowners expected to save an average of $800 per year, according to a HUD press release.

In addition to the recent reduction, there are other ways to reduce or eliminate FHA mortgage insurance. One way is through automatic termination, which depends on when the FHA loan was taken out and the original down payment amount. For loans taken out before June 3, 2013, with a down payment of at least 10%, MIP can be removed after 5 years. For loans taken out on or after June 3, 2013, with a similar down payment, MIP will be removed after 11 years.

Another way to eliminate FHA mortgage insurance is through refinancing to a conventional loan. This option is suitable if you have sufficient home equity (typically 20% or more), a strong credit score, and a low debt-to-income ratio. By refinancing, you can remove the mortgage insurance requirement and potentially save money in the long term. However, it is important to consider the closing costs associated with refinancing and ensure that the upfront cost will be offset by future savings.

The FHA mortgage insurance reduction has made financing more affordable for borrowers, providing greater accessibility to homeownership. With lower MIP rates, borrowers can save money on their monthly payments and qualify for loans that may have previously been out of reach.

Report Car Crashes: Insurance Claim Steps

You may want to see also

Explore related products

$13.25

![]()

FHA mortgage insurance removal options

FHA mortgage insurance, also known as Mortgage Insurance Premium (MIP), is an additional payment made by the borrower to the lender to secure the loan. It is a way to protect the lender's financial interest in case of default on an FHA mortgage. Beginning March 20, 2023, mortgage insurance premiums will be lower on most FHA loans, making payments more affordable and qualifying easier.

There are two main ways to remove FHA mortgage insurance: automatic termination and refinancing. The eligibility criteria for automatic MIP cancellation depend on when you took out your FHA loan and your original down payment amount.

Automatic Termination

If your FHA loan was taken out before June 3, 2013, you can remove MIP after 5 years if your original down payment was at least 10% of the purchase price. If your down payment was less than 10%, you will generally need to pay MIP for the life of the loan, unless you refinance.

For loans taken out on or after June 3, 2013, MIP can be removed after 11 years if the original down payment was at least 10%. Additionally, the loan must be in good standing, with all mortgage payments made on time, and the property must be the borrower's principal residence.

Refinancing

If you don't meet the criteria for automatic MIP cancellation, refinancing into a conventional loan is another option to remove FHA mortgage insurance. Refinancing involves taking out a new loan to pay off the existing FHA loan. To qualify for refinancing, you typically need to have at least 20% equity in your home, a strong credit score, and a low debt-to-income ratio.

It is important to evaluate your options carefully and consider the benefits of each approach. Removing MIP through automatic termination or refinancing can help lower your monthly mortgage payments. However, even if you qualify for MIP cancellation, refinancing may still be the most beneficial option in some cases.

Critical Illness Insurance: Is It Right for Your Employees?

You may want to see also

Explore related products

![]()

FHA mortgage insurance premiums (MIP)

FHA Mortgage Insurance Premium (MIP) is an additional payment made by the borrower to their lender to secure the loan. MIP is a way to protect the lender's financial interest in the case of default on an FHA mortgage. The Federal Housing Administration governs FHA loans, which often accommodate borrowers with lower credit scores, income, and cash-to-close compared to conventional loans.

There are two types of FHA loan insurance payable on an FHA loan: the upfront mortgage insurance premium (UFMIP) and the annual mortgage insurance premium (MIP). The upfront mortgage insurance premium (UFMIP) is charged as a lump sum of 1.75% of the loan amount. It is typically financed into the mortgage amount but can also be paid in full in cash. On the other hand, the annual mortgage insurance premium (MIP) is charged annually, divided by 12, and added to the monthly mortgage payment. The cost of annual MIP ranges between 15 and 75 basis points, which is 0.15% to 0.75% of the loan amount.

There are two main ways to remove FHA mortgage insurance: automatic termination and refinancing. If you qualify for automatic MIP termination, your mortgage insurance will be removed automatically after 11 years. However, if you don't meet the criteria, refinancing into a conventional loan is an option. To be eligible for FHA mortgage insurance removal, your loan must be in good standing, and you must meet specific requirements regarding payment history, outstanding loans, and property type.

FHA Mortgage Insurance: What You Need to Know About Payments

You may want to see also

Explore related products

![]()

FHA mortgage insurance eligibility

FHA mortgage insurance is mandatory for all FHA loans. It is a government guarantee to pay a lender's losses if you default on a loan. The insurance covers FHA-approved lenders and FHA loans on single-family homes, multifamily properties, manufactured homes, condos and co-ops.

There are two types of FHA loan insurance payable on an FHA loan: the upfront mortgage insurance premium (UFMIP) and the annual mortgage insurance premium (MIP). The upfront mortgage insurance premium is typically 1.75% of the loan amount, which can be financed into the mortgage amount or paid in full in cash. The annual mortgage insurance premium is charged annually, divided by 12 and added to your monthly payment. The cost of annual MIP ranges between 15 and 75 basis points, which is 0.15% to 0.75% of your loan amount. The cost varies based on factors such as the loan term, loan amount, and loan purpose.

FHA mortgage insurance is generally more expensive than private mortgage insurance (PMI) on a conventional loan, and it is required regardless of your down payment amount. However, FHA loans offer more flexibility in credit requirements and allow a minimum down payment of 3.5%.

FHA mortgage insurance premiums are not tax-deductible, but you may be eligible for a partial refund of your upfront MIP if you refinance your existing FHA loan through an FHA Streamline Refinance. Additionally, making a larger down payment of 10% or more can help you avoid paying MIP for the entire loan term.

Is Extra SIPC Insurance Coverage Necessary?

You may want to see also

Explore related products

![]()

FHA mortgage insurance refunds

If you have an FHA-insured mortgage, you may be eligible for a refund from the US Department of Housing and Urban Development (HUD). The HUD's Office of Financial Services - Single Family Insurance Operations Division (SFIOD) is responsible for paying eligible homeowner refunds.

To be eligible for a refund, you must have closed on your FHA loan within the past 180 days or within the last three years, depending on the source. You must also be current on your mortgage payments and cannot have any foreclosures listed on your credit report. Additionally, you can only receive a refund if you refinance your existing FHA loan into another FHA loan, such as an FHA Streamline Refinance or an FHA Cash-out Refinance.

The refund amount depends on how long you wait to refinance your loan. If you refinance within 12 months, you will receive a refund of 58% of your upfront payment. If you wait three years to refinance, your refund will be equal to 10% of your upfront payment. It's important to note that you won't receive your refund as a cash payment. Instead, the refund will be applied to the upfront Mortgage Insurance Premium (MIP) payment you need to make when you refinance your loan.

To apply for a refund, you can submit all the documentation related to your application to the FHA via email, fax, upload, or mail. You can also authorise a third party tracer to fill out a HUD-27050-B form and apply for a refund on your behalf.

Mortgage Loan: Insurance and Taxes Included?

You may want to see also

Frequently asked questions

An FHA MIP is an additional payment made by the borrower to secure the loan. It is a way to protect the lender in case the borrower defaults on the loan.

Beginning March 20, 2023, FHA mortgage insurance premiums were reduced, making payments more affordable. For FHA borrowers with a loan term of more than 15 years, the annual MIP was reduced from 0.85% to 0.55%.

There are two main ways to remove FHA mortgage insurance: automatic termination and refinancing. Automatic termination depends on when you took out your FHA loan and your original down payment amount. If you don't meet the criteria for automatic termination, you can consider refinancing to a conventional loan.

To be eligible for FHA mortgage insurance removal through refinancing, you must meet certain requirements. Your loan must be in good standing, you must have a good payment history, and your property must be your principal residence. Additionally, you will need sufficient home equity, a strong credit score, and a low debt-to-income ratio.

If you are considering refinancing to remove FHA mortgage insurance, you should evaluate your options by considering factors such as equity, credit score, and debt-to-income ratio. You will need at least 20% equity in your home and a credit score of at least 620 to qualify for a conventional refinance.