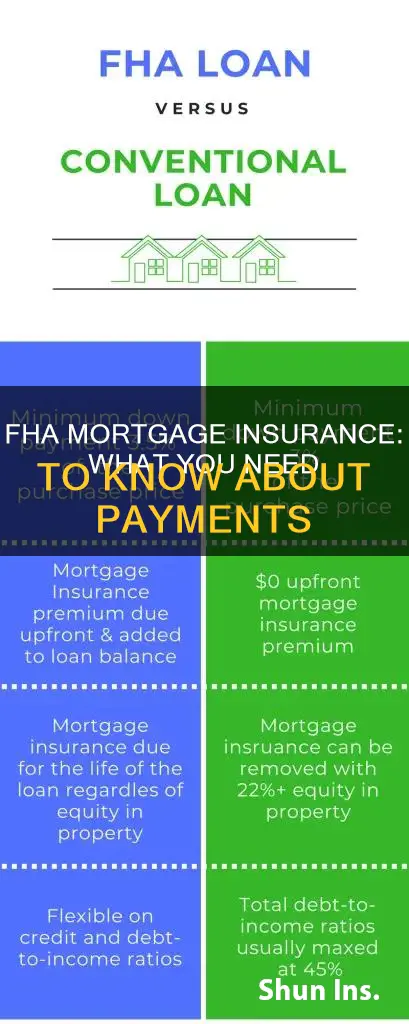

FHA mortgage insurance, also known as FHA MIP, is an additional fee that all borrowers of FHA loans must pay. It includes an upfront premium, typically paid at closing, and annual premiums. The upfront premium is 1.75% of the loan amount, while the annual premium varies based on the loan amount, size of the down payment, and loan term. FHA mortgage insurance is paid into the Mutual Mortgage Insurance Fund (MMIF) and protects the lender in case the borrower defaults. While some FHA borrowers can get rid of their monthly mortgage insurance premiums, most will need to refinance their loan or pay it off completely to eliminate this expense.

| Characteristics | Values |

|---|---|

| FHA mortgage insurance removal | Possible for many homeowners |

| Possibility of natural FHA mortgage insurance removal | When insurance lapses |

| FHA mortgage insurance removal eligibility | Depends on factors like down payment, loan term, and loan amount |

| FHA mortgage insurance premium (MIP) | Mandatory for all FHA loans |

| FHA upfront mortgage insurance premium (UFMIP) | 1.75% of the loan amount, paid at closing or rolled into the loan amount |

| Annual MIP | 0.85% of the loan balance paid annually or broken down into 12 monthly payments |

| Partial refund of UFMIP | Applicable if refinancing or selling within the first 3 years of the loan term |

| Refinancing | May eliminate existing monthly mortgage insurance premiums |

Explore related products

$0.99 $15.99

What You'll Learn

![]()

FHA mortgage insurance removal

If you refinance or sell your home within the first 3 years of your loan term, you may be able to get a partial refund of your Upfront Mortgage Insurance Premium (UFMIP). The amount of your potential refund depends on how far into your loan term you are when you refinance or sell. Here’s a breakdown of the refund percentages:

- If you refinance or sell within the first 12 months: 80% refund

- If you refinance or sell between months 13-24: 60% refund

- If you refinance or sell between months 25-36: 40% refund

For mortgages with an FHA case number assignment date on or after June 3, 2013, the FHA insurance can be terminated by the servicer or holder if the mortgage is paid in full before the maturity date. If your mortgage originated before June 3, 2013, you’d need to meet the following conditions:

- You’ve made all monthly mortgage payments on time

- You’ve paid for at least 5 years of a 20, 25 or 30-year loan (there’s no time limit for a 15-year mortgage)

- Your mortgage has a 78% or less loan-to-value ratio (LTV)

If your loan was finalized on or after June 3, 2013, you’d need to have made a 10% or larger down payment when purchasing the home and have made on-time mortgage payments for the last 11 years. Unfortunately, if you don’t meet either set of the above conditions, you won’t be able to cancel your MIP while keeping your FHA loan intact.

However, if you’re determined to get rid of your mortgage insurance, you can apply to refinance your FHA loan into a conventional mortgage, but you’ll have to meet specific requirements. To remove PMI or MIP on an existing loan, refinance once your home reaches 20 percent equity. For a new loan type, consider options like piggyback loans, lender-paid mortgage insurance, or specialized programs without PMI.

DirectPay Pet Insurance: Worth the Cost?

You may want to see also

Explore related products

![FHA Multi-Family Housing Mortgage Insurance Program... Hearing... S. Hrg. 107-534... Committee On Banking, Housing, & Urban Affairs, United States Senate... 107th Congress, 1st Session [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

Upfront Mortgage Insurance Premium (UFMIP)

UFMIP is designed to protect the lender in case the borrower defaults on their mortgage payments. FHA loans have lower down payment requirements, as low as 3.5% of a home's price tag, and less stringent income and credit requirements than conventional loans. Therefore, the risk to the lender of the borrower defaulting is higher, and UFMIP helps to reduce this risk.

It is important to note that UFMIP is non-refundable in most cases, except when the borrower refinances to a new FHA-insured mortgage within 3 years of the original loan. The partial refund percentages for refinancing or selling within the first 5 years are outlined as follows:

- If you refinance or sell within the first 12 months: 80% refund

- If you refinance or sell between months 13-24: 60% refund

- If you refinance or sell between months 25-36: 40% refund

UFMIP is a requirement for FHA home loans, and borrowers must also pay monthly MIP payments, which range from 0.45% to 1.05% of the loan amount. The duration of these payments depends on the down payment amount, with a down payment of less than 10% resulting in MIP payments for the life of the loan, and a down payment of 10% or more resulting in MIP payments for only the first 11 years.

Reporting Suspected Social Security Insurance Fraud: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Annual MIP

FHA mortgage insurance premiums (MIP) are mandatory for all borrowers, regardless of their down payment. The Federal Housing Administration (FHA) is not a mortgage lender; instead, it's an insurance provider for lenders. When you get an FHA loan, your lender provides the money, and the FHA insures the loan.

The annual MIP rate varies based on the size, term, and loan-to-value (LTV) ratio of the loan. Most borrowers pay 0.85% of their loan balance each year in annual MIP. For a $250,000 loan balance, 0.85% equals $2,125, which would be broken down into 12 monthly payments of about $177 each. The FHA charges a different annual insurance rate for some loans. The annual mortgage premium costs between 0.15% and 0.75% of the loan amount.

There are a few ways to remove or avoid paying annual MIP. Firstly, if you put 10% or more down on your loan, the annual MIP will automatically be removed after 11 years of payments. Secondly, if you closed your loan before June 3, 2013, the annual MIP will be removed once your loan balance reaches 78% of your home's value. Lastly, you can refinance your FHA loan into a conventional loan without MIP or pay off the loan entirely to eliminate the annual MIP.

Switching Home Insurance: A Simple Guide

You may want to see also

Explore related products

![]()

Private mortgage insurance (PMI)

PMI is arranged by the lender and provided by private insurance companies. It protects the lender against losses caused by borrowers failing to make loan payments. It is important to note that PMI does not protect the borrower, and they can still lose their home through foreclosure if they fall behind on their mortgage payments.

PMI can be paid in different ways. Sometimes, it is paid as a one-time upfront premium at closing, and the amount is shown on the Loan Estimate and Closing Disclosure. Other times, it is paid through both upfront and monthly premiums, with the monthly premium added to the monthly mortgage payment.

Borrowers can request to cancel PMI when their mortgage balance reaches 80% of their home's value. Federal law dictates that lenders must automatically end PMI when the loan-to-value (LTV) ratio drops to 78%, or when the borrower passes the midpoint of their loan term. To prove that their home equity has reached 20%, borrowers may need to get their home reappraised by a professional appraiser or broker.

PMI should not be confused with mortgage insurance premium (MIP), which is specific to FHA loans and is required for all borrowers, regardless of their down payment. While PMI is associated with conventional loans, it can typically be removed once the homeowner builds enough equity.

Assessing Home Value for Insurance

You may want to see also

Explore related products

$15.95

$10.49 $28.95

![]()

Removing FHA mortgage insurance without refinancing

FHA mortgage insurance, also known as FHA MIP, is required for all borrowers, regardless of their down payment. It is not to be confused with private mortgage insurance (PMI), which is for conventional loans. FHA MIP usually lasts 11 years or for the life of the loan.

- If you put 10% or more down, your annual MIP will be removed after 11 years of payments.

- If your loan was closed before June 3, 2013, your annual MIP will be removed once your loan balance reaches 78% of your home's value.

- If your loan doesn't qualify for automatic cancellation, you can request cancellation by writing to your mortgage servicer. To be eligible for this, your loan-to-original-value (LTOV) ratio must be below 80%.

- An FHA Streamline Refinance allows you to refinance your existing FHA loan to a lower interest rate without a new appraisal or income verification. While this won't eliminate your MIP, it could lower your overall mortgage payment.

If you are considering refinancing, it is important to note that you will need to pay closing costs, so be sure to do the math and determine if the upfront cost will be worth the savings in the long run. Additionally, if you refinance to a conventional loan with an LTV ratio of 80% or higher, you may still need to pay for mortgage insurance, and PMI could be pricier than FHA MIP.

FHA Insurability: Home Renovation Tips

You may want to see also

Frequently asked questions

It is an insurance policy that protects the lender if the borrower defaults. It includes an upfront premium, typically paid at closing, and annual premiums.

The upfront premium is 1.75% of the loan amount, while the annual premium varies based on the size, term and loan-to-value (LTV) ratio of the loan.

Yes, if you refinance or sell your home within the first 3 years of your loan term, you may be eligible for a partial refund of your upfront premium. The amount of the refund depends on how far into your loan term you are when you refinance or sell.

In most cases, you will need to refinance into another type of loan to eliminate this expense. However, some FHA loan holders may be able to get rid of their mortgage insurance premiums without refinancing by making payments for 11 years or paying off their loan.

No, it is not tax-deductible.