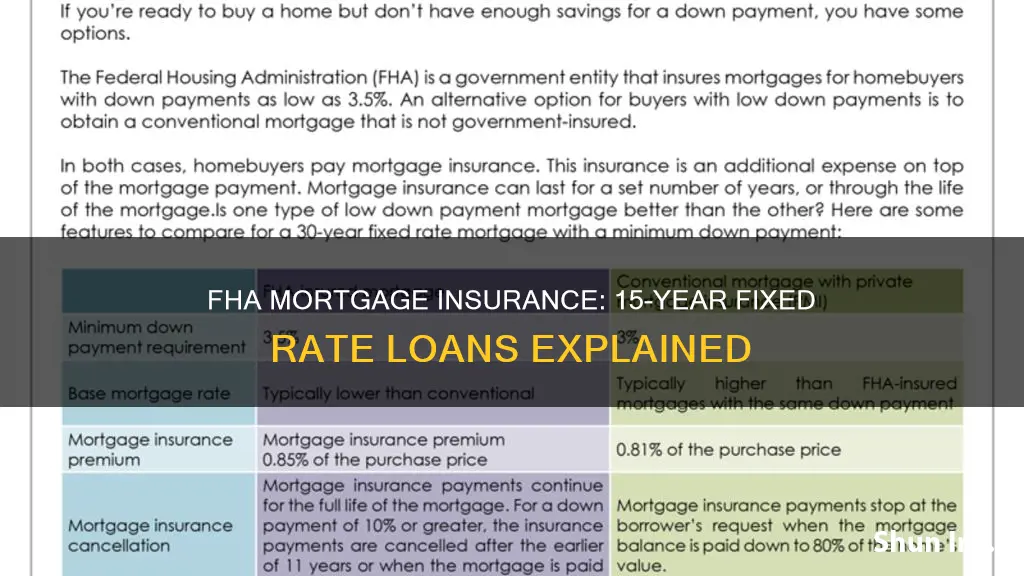

FHA mortgage insurance is a type of policy that protects lenders against losses that result from defaults on home mortgages. FHA requires both upfront and annual mortgage insurance for all borrowers, regardless of the amount of down payment. The cost of FHA mortgage insurance varies based on factors such as the loan amount, the size of the down payment, and the loan term. For example, if you borrow a loan amount greater than or equal to $726,200 for a term less than 15 years, your annual MIP will be reduced to 65 basis points. On the other hand, if you opt for a shorter term like a 15-year mortgage, you will benefit from lower mortgage insurance premiums.

| Characteristics | Values |

|---|---|

| FHA Mortgage Insurance Purpose | Protects lenders against losses that result from defaults on home mortgages |

| FHA Mortgage Insurance Requirements | Required for all borrowers, regardless of the amount of down payment |

| FHA Mortgage Insurance Cost | Varies based on the LTV ratio, loan term, and loan amount |

| FHA Mortgage Insurance Premium (MIP) | Paid at closing and on a monthly basis until the loan-to-value (LTV) reaches the prescribed limit |

| FHA Mortgage Insurance Duration | Paid for the life of the loan if the down payment is less than 10%; paid for 11 years if the down payment is 10% or more |

| FHA Loan Term Options | Typically 15 or 30 years |

| FHA Loan Amount Threshold | Loans greater than $726,200 have a higher annual MIP of 65 basis points |

| FHA Mortgage Insurance Calculation | Multiplying the base loan amount by the MIP rate and dividing by 12 to get the monthly MIP |

Explore related products

What You'll Learn

- FHA mortgage insurance protects lenders against losses

- Annual premiums range from 0.15% to 0.75% of the loan balance

- The cost varies depending on the loan amount and term

- FHA requires upfront and annual insurance, regardless of down payment

- MIP is paid until the loan-to-value reaches the prescribed limit

![]()

FHA mortgage insurance protects lenders against losses

FHA mortgage insurance, also known as Mortgage Insurance Premium (MIP), is a policy that protects lenders against losses that may result from defaults on home mortgages. It is a mandatory requirement for all borrowers, regardless of the amount of down payment. This insurance allows lenders to provide more flexible benefits and varying programs, such as fixed-rate loans.

The cost of FHA mortgage insurance varies based on the Loan to Value (LTV) ratio, which is calculated by dividing the loan amount by the home's value. A higher loan amount results in a higher LTV ratio. The loan term also impacts the cost, with shorter-term loans, such as a 15-year mortgage, offering lower mortgage insurance premiums.

The FHA mortgage insurance includes an upfront charge, typically financed into the loan amount, and a monthly premium included in the mortgage payment. The upfront charge, known as the Upfront Mortgage Insurance Premium (UFMIP), is usually 1.75% of the loan amount, while the monthly premium, or annual MIP, ranges from 0.15% to 0.75% of the loan amount.

While FHA mortgage insurance protects lenders, it also benefits borrowers by making it easier for them to qualify for loans. The insurance allows lenders to be more willing to approve applicants with lower credit scores and smaller down payments. Additionally, FHA mortgage insurance can be removed or mitigated through various options, such as obtaining down payment assistance or refinancing into a conventional loan without mortgage insurance.

Overall, FHA mortgage insurance plays a crucial role in protecting lenders against potential losses while also facilitating homeownership for borrowers who may not meet conventional loan requirements.

Insurance Claims: Minor Fender Benders, What to Do?

You may want to see also

Explore related products

$13.25

![]()

Annual premiums range from 0.15% to 0.75% of the loan balance

FHA mortgage insurance, also known as Mortgage Insurance Premium (MIP), is a policy that protects lenders from losses if borrowers default on their loans. It is mandatory for all FHA borrowers, regardless of the down payment amount. The cost of FHA mortgage insurance varies based on factors such as the loan amount, the size of the down payment, and the loan term.

For loans with terms longer than 15 years, the annual MIP ranges from 0.15% to 0.75% of the average outstanding loan balance. This range of 15 to 75 basis points translates to a percentage of your loan amount, with a lower percentage for larger down payments. For example, if you have a 30-year fixed-rate FHA mortgage and make the minimum down payment of 3.5%, your MIP will be 0.55%.

The loan term also affects the MIP rate. For instance, FHA borrowers who previously paid 0.80% annually towards MIP now pay 0.50% for loan terms longer than 15 years. Additionally, the loan amount plays a role in determining the MIP rate. Loan amounts greater than $726,200 with a Loan to Value (LTV) greater than 90% and a term of up to 15 years will have an annual MIP of 65 basis points.

It is important to note that FHA mortgage insurance cannot be canceled if the down payment is less than 10%. However, if you put down at least 10%, you will only pay MIP for 11 years instead of the entire loan term. Furthermore, refinancing an FHA loan into a non-FHA loan is another way to eliminate MIP payments.

Mortgage Insurance: Is It a Must-Have?

You may want to see also

Explore related products

![]()

The cost varies depending on the loan amount and term

FHA mortgage insurance is a policy that protects lenders from losses that may result from defaults on home mortgages. The Federal Housing Administration (FHA) requires both upfront and annual mortgage insurance for all borrowers, regardless of the amount of the down payment. The cost of FHA mortgage insurance varies depending on the loan amount and term.

The loan amount is determined by the lender, who divides the loan amount by the value of the home to determine the loan-to-value (LTV) ratio. The higher the loan amount, the higher the LTV ratio. The LTV ratio is a key factor in determining the cost of FHA mortgage insurance.

The loan term is the length of time the borrower chooses to repay the loan, typically 15 or 30 years for FHA loans. A shorter-term loan, such as a 15-year mortgage, will have lower mortgage insurance premiums than a longer-term loan. For example, for a loan term of more than 15 years, the annual MIP for loans greater than $726,200 with a Loan to Value of greater than 90% will be reduced to 65 basis points. On the other hand, if you choose a 30-year fixed-rate FHA mortgage and make a minimum down payment of 3.5%, your MIP will be 0.55%.

The cost of FHA mortgage insurance is typically calculated as a percentage of the loan amount, ranging from 0.15% to 0.75% of the average outstanding loan balance. This means that the higher the loan amount, the higher the cost of FHA mortgage insurance. Additionally, the size of the down payment can also affect the cost of FHA mortgage insurance. A larger down payment can help shorten the amount of time the borrower needs to pay the insurance, as MIP will go away after 11 years if the down payment is at least 10%.

It is important to note that FHA mortgage insurance cannot be canceled if the down payment is less than 10%. To get rid of FHA mortgage insurance payments, borrowers may need to refinance the mortgage into a non-FHA loan or pay off the loan early.

Stolen Reports: Insurance Claims and Acceptance

You may want to see also

Explore related products

![]()

FHA requires upfront and annual insurance, regardless of down payment

FHA mortgage insurance, also known as MIP (mortgage insurance premium), is a type of policy that protects lenders against losses that result from defaults on home mortgages. This type of insurance is required for all FHA loans, regardless of the down payment amount.

There are two types of FHA mortgage insurance premiums: upfront and annual. The upfront mortgage insurance premium, also known as UFMIP, is typically paid as a lump sum at closing and is equal to 1.75% of the total loan amount. This fee can also be rolled into the total loan cost and paid as part of the monthly mortgage payment. The annual mortgage insurance premium, on the other hand, is charged annually and is based on factors such as the down payment size and total loan amount. The annual MIP ranges between 0.15% to 0.75% of the loan amount.

It's important to note that FHA mortgage insurance is generally more expensive than private mortgage insurance (PMI) on a conventional loan. Additionally, while PMI can be removed once the borrower reaches a certain level of equity in their home, MIP is required for the life of the loan unless the borrower provides a larger down payment (typically 10% or more) at closing. In that case, MIP can be cancelled after 11 years.

FHA loans are a popular option for first-time homebuyers who may not have saved enough for a large down payment. By offering flexible benefits and varying programs, FHA-approved lenders can provide borrowers with options such as fixed-rate loans and adjustable-rate mortgages (ARMs). However, it's important to consider the long-term costs of FHA mortgage insurance when budgeting for a home loan.

While a larger down payment won't help you avoid FHA mortgage insurance, it can reduce the monthly MIP costs and shorten the amount of time you'll need to pay it. Additionally, opting for a shorter loan term, such as a 15-year mortgage, can result in lower mortgage insurance premiums.

Amica Insurance: Worth the Money or Not?

You may want to see also

Explore related products

![]()

MIP is paid until the loan-to-value reaches the prescribed limit

Mortgage Insurance Premium (MIP) is a type of insurance that is associated with Federal Housing Administration (FHA) loans. It is a form of protection for lenders in the event that a borrower defaults on their loan. FHA loans are considered higher risk due to lower credit scores and smaller down payments, so MIP is required for all borrowers to compensate lenders in case of defaults.

MIP includes an upfront premium, typically paid when the loan is issued, and annual premiums. The upfront premium is usually 1.75% of the total loan amount, while the annual premium ranges from 0.15% to 0.75% of the loan amount. The annual premium depends on factors such as the loan amount, loan term, and down payment.

The length of time a borrower pays MIP on an FHA loan depends on various factors, including the origination date of the loan and the down payment amount. For loans originated before June 3, 2013, with a down payment of at least 10%, MIP can be removed after 5 years. However, if the down payment was less than 10%, MIP typically remains for the life of the loan.

For loans originated after June 3, 2013, the guidelines are similar. If the original down payment was at least 10%, MIP can be removed after 11 years. However, if the down payment was less than 10%, the borrower must pay MIP for the entire loan term.

It's important to note that the only way to eliminate MIP on FHA loans originated after June 3, 2013, is by paying off the loan or refinancing to a non-FHA loan. Additionally, borrowers with FHA loans greater than $726,200 and terms less than or equal to 15 years will have a reduced annual MIP of 65 basis points.

Mortgage Insurance: Statement Appearance and What It Means

You may want to see also

Frequently asked questions

FHA mortgage insurance is a policy that protects lenders against losses that result from defaults on home mortgages.

The cost of FHA mortgage insurance varies based on your LTV ratio, loan term, and loan amount. The insurance premium ranges from 0.15% to 0.80% of the loan amount.

If your down payment is less than 10% of the purchase price, you will need to pay FHA mortgage insurance for the entire loan term. If you put down at least 10%, you will pay mortgage insurance premiums for 11 years.

The lender calculates the monthly Mortgage Insurance Premium (MIP) as a percentage of the loan amount based on the LTV ratio and loan term. For a 30-year fixed-rate FHA mortgage with a minimum down payment of 3.5%, the MIP will be 0.55%.