Hazard insurance is a type of financial protection for homeowners that covers the costs of repairing or rebuilding a property damaged by natural disasters, including fires, storms, lightning, explosions, and theft. It is a subsection of homeowners insurance, and mortgage lenders often require borrowers to have it as it also protects their investment in the property. Hazard insurance does not cover all types of damage, and additional policies may be required depending on the location of the property.

| Characteristics | Values |

|---|---|

| Definition | Hazard insurance is a subsection of homeowners insurance that covers damage to the home's structure. |

| Purpose | It provides financial protection and peace of mind to homeowners against damage caused by natural disasters and other hazards. |

| Requirements | Mortgage lenders often require borrowers to have hazard insurance as part of their homeowners insurance policy. The amount and specific coverage required may vary by lender and location. |

| Coverage | Fire, wind, hail, snow, lightning, theft, vandalism, explosions, and damage from fallen trees or vehicles. |

| Exclusions | Floods, earthquakes, and hurricanes may be excluded in some regions, and additional policies may be required for these perils. |

| Cost | The cost of hazard insurance can be included in the homeowner's insurance premium, or lenders may offer an escrow account to split the annual premium into monthly payments. |

| Cancellation | Hazard insurance is typically required until the mortgage is paid off. Cancelling it will make the homeowner fully responsible for any property damage or loss. |

Explore related products

What You'll Learn

![]()

Hazard insurance is a subsection of homeowners insurance

While hazard insurance is essential for protecting your property, it is important to note that it only covers damage to the structure of your home, including the roof and foundation. Any personal belongings or liability damages are not typically covered under hazard insurance. Therefore, it is often bundled with homeowners insurance to provide a more comprehensive coverage plan.

Homeowners insurance, on the other hand, covers a broader range of risks, including damage to the home, personal property, and liability damages. When purchasing a home, most mortgage lenders will require you to have homeowners insurance, which includes hazard insurance coverage. This ensures that the lender is protected in case of any damage to the property.

The cost of hazard insurance can vary depending on various factors, including the value of the home, policy limits, and deductible amount. Additionally, the specific coverage provided by hazard insurance can differ depending on the policy. It is important for homeowners to carefully review their policy to understand what types of hazards are covered and whether additional coverage is needed for specific risks, such as flooding or earthquakes.

Overall, hazard insurance is a crucial component of homeowners insurance, providing financial protection and peace of mind for property owners in the event of natural disasters or other hazards. By understanding the coverage provided and any potential gaps, homeowners can ensure they have the necessary protection in place for their homes and belongings.

Ryanair Insurance: Worth the Cost?

You may want to see also

Explore related products

$12 $24.99

$4.99 $14.99

$9.97

![]()

It covers damage to the structure of the home

Hazard insurance is an essential part of protecting your property as a homeowner. It is a subsection of homeowners insurance and not separate home insurance coverage. It is often required when qualifying for a mortgage. Hazard insurance covers damage to the structure of the home, including the roof, walls, floors, and foundation. This includes damage caused by fires, severe storms, lightning, hail, sleet, wind, snow, smoke, theft, and vandalism. It can also cover damage caused by explosions, usually from gas leaks, and damage caused by fallen trees or vehicles colliding with the home.

It is important to note that hazard insurance does not cover all types of damage. For example, it typically does not include damage from flooding, earthquakes, or hurricanes in some regions. Homeowners in areas prone to certain risks, such as floods, landslides, or earthquakes, may need to purchase separate or additional insurance policies to cover these specific contingencies.

The amount of hazard insurance required depends on the value of the home and the cost of replacing it in the event of a total loss. Mortgage lenders often require borrowers to maintain hazard coverage through a homeowners insurance policy to protect their investment in the property. This helps ensure that homeowners have the financial means to repair or rebuild their homes in the event of a covered loss, reducing the risk of foreclosure and repossession.

To find the best hazard insurance for their needs and budget, homeowners should get multiple quotes and carefully review the coverage offered. Speaking with an insurance agent and their mortgage lender can help ensure that they have the necessary coverage for their area and meet any lender requirements.

Writing Damage Reports: A Guide for Insurance Claims

You may want to see also

Explore related products

![]()

It does not cover flooding, earthquakes or hurricanes

Hazard insurance is an essential part of protecting your property as a homeowner. It provides financial protection against damage to the structure of your home and surrounding structures, such as a garage. This includes damage caused by fires, storms, lightning strikes, hail, explosions, vandalism, and theft.

However, it is important to note that hazard insurance does not cover flooding, earthquakes, or hurricanes in some regions. While hazard insurance covers a range of natural disasters, these three events are often excluded from coverage. This exclusion is because flooding, earthquakes, and hurricanes can cause extensive and costly damage, and insurers consider them too high-risk to insure under a standard hazard insurance policy.

Homeowners in areas prone to flooding, earthquakes, or hurricanes should be aware of this exclusion and take steps to protect themselves financially. They may need to purchase separate insurance policies or add-ons specifically for these hazards. For example, flood insurance policies are available to protect against flooding, and earthquake insurance can provide additional coverage in areas prone to seismic activity.

The specific coverage provided by hazard insurance can vary depending on the region and the insurance provider. Therefore, it is essential to carefully review the terms and conditions of your policy to understand what is and is not covered. Additionally, speaking with an insurance agent or broker can help clarify the details of your coverage and identify any gaps that may need to be addressed with additional policies or add-ons.

In summary, while hazard insurance provides valuable protection against a range of natural disasters, it is important to be aware of its limitations. By understanding what is not covered, homeowners can take the necessary steps to ensure they have adequate protection in the event of flooding, earthquakes, or hurricanes.

Mortgage Insurance: Protecting Your Home and Finances

You may want to see also

Explore related products

![]()

It is required by mortgage lenders to protect their investment

Mortgage insurance is a policy that protects a mortgage lender or title holder in the event that the borrower defaults on payments, dies, or is otherwise unable to meet the contractual obligations of the mortgage. Hazard insurance, specifically, is a type of mortgage insurance that covers physical damage to the property from fires, floods, storms, and other natural hazards. This type of insurance is typically required by lenders to protect their investment and ensure that the property maintains its value throughout the life of the loan.

The primary purpose of hazard insurance is to protect the lender's investment by ensuring that they will not suffer a financial loss if the property is damaged or destroyed. Should something happen to the property, the lender is guaranteed compensation to cover the remaining loan balance. This is especially important for lenders when the outstanding loan amount is higher than the property's market value, a situation known as being "upside down" or "underwater" on the mortgage.

Hazard insurance policies typically cover damage from fires, lightning strikes, windstorms, and hail. They may also include protection against vandalism and theft. Additionally, lenders in certain areas may require borrowers to purchase additional coverage for specific risks, such as flood or earthquake insurance. Without this extra coverage, lenders may refuse to approve a loan. This is because the lender could be left with a property that has decreased in value significantly or even become uninhabitable.

The cost of hazard insurance can vary depending on several factors, including the location and value of the property, as well as the borrower's credit score and claims history. Borrowers usually pay the premiums as part of their monthly mortgage payments, with the lender being responsible for ensuring that the insurance payments are made on time and keeping a close eye on the policy to make sure it remains valid. While the lender is the beneficiary of the policy, the borrower owns the policy and has the right to file a claim and receive payment for repairs or rebuilding.

In summary, hazard mortgage insurance is a crucial protection for lenders, ensuring that their investment is secure even in the face of unforeseen events. By requiring this coverage, lenders can minimize their financial risk and maintain the value of their collateral. This, in turn, helps maintain stability in the housing market and contributes to the overall health of the economy. For borrowers, while it may add to the overall cost of owning a home, it also provides peace of mind and protection against the financial consequences of unexpected disasters.

Dorm Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

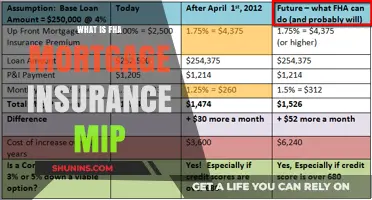

It is not the same as private mortgage insurance (PMI)

Hazard insurance is a subsection of homeowners insurance and not separate home insurance coverage. It is designed to provide compensation if sudden events damage your property structures, including fire, wind, hail, and snow. It protects your home from natural disasters like fires, storms, earthquakes, and other events that may vary by policy and location. It is usually a requirement when qualifying for a mortgage.

Private mortgage insurance (PMI), on the other hand, is a type of insurance that you may be required to purchase if you take out a conventional loan with a down payment of less than 20% of the purchase price. It is designed to protect the lender, not the borrower, in the event that they default on their loan. It is important to note that PMI does not protect the borrower from the negative repercussions of foreclosure.

While both types of insurance are related to mortgages, they serve different purposes. Hazard insurance is designed to protect the homeowner and their property, while PMI is designed to protect the lender in the event of non-payment. Additionally, hazard insurance is typically bundled as a part of homeowners insurance, whereas PMI is a separate type of insurance that is purchased specifically for mortgages.

Furthermore, the requirements for hazard insurance and PMI can vary. While most mortgage lenders require homeowners insurance, which includes hazard insurance, as part of buying a house, the requirement to buy PMI usually applies when the borrower has less than 20% equity in their home. In some cases, lenders may offer conventional loans with smaller down payments that do not require PMI, but these loans typically come with a higher interest rate.

In summary, while both hazard insurance and PMI are important considerations when obtaining a mortgage, they serve distinct purposes and offer different types of protection. Hazard insurance provides financial protection for the homeowner and their property, while PMI safeguards the lender in the event of non-payment.

Contraception and Insurance: What's the Link?

You may want to see also

Frequently asked questions

Hazard insurance is a subsection of homeowners insurance that covers damage to the structure of the home. It is designed to provide financial protection to the homeowner in the event of damage caused by natural disasters, such as fires, storms, and earthquakes.

Hazard insurance covers damage to the physical structure of the home, including the roof, walls, floors, and foundation. It also covers other nearby structures, such as a garage. In addition, hazard insurance can provide coverage for damage caused by theft, vandalism, explosions, and lightning strikes.

Yes, mortgage lenders typically require homeowners to have hazard insurance as part of their homeowners insurance policy. This is to protect their investment in the property. The amount of hazard insurance required may vary depending on the lender and the location of the property.

It is generally difficult to remove hazard insurance from a mortgage as lenders rely on the financial protection it provides. Once the mortgage is paid off, you may be able to adjust the coverage or have the lender remove the mortgage lien, allowing you to remove the hazard insurance. However, this may vary depending on the lender and specific circumstances.