FHA mortgage insurance, also known as Mortgage Insurance Premium (MIP), is an added cost that borrowers must consider when taking out an FHA loan. It is a type of mortgage insurance that is mandatory for homeowners who take out loans backed by the Federal Housing Administration (FHA). Unlike conventional loans, which require private mortgage insurance (PMI) if a home down payment is less than 20% of the purchase price, FHA loans require MIP regardless of the down payment amount. The purpose of MIP is to protect lenders against losses that may result from defaults on home mortgages.

| Characteristics | Values |

|---|---|

| What is FHA Mortgage Insurance Premium (MIP)? | A type of mortgage insurance that is required of homeowners who take out loans backed by the Federal Housing Administration (FHA). |

| Who does it protect? | The lender, in the event of borrower default. |

| Who pays it? | All FHA loan borrowers. |

| When is it paid? | At closing, or added to the loan balance, and then annually, divided into monthly instalments. |

| How much is paid? | The upfront MIP rate is 1.75% of the total loan amount. The annual MIP ranges from 0.15% to 0.75% of the loan amount, with most borrowers paying 0.55%. |

| How long is it paid for? | For the duration of the loan term, unless certain conditions are met. If a down payment of 10% or more is made, MIP is only required for the first 11 years. |

| How to remove it? | By refinancing into a conventional loan. |

Explore related products

What You'll Learn

![]()

FHA mortgage insurance protects lenders against borrower default

FHA mortgage insurance, also known as Mortgage Insurance Premium (MIP), is an added cost that borrowers must consider when taking out an FHA loan. It is an additional payment made to secure the mortgage loan. FHA loans require borrowers to pay a mortgage insurance premium, which is typically mandatory regardless of the down payment amount. The insurance premium includes an upfront premium, usually paid at closing, and annual premiums. The upfront premium is typically 1.75% of the loan amount, while the annual premium varies depending on the loan size, term, and loan-to-value (LTV) ratio.

The length of time a borrower pays off their FHA loan affects the amount they pay towards FHA MIP. For example, a 30-year FHA loan with a 3.5% down payment will result in MIP payments for the entire loan term. However, if a borrower can make a 10% down payment, they may only need to pay MIP for the first 11 years. Additionally, borrowers who can afford to pay off their loans quicker and opt for a shorter term, such as a 15-year mortgage, will benefit from lower mortgage insurance premiums.

While FHA mortgage insurance protects lenders, it also benefits borrowers by making it easier to qualify for a loan. Without FHA mortgage insurance, lenders would likely require a much larger down payment from borrowers. FHA loans are a good option for first-time homebuyers who may not have saved enough for a large down payment. Even borrowers with bankruptcy or foreclosure history may qualify for an FHA-backed mortgage.

Borrowers can remove FHA MIP by refinancing into a conventional loan once they have built up enough equity in their home, typically 20% or more. At that point, they can switch to a conventional loan and cancel mortgage insurance altogether. It is important for borrowers to consider the total cost of their loan, including MIP, when comparing different loan options.

Kwik Fit Tyre Insurance: Worth the Cost?

You may want to see also

Explore related products

$13.25

![]()

MIP is mandatory for all FHA loans, regardless of down payment

Mortgage Insurance Premium (MIP) is an added cost that borrowers of FHA loans must pay. It is a type of mortgage insurance that is required of homeowners who take out loans backed by the Federal Housing Administration (FHA). The purpose of MIP is to protect lenders against losses that may result from defaults on home mortgages.

MIP is mandatory for all FHA loans, regardless of the down payment amount. This is because FHA loans are considered riskier for lenders due to their low down payment requirements, which can be as low as 3.5%. By requiring MIP, lenders can protect themselves against potential defaults.

The upfront MIP payment is typically due when you close on your FHA loan, and it is usually set at 1.75% of the total loan amount. However, borrowers have the option to add this cost to their loan balance if they prefer. After the upfront payment, borrowers will also be responsible for annual MIP payments, which are divided into monthly installments and continue throughout the loan term.

The length of time a borrower pays MIP on an FHA loan depends on the loan term and the down payment amount. For a 30-year FHA loan, if a borrower puts down 3.5%, they will pay MIP for the entire loan term. However, if they put down at least 10%, they will only pay MIP for the first 11 years. It's important to note that MIP rates may vary depending on the loan amount, loan term, and LTV ratio.

While MIP is mandatory for all FHA loans, borrowers can explore options to mitigate the cost. One option is to refinance into a conventional loan once they have built enough equity, typically 20% or more. At that point, borrowers may be able to cancel mortgage insurance altogether. Additionally, there are assistance programs available that can help boost the down payment, potentially reducing the overall MIP cost.

Farmers Insurance Subsidy Programs: Unraveling the Benefits for Farmers and Ranchers

You may want to see also

Explore related products

![]()

MIP costs vary depending on loan term, size, and LTV ratio

Mortgage Insurance Premium (MIP) rates are set by the Federal Housing Administration (FHA) and are based on the size of your loan and your loan's loan-to-value (LTV) ratio. The upfront MIP is always 1.75% of the loan amount, but the annual MIP varies depending on the loan term, size, and LTV ratio.

For FHA loans originated between December 31, 2000, and June 3, 2013, the MIP could be removed if the borrower paid off at least 78% of the loan-to-value amount. For loans originated after June 3, 2013, if the down payment was less than 10% of the home's value, the borrower must pay the MIP for the life of the loan.

The length of the mortgage term also affects the MIP amount. FHA loans are available in various term lengths, but the two main categories are terms longer than 15 years and terms of 15 years or less. For FHA loans longer than 15 years, the annual MIP ranges from 0.5% to 0.8% of the loan balance, depending on the loan amount and LTV ratio. The higher the loan amount or the lower the down payment, the higher the MIP. For shorter-term loans, the MIP rates drop to between 0.45% and 0.95%.

The loan-to-value ratio also plays a significant role in determining the MIP costs. A lower LTV ratio can help reduce the overall MIP costs. Borrowers can achieve a lower LTV ratio by increasing their down payment or utilising down payment assistance programs.

It is important to note that FHA MIP rates are subject to change and have been reduced in the past. For example, the US Department of Housing and Urban Development (HUD) reduced the annual FHA MIP by 30 basis points in February 2023.

Cheap Car Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

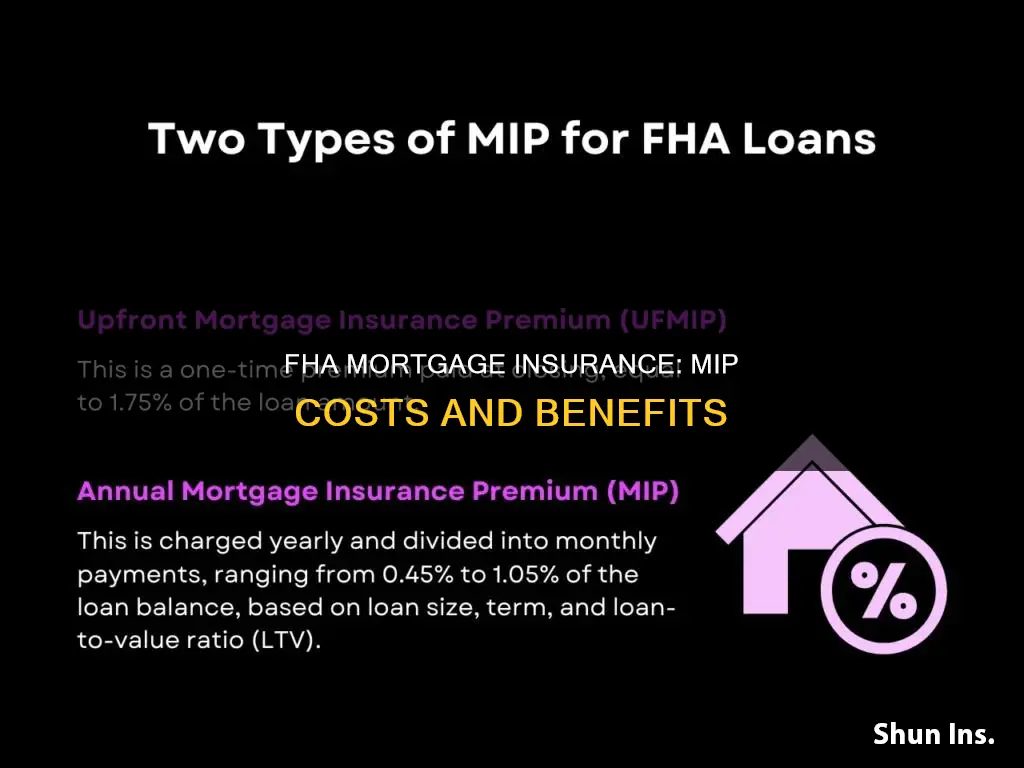

MIP can be paid upfront or added to the loan balance

Mortgage insurance is required for all FHA loans, regardless of the down payment amount. This insurance comes in the form of two components: an upfront mortgage insurance premium (UFMIP) and an annual Mortgage Insurance Premium (MIP). The UFMIP is a lump sum that is typically financed into the borrower's loan amount, resulting in a higher loan balance. Alternatively, borrowers also have the option to pay this amount out of pocket during the closing of the loan. On the other hand, the annual MIP is a monthly fee that is usually added to the borrower's monthly mortgage payment. This fee is based on a percentage of the loan amount, which is then divided by 12 to get the monthly cost.

The ability to finance the UFMIP into the loan balance provides flexibility for borrowers, especially those who may have financial constraints or prefer to maintain liquidity. By including the UFMIP in the loan, borrowers can avoid the need for a larger upfront cash outlay. This option can be particularly advantageous for those who plan to stay in their homes for an extended period, as it spreads the cost over the life of the loan.

However, it's important to note that financing the UFMIP will result in a higher loan balance, which in turn leads to paying more interest over the life of the loan. Additionally, the monthly MIP payments will also be slightly higher due to the increased loan amount. For borrowers who opt to pay the UFMIP upfront, this can reduce the overall cost of the loan, as they avoid paying interest on the UFMIP amount.

The annual MIP, which is paid monthly, is mandatory for the life of the FHA loan, regardless of the loan-to-value ratio. This differs from conventional loans, where private mortgage insurance (PMI) can be cancelled once the borrower reaches a certain level of equity in their home. However, for FHA loans originated after June 2013 with a term of more than 15 years and a down payment of less than 10%, the annual MIP will generally remain in place for the life of the loan. Loans that meet certain criteria may be eligible for MIP removal after 11 years, typically applying to loans with a higher down payment or shorter loan term.

Car Accident? Here's What to Do Next

You may want to see also

Explore related products

![]()

MIP can be removed by refinancing into a conventional loan

FHA loans are insured by the Federal Housing Administration (FHA). If a borrower defaults on their mortgage, the FHA compensates the lender for the outstanding balance. This insurance is funded by the Mutual Mortgage Insurance Fund (MMIF), which is, in turn, funded by the FHA Mortgage Insurance Premium (MIP) – an additional fee paid by the borrower. MIP includes an upfront premium, usually paid at closing, and annual premiums.

MIP is mandatory for all FHA loans, regardless of the down payment amount, and in most cases, it must be paid for the entire loan term. However, there are certain conditions under which MIP can be removed. For example, if your loan originated before June 3, 2013, you must have made all monthly mortgage payments on time and have paid for at least five years of a 20, 25, or 30-year loan. If your loan was finalised after this date, you must have made a 10% or larger down payment and have made on-time mortgage payments for the last 11 years.

If your FHA loan does not meet these criteria for MIP removal, you may be able to refinance it into a conventional loan. To do this, you will generally need to have built up 20% equity in your home. You will also need to pay closing costs, so it is important to consider whether the upfront cost of refinancing will be worth the savings in the long run. Refinancing can be beneficial for several reasons, including the potential for a lower interest rate and the ability to pay off your mortgage sooner.

Political Risk Insurance: Necessary Protection or Wasteful Expense?

You may want to see also

Frequently asked questions

FHA mortgage insurance MIP (Mortgage Insurance Premium) is an added cost that you'll need to pay on top of your mortgage payments if you take out an FHA loan. It protects the lender if you default.

FHA MIP includes two costs: an upfront premium, typically paid at closing, and annual premiums. The upfront premium is 1.75% of the total value of your loan. The annual premium varies depending on the size, term and loan-to-value (LTV) ratio of the loan, and typically ranges from 0.15% to 0.75% of the loan amount.

If you put down a deposit of at least 10%, you will pay MIP for 11 years. If you put down less than 10%, you will pay MIP for the entire loan term.