Private mortgage insurance (PMI) is a type of insurance that is required when borrowers make a down payment of less than 20% of the total cost of the home. PMI is typically paid monthly and the cost is added to the borrower's monthly mortgage payment. The insurance protects the lender in the event that the borrower falls behind on their payments, although it does not protect the borrower themselves. There are several different types of loans available to borrowers with low down payments, including FHA loans, USDA loans, VA-backed loans, and conventional loans.

| Characteristics | Values |

|---|---|

| Who needs to pay for mortgage insurance? | Borrowers making a down payment of less than 20% of the purchase price of the home. |

| When is mortgage insurance required? | On Federal Housing Administration (FHA) and U.S. Department of Agriculture (USDA) loans. |

| What does mortgage insurance do? | It lowers the risk to the lender of making a loan to the borrower, allowing the borrower to qualify for a loan they might not otherwise be able to get. |

| What types of mortgage insurance are there? | Private mortgage insurance (PMI) and mortgage insurance premium (MIP). |

| How is private mortgage insurance paid? | Monthly, with little or no initial payment required at closing. |

| Can private mortgage insurance be cancelled? | Yes, under certain circumstances. |

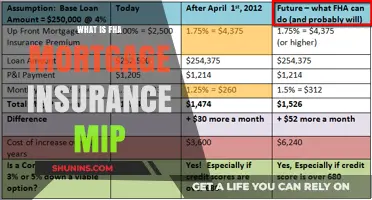

| How is mortgage insurance premium paid? | With FHA loans, part of the mortgage insurance premium is due upfront at closing (1.75% of the total loan amount), and the rest is paid annually. |

| Can mortgage insurance premium be cancelled? | It depends on the loan's origination date and other factors. |

Explore related products

$12.98 $17.99

What You'll Learn

![]()

Private mortgage insurance (PMI)

The requirement to buy PMI usually also applies when refinancing a conventional loan, when your equity is less than 20% of the value of your home. PMI is arranged by the lender and provided by private insurance companies. It is important to note that PMI does not protect you, the borrower; if you fall behind on your mortgage payments, you can still lose your home through foreclosure.

PMI rates vary by down payment amount and credit score but are generally cheaper than FHA rates for borrowers with good credit. Most PMI is paid monthly, with little or no initial payment required at closing. Under certain circumstances, you can cancel your PMI. For example, if you pay off 20% of the loan's value or after the loan is 15 years old, you may be able to cancel. Additionally, if your loan amount falls to 75-80% of your home's value, you may be able to cancel your PMI through a new appraisal.

Reporting Insurance Recoveries: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Federal Housing Administration (FHA) loans

Mortgage insurance is typically required for borrowers who make a down payment of less than 20% of the purchase price of the home. It lowers the risk to the lender and makes it more likely that they will offer you a loan. However, it increases the cost of your loan and does not protect you—if you fall behind on your payments, your credit score could suffer and you can lose your home through foreclosure.

FHA loans are a type of government-insured mortgage issued by an FHA-approved lender to help borrowers who don't meet conventional standards. They are designed to be easier to qualify for, especially for first-time buyers or those with less-than-perfect credit. The FHA insures these loans, so lenders are more willing to approve applicants with lower credit scores.

FHA loans are available to everyone, including those who can afford conventional mortgages, although they are principally designed for lower-income borrowers. Borrowers who can afford a substantial down payment may be better off with a conventional mortgage, as they can avoid the monthly mortgage insurance payments required by FHA loans.

FHA mortgage insurance is required for all FHA loans. It costs the same no matter your credit score, with only a slight increase in price for down payments of less than 5%. Some borrowers will pay mortgage insurance until they reach 20% equity in the home, while others will pay it for the entire duration of the loan until the mortgage is paid off or refinanced.

FHA Insured Mortgages: What You Need to Know

You may want to see also

Explore related products

![]()

When to pay mortgage insurance upfront

Mortgage insurance is typically required when borrowers make a down payment of less than 20% of the purchase price of the home. It lowers the risk to the lender in case the borrower is unable to repay the loan. Private mortgage insurance (PMI) is one such type of insurance that is arranged by the lender and provided by private insurance companies.

PMI can be paid in different ways, including monthly or upfront. Paying PMI upfront is called single-payment mortgage insurance, where the buyer pays part of the future mortgage insurance premiums at closing, and often at a discount. This option is not for everyone, as it requires the financial ability to afford a large payment at closing. However, it offers several advantages, including:

- Lowering the buyer's debt-to-income ratio, resulting in a reduced mortgage payment.

- Lowering the overall cost of the loan over time, as paying monthly PMI for three and a half years can quickly exceed the cost of a single upfront payment.

- Making it easier to qualify for a mortgage, as lenders use the ratio of monthly debt payments to monthly income to determine qualification.

- Avoiding the need to refinance the loan, as keeping the monthly payment low through single-payment mortgage insurance may be sufficient.

- Reducing the monthly payment, as paying PMI upfront means there are no ongoing monthly mortgage insurance costs.

Therefore, paying mortgage insurance upfront can be a good option for those who have the financial means to afford the large upfront payment and plan to stay in the home long enough to recoup the cost of the premium.

Hit-and-Run Reports: Insurance Claims or Actual Accidents?

You may want to see also

Explore related products

![]()

Cancelling mortgage insurance

Mortgage insurance is a type of insurance that lenders require borrowers to buy when they take out a conventional loan with a down payment of less than 20% of the purchase price. This insurance protects the lender in the event that the borrower stops making payments on their loan. Private mortgage insurance (PMI) is one type of mortgage insurance that borrowers might be required to buy.

If you have a conventional loan with PMI, there are several ways to cancel your mortgage insurance. One way is to wait for your lender or servicer to automatically terminate it once your principal balance reaches 78% of the original value of your home. For a 30-year loan, this midpoint is typically reached after 15 years. Alternatively, if your home's value increases due to appreciation or renovations, you may be eligible to request a PMI cancellation by paying for a home appraisal to verify the new market value. You can also submit a written request to your mortgage servicer to cancel your PMI if your loan-to-original-value (LTOV) ratio falls below 80%.

If you have a Federal Housing Administration (FHA) loan, you pay a mortgage insurance premium (MIP) instead of PMI. With an FHA loan, you will typically pay MIP for either 11 years or the entire length of the loan, depending on the terms. One way to get rid of MIP is to refinance to a conventional loan.

It is important to note that cancelling your mortgage insurance will reduce your monthly costs. However, before making any decisions, it is recommended to consult with a mortgage loan officer or seek advice from a HUD-approved housing counseling agency to discuss your specific situation and explore the best options available to you.

Verizon Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

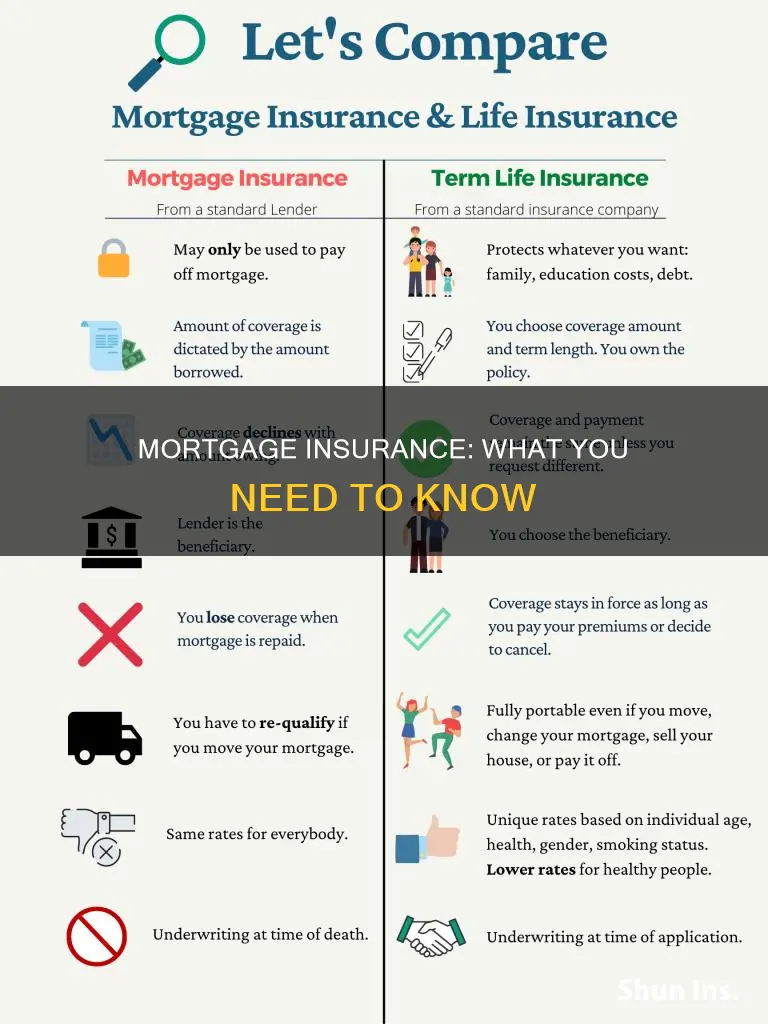

Mortgage insurance vs. mortgage life insurance

Mortgage insurance, also known as private mortgage insurance (PMI), is a type of insurance that borrowers are typically required to purchase when taking out a conventional loan with a down payment of less than 20% of the purchase price. It protects the lender against potential losses if the borrower is unable to repay the loan. While it can help borrowers qualify for a loan they may not otherwise be eligible for, it increases the cost of the loan and does not protect the borrower, who can still lose their home through foreclosure if they fall behind on payments.

Mortgage life insurance, on the other hand, is a type of life insurance policy that is designed to pay off the remaining balance of a mortgage in the event of the borrower's death. It is often referred to as "mortgage protection insurance" or "mortgage protection life insurance". The payout from mortgage life insurance goes directly to the lender to pay off the mortgage debt, ensuring that the borrower's loved ones can keep the house. However, this lack of flexibility means that the borrower's family will not have the freedom to spend the money as they see fit. Additionally, the payout from mortgage life insurance decreases over time as the mortgage balance is paid off, whereas the payout from a life insurance policy remains the same regardless of when a valid claim is made during the policy term.

Another key difference between mortgage insurance and mortgage life insurance lies in who they protect. Mortgage insurance protects the lender, not the borrower, in the event that the borrower falls behind on their payments. In contrast, mortgage life insurance protects the borrower's loved ones by ensuring that the mortgage is paid off in the event of their death.

When deciding between mortgage insurance and mortgage life insurance, it is important to consider your financial goals, health, and ability to qualify for coverage. Mortgage life insurance may be a good option for those who cannot medically qualify for other life insurance policies, as it typically does not require a medical exam. However, for those who are in good health and qualify for competitively priced term or permanent life insurance, a life insurance policy may offer more flexibility and broader coverage.

It is worth noting that there are alternative options to mortgage insurance for borrowers who make a low down payment. For example, borrowers can consider an FHA loan, which does not require private mortgage insurance but instead includes mortgage insurance premiums paid to the Federal Housing Administration (FHA). Additionally, VA-backed loans, which are intended to help servicemembers, veterans, and their families, do not require a monthly mortgage insurance premium, although there is an upfront "funding fee" that can be rolled into the mortgage.

Home Insurance Legal Protection

You may want to see also

Frequently asked questions

Mortgage insurance is a type of insurance that compensates the lender in the event that the borrower defaults on the mortgage. It is usually required for loans with a down payment of less than 20% of the purchase price of the home.

Private mortgage insurance (PMI) is a type of mortgage insurance that is provided by private insurance companies. It is required for conventional loans with a down payment of less than 20%. PMI rates vary by down payment amount and credit score but are generally cheaper than FHA rates for borrowers with good credit.

FHA mortgage insurance is required for all Federal Housing Administration (FHA) loans. It costs the same regardless of credit score, with a slight increase for down payments of less than 5%. The upfront premium is 1.75% of the loan amount, and there is also an annual premium of 0.15% to 0.75%.

Yes, under certain circumstances, you can cancel your mortgage insurance. For conventional loans, you can cancel PMI once you have paid off 20% of the loan's value or after the loan is 15 years old. For FHA loans, you may be able to cancel MIP if you have paid off at least 78% of the loan-to-value amount, but this depends on the origination date of the loan.