FHA loans are insured by the Federal Housing Administration (FHA). Borrowers who take out an FHA loan must pay FHA mortgage insurance premiums (MIP), which protect the lender if the borrower defaults. The FHA MIP includes an upfront premium, typically paid at closing, and annual premiums. The cost of the annual premiums depends on the loan amount, the size of the down payment, and the loan term. FHA mortgage insurance premiums are additional fees that all FHA loan borrowers pay, upfront and over the mortgage term.

| Characteristics | Values |

|---|---|

| FHA loan insurance | FHA MIP (Mortgage Insurance Premium) |

| Who pays? | All FHA loan borrowers |

| What does it protect against? | Default by the borrower |

| Who does it protect? | The lender |

| Who insures the loan? | Federal Housing Administration (FHA) |

| What happens if the borrower defaults? | FHA compensates the lender for the outstanding balance |

| Where do FHA MIP payments go? | Mutual Mortgage Insurance Fund (MMIF) |

| What is the upfront MIP payment? | 1.75% of the loan amount |

| When is the upfront MIP payment due? | At closing or can be added to the loan balance |

| Are there additional payments? | Yes, annual MIP payments |

| How are annual MIP payments calculated? | Based on loan amount, size, term, and loan-to-value (LTV) ratio |

| Can FHA mortgage insurance be avoided or mitigated? | Yes, through down payment assistance, obtaining a different type of mortgage, or refinancing |

| Is FHA mortgage insurance tax-deductible? | No |

Explore related products

What You'll Learn

![]()

FHA mortgage insurance premiums (MIP)

FHA mortgage insurance, also known as MIP (mortgage insurance premium), is mandatory for FHA loans and serves to protect lenders against losses resulting from borrower default. The insurance covers FHA-approved lenders and FHA loans for single-family homes, multifamily properties, manufactured homes, condos, and co-ops. There are two types of FHA loan insurance: the upfront mortgage insurance premium (UFMIP) and the annual mortgage insurance premium (MIP).

The UFMIP is a one-time charge, typically paid at closing, and is equivalent to 1.75% of the loan amount. It can be financed into the mortgage or paid in cash in full (partial cash payments are not allowed). If you refinance or sell your home within the first three years of the loan term, a partial refund of the UFMIP may be possible, depending on when the transaction occurs during this period.

The annual MIP, on the other hand, is charged annually and then divided by 12 to be included in your monthly mortgage payments. The cost of the annual MIP ranges from 15 to 75 basis points (0.15% to 0.75% of the loan amount). The specific rate depends on factors such as the loan term, loan amount, loan purpose, and LTV (loan-to-value) ratio. Borrowers with a higher LTV ratio will generally pay a higher MIP.

It's important to note that FHA mortgage insurance rates can increase, but your original MIP rate will not be affected as long as you stick with your original FHA loan. To remove MIP payments, you would need to refinance into a conventional loan once you have sufficient equity. An alternative option is an FHA Streamline Refinance, which could lower your overall mortgage payment, but it will not eliminate MIP entirely.

Insuring Your Home: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

MIP payment methods

Mortgage insurance premium (MIP) is a type of mortgage insurance required for homeowners who take out loans backed by the Federal Housing Administration (FHA). FHA-backed lenders use MIPs to protect themselves against higher-risk borrowers who are more likely to default on loans. FHA mortgages require every borrower to have mortgage insurance.

Upfront Mortgage Insurance Premium (UFMIP): This is a one-time payment made at the beginning of the loan. For FHA loans, the upfront MIP is typically 1.75% of the total loan amount. Borrowers can choose to pay this amount in cash at closing or roll it into their loan.

Monthly MIP Payments: Some FHA loans may require borrowers to make monthly MIP payments, which are typically included in the borrower's monthly mortgage payment. The amount of the monthly MIP depends on factors such as the base loan amount, loan-to-value (LTV) ratio, and the duration of the mortgage term.

Annual MIP Payments: Certain mortgages, including some FHA loans, may require an annual MIP payment. This is typically calculated as a percentage of the loan amount, similar to the upfront MIP, but the specific percentage can vary.

It is important to note that the specific MIP payment methods and requirements can vary depending on the loan's origination date, the borrower's credit score, and other factors. Additionally, MIP policies and guidelines may change over time, so it is always advisable to consult with a qualified lender or financial advisor for the most up-to-date information.

Furthermore, borrowers should be aware that MIP is typically required for the life of the loan unless certain conditions are met. For FHA loans originated between December 31, 2000, and June 3, 2013, the borrower may request the lender to cancel the MIP once they have paid off at least 78% of the loan-to-value amount. For loans originated after June 3, 2013, if the borrower made a down payment of less than 10%, they must pay MIP for the entire duration of the loan.

Mortgage Insurance: When Does It End?

You may want to see also

Explore related products

![]()

MIP cost calculation

When taking out an FHA loan, you will need to pay a mortgage insurance premium (MIP) in addition to your mortgage payments. The MIP is an insurance policy that protects your mortgage lender in case you default on your loan. It is beneficial to homebuyers as it relieves the burden of having to pay a large down payment that lenders usually require in the absence of insurance.

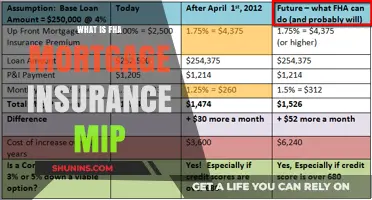

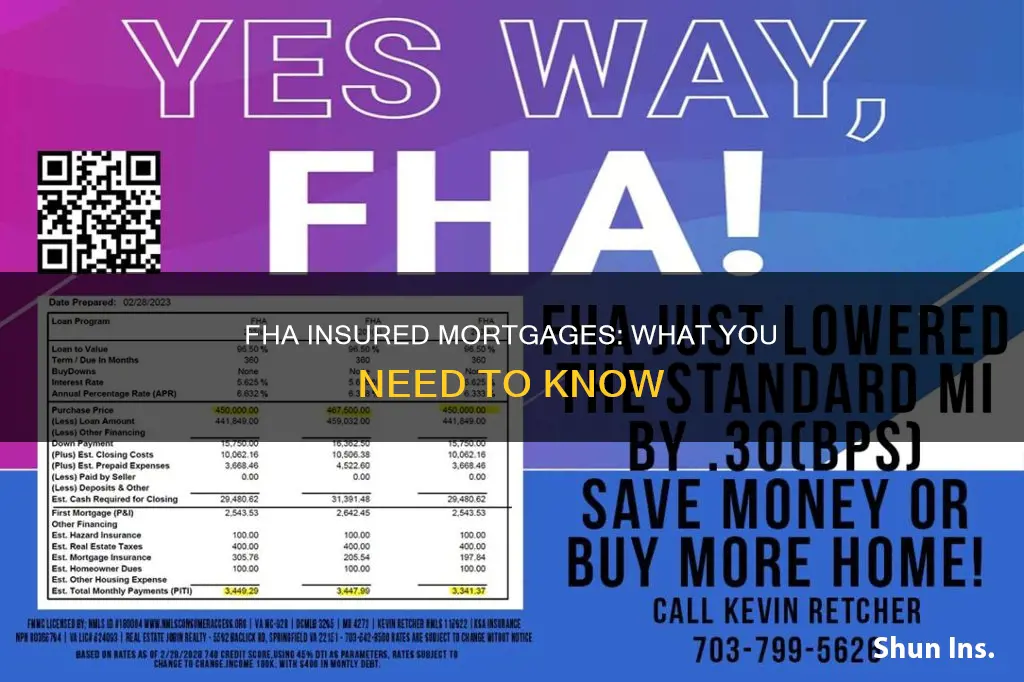

The MIP cost calculation for an FHA loan involves two payments: an upfront premium and an additional annual payment. The amount you pay for both depends on your loan amount. The upfront MIP payment is typically 1.75% of the total value of your loan. For example, if you borrow $150,000 for your mortgage, your upfront payment will be $2,500. This payment is due when you close on your FHA loan, or it can be added to the balance of the loan. You will only need to make this upfront payment once, unless you refinance or take on another FHA loan in the future.

The annual MIP payment depends on the loan term and the loan amount. If your loan term is 15 years or less and your loan amount is $726,200 or less, you will pay a certain amount in annual MIP. However, if your loan amount is greater than or equal to $726,200 and the loan term is less than 15 years, the annual MIP will be higher.

You can use an FHA Mortgage Calculator to estimate your total mortgage costs, including MIP charges, over any time frame. This calculator takes into account factors such as the loan amount, loan term, and down payment to provide an accurate estimate of your total costs. It is important to note that FHA MIP policies differ from private mortgage insurance (PMI) policies, as FHA uses an amortized premium, meaning insurance costs change along with your loan amount.

Down Payments: Reducing Mortgage Insurance Costs

You may want to see also

Explore related products

![]()

MIP refunds

When taking out a Federal Housing Administration (FHA) loan, borrowers are required to pay two types of mortgage insurance premiums: an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP). The upfront fee is equal to 1.75% of the loan amount, while the annual fee is typically 0.85% of the loan amount, divided into 12 monthly instalments.

If you refinance your FHA loan into another FHA loan, you may be eligible for a partial refund of your upfront mortgage insurance premium. The refund amount depends on how long you wait to refinance. If you refinance within 12 months, you will receive a refund of 58% of your upfront payment. If you wait until 3 years, the refund drops to 10%. After 36 months, you are no longer eligible for a refund. It's important to note that the refund is not given as a cash payment. Instead, it is applied directly to reduce the upfront MIP payment on your new FHA loan.

To calculate your refund amount, you can use the following formula: take your original MIP amount and multiply it by your refund percentage. For example, if your original MIP amount was $3,500 and you are eligible for a 50% refund, your refund would be $1,750. This amount would then be subtracted from the upfront MIP on your new FHA loan, reducing the amount you need to pay.

To qualify for an MIP refund, you must meet certain requirements. Your FHA loan must have been closed less than 3 years ago, and you must be current on your mortgage payments with no foreclosures listed on your credit report. Additionally, you can only receive a refund if you refinance into another FHA loan. The lender will handle the refund process, and you can contact the HUD Mortgage Insurance Premium Refund Support Service Center for more information.

HomeAway Insurance: Is Damage Coverage Worth the Cost?

You may want to see also

Explore related products

![]()

MIP alternatives

FHA mortgage insurance, also known as MIP (mortgage insurance premium), is mandatory for all Federal Housing Administration (FHA) loans. It protects lenders against borrower default. MIP includes an upfront premium of 1.75% of the loan amount, paid when the loan is closed, and additional annual payments. The annual MIP varies based on the size, term and loan-to-value (LTV) ratio of the loan, typically costing between 0.15% and 0.75% of the loan amount.

While MIP is a requirement of FHA loans, there are alternative options for borrowers who want to avoid paying it. Here are some MIP alternatives:

Conventional Loans and PMI

One alternative to FHA loans is to take out a conventional loan. Unlike FHA loans, conventional loans do not always require mortgage insurance. If you put down a 20% or more down payment on a conventional loan, you will not need to pay for private mortgage insurance (PMI). PMI is a type of mortgage insurance that applies to conventional loans when the borrower makes a down payment of less than 20%. However, if you initially take out a conventional loan with PMI, you can request that your lender cancels the PMI payments once you reach 20% home equity.

USDA Loans

If you are an eligible service member or buying in a qualifying rural area, you may qualify for a USDA loan. USDA loans do not require a down payment or mortgage insurance, providing an alternative to FHA loans and their associated MIP.

Down Payment Assistance Programs

Another option to mitigate MIP costs is to utilise down payment assistance programs. By boosting your down payment to 10% through assistance programs, you can reduce the duration of MIP payments. With a 10% or larger down payment on an FHA loan, you will pay MIP for the first 11 years, instead of for the entire loan term.

Refinancing

If you are already committed to an FHA loan, refinancing into a conventional loan at a later stage may help you avoid MIP. Refinancing to a conventional loan with at least 20% home equity means you can escape the ongoing MIP payments associated with FHA loans. However, it is important to consider the costs and benefits of refinancing carefully, as it may not always be worth it solely for the purpose of reducing MIP.

Personal Mortgage Insurance: What You Need to Know

You may want to see also

Frequently asked questions

FHA loans are "insured" by the Federal Housing Administration (FHA). If a borrower defaults on the mortgage, the agency will compensate the lender for the outstanding balance.

An FHA MIP is an additional payment made to secure an FHA loan. It involves two payments: an upfront premium and an additional annual payment. The amount paid depends on the loan amount, the size of the down payment, and the loan term.

The upfront MIP payment is 1.75% of the loan amount, typically paid at closing. Annual premiums vary based on the size, term, and loan-to-value (LTV) ratio of the loan.

No, FHA mortgage insurance premiums are not tax-deductible.