Florida's auto insurance rates are among the highest in the country, with drivers paying more than twice the national average. The high rates are attributed to several factors, including Florida's no-fault auto insurance laws, a high proportion of uninsured drivers, increased risk of extreme weather conditions, and higher healthcare costs. In response to the escalating insurance costs, Florida lawmakers are considering repealing the state's no-fault system and implementing a responsibility-based system of bodily injury liability insurance. This change aims to reduce insurance rates by decreasing lawsuits and eliminating fraud.

| Characteristics | Values |

|---|---|

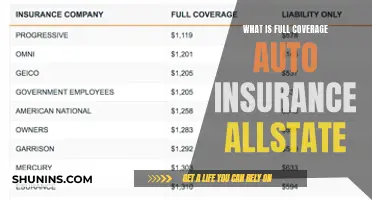

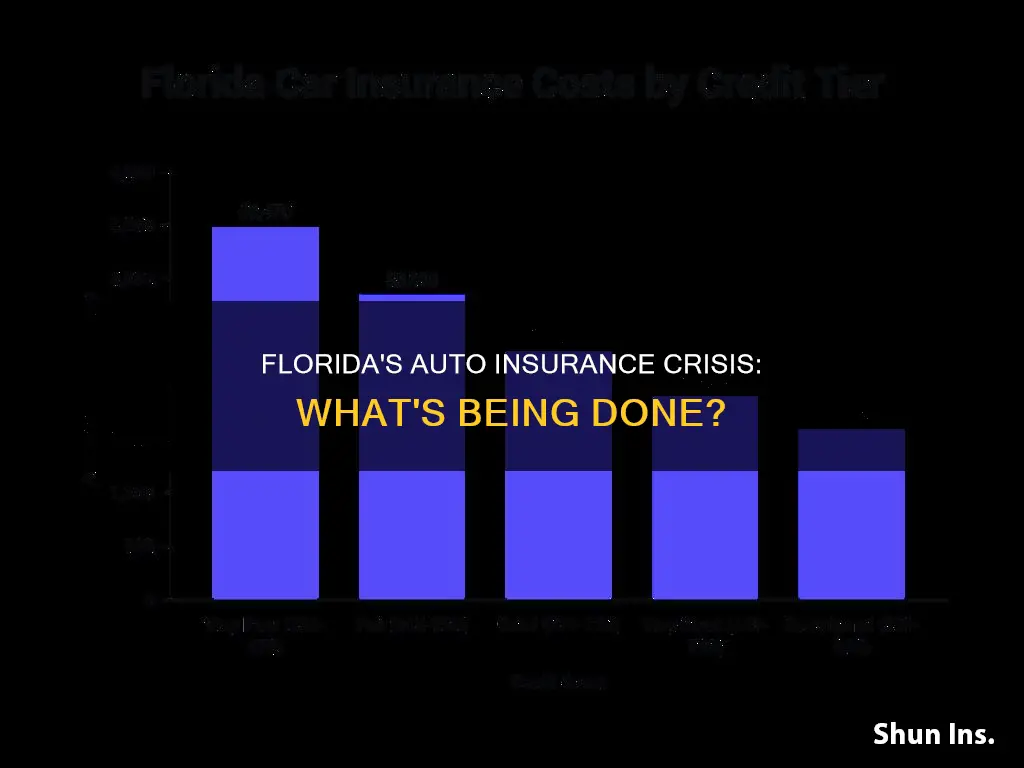

| Average annual cost of car insurance in Florida | $2,412, $2,208, $2,917, $3,183, $213, $216 |

| Average annual cost of car insurance in the US | $1,668, $2,118, $2,019, $2,160, $140 |

| Increase in insurance rates in Florida | 25%, 33.9% to 57.3%, 30.2%, 44.3%, 23.8%, 7% |

| Reasons for high insurance rates | High proportion of uninsured drivers, increased risk of hurricanes, higher auto theft rates, fraud, high healthcare costs, high-risk drivers, busy roads, additional insurance requirements |

| Insurance companies increasing rates | United Services Automobile Association (USAA), State Farm Mutual Automobile Insurance Co., Progressive, Liberty Mutual, Geico General Insurance Co., Auto Club South (AAA) |

Explore related products

What You'll Learn

![]()

Florida's high rate of uninsured drivers

Florida has the highest rate of uninsured drivers in the US, with about 26.7% of drivers lacking insurance coverage. This is significantly higher than the national average of 13%, which equates to around 32 million uninsured drivers on US roads.

The high rate of uninsured drivers in Florida is one of the reasons that the state's auto insurance rates are so high. Florida's auto insurance rates are the fourth-highest in the US, with an average cost of $2,208 per year. This is an increase of 25% from 2015 to 2021.

The high cost of insurance in Florida is due to several factors, including the state's no-fault auto insurance laws, high healthcare costs, and the risk of severe weather events such as hurricanes and tornadoes. Florida also has a high rate of auto theft and claims fraud, which contribute to the high insurance costs.

The consequences of driving without insurance in Florida include fines and license suspension, but this does little to help victims of accidents caused by uninsured drivers. While victims can sue the uninsured driver, it is often discovered that these drivers have limited financial resources, making it not worth pursuing legal action.

To protect themselves from uninsured drivers, Floridians can purchase ""uninsured and underinsured motorist insurance" as additional coverage. This added expense protects drivers and their families in the event of a collision with an uninsured driver, covering injuries and property damage.

The issue of uninsured drivers is not unique to Florida, and nearly half of US states require drivers to have uninsured motorist coverage. While this added protection is beneficial to insured drivers, it also contributes to the overall cost of insurance in the state.

Auto Insurance: Wisconsin's Mandatory Law

You may want to see also

Explore related products

![]()

High auto theft rates

Florida's high auto insurance rates are influenced by various factors, including the state's no-fault auto insurance laws, extreme weather conditions, high healthcare costs, and a significant number of uninsured drivers. However, one significant factor contributing to the high insurance rates in Florida is the state's high auto theft rates.

Florida has the fourth-highest vehicle theft rate in the nation. In 2022, thieves stole 45,973 vehicles from Floridians, a 6% increase from 2021. The state's overall theft rate is slightly lower than the national average, with 18.43 thefts per 1,000 residents. However, certain areas within Florida have much higher theft rates. For instance, the northwest neighbourhoods have a theft rate of 1 in 26, while the east part of the state is considered safer, with a rate of 1 in 184.

The high auto theft rate in Florida is influenced by several factors. One reason is the state's high population density and tourist attractions, which provide more opportunities for thieves. Florida is the third-busiest state in the country, with 79.8 million visitors in 2020. The high traffic density increases the likelihood of car theft. Additionally, Florida's position as a hurricane-prone state may contribute to auto theft, as natural disasters can cause chaos and provide opportunities for criminal activity.

The types of vehicles driven in Florida may also be a factor in auto theft rates. Certain Kia and Hyundai models that lack engine immobilizers are especially vulnerable to theft. Older vehicles, such as the 2004 Toyota Camry and the 2012 Toyota Rav 4, are also targeted by thieves, as seen in the experiences of Ana Curbelo and Lewis Breland, respectively.

To combat auto theft, Florida residents are encouraged to take preventive measures. These include practising good security hygiene, such as locking doors and keeping keys secure, and installing anti-theft devices. Additionally, parking in well-lit areas or garages and considering motion sensor security lights can deter thieves. Keeping auto policies up to date and promptly reporting vehicle theft to law enforcement and insurers are also crucial steps in mitigating the impact of auto theft.

Camper Coverage Quandary: Does Auto Insurance Protect Against Water Damage?

You may want to see also

Explore related products

![]()

High number of uninsured drivers

Florida has a high number of uninsured drivers, which is a significant factor contributing to the state's high auto insurance rates. As of 2024, Florida's auto insurance rates are above the national average, with an annual cost of $2,412 compared to the national average of $1,668. The high proportion of uninsured drivers in Florida drives up the cost of insurance for all drivers in the state.

The Insurance Information Institute (Triple-I) estimates that, as per year-end 2022 data, approximately 15.9% of Florida drivers do not have insurance, which is higher than the national average of 14%. However, the Insurance Research Council (IRC) provides a higher estimate, suggesting that the number of uninsured drivers in Florida could be as high as 20.4%. This is a significant increase from the national average in 2019, which was 12.6%.

The high cost of car insurance in Florida is a major reason for the high number of uninsured drivers. Florida's insurance rates are among the most expensive in the country, with minimum-liability coverage costing up to $115 per month and full coverage costing up to $270 per month. In comparison, the national average for minimum coverage is $52 per month. The high insurance rates in Florida have led to a situation where many drivers are unable to afford coverage, despite it being a legal requirement.

The consequences of a high number of uninsured drivers are significant. Firstly, it increases the financial burden on insured drivers, as they have to bear the cost of accidents involving uninsured drivers. Additionally, uninsured motorists are more likely to be reckless on the road, making the roads less safe for everyone. Florida has a high rate of vehicle accidents and fatalities, with the third-highest vehicle accident fatality rate in the US in 2023, amounting to 3,278 deaths.

To address the issue of uninsured drivers, Florida has implemented various measures. The state has compulsory auto insurance laws, requiring drivers to carry a minimum of $10,000 in personal injury protection and $10,000 in property damage liability insurance. However, Florida is a no-fault state, which means that each driver's insurance covers their medical expenses and those of their passengers, regardless of who is at fault in an accident. This no-fault system may contribute to higher insurance rates, as it increases the potential costs for insurance companies.

In conclusion, the high number of uninsured drivers in Florida is a significant factor in the state's high auto insurance rates. The high cost of insurance has led to an increase in uninsured drivers, creating a cycle that further drives up insurance costs. This has resulted in safety concerns and financial burdens for insured drivers. Florida's efforts to mandate auto insurance have not been fully effective, and the state continues to struggle with the challenge of reducing the number of uninsured motorists.

Auto Insurance: Age Discrimination?

You may want to see also

Explore related products

$15.95 $15.95

![]()

Extreme weather conditions

Florida's unpredictable weather poses significant risks that can affect auto insurance premiums. The state is susceptible to hurricanes, storms, flooding, and hail, which can cause extensive vehicle damage. During hurricane season, from June 1 to November 30, strong winds, heavy rain, and flooding can impact cars and homes.

The risk of hurricane and storm damage is a notable concern in Florida. Natural disasters can lead to vehicle damage from falling trees, debris, flooding, or high winds. When claims increase due to these weather events, insurance companies often raise their rates to cover the heightened risk. Flooding, a frequent occurrence during hurricane season, can cause severe vehicle damage, making comprehensive coverage more expensive in Florida.

Severe weather conditions can also increase the likelihood of accidents. Heavy rain can reduce visibility and make roads slippery, leading to more collisions and insurance claims, potentially resulting in higher insurance premiums. After extreme weather events, the demand for auto repairs and replacements typically rises, driving up the cost of parts and labor. Insurance companies may adjust their rates to reflect these higher costs.

Given the weather risks in Florida, many car owners opt for comprehensive coverage, which protects against damage caused by events other than collisions, such as storms or flooding. The increased demand for comprehensive coverage can influence the overall cost of auto insurance in the state.

The impact of extreme weather on auto insurance rates in Florida is significant. The state's unpredictable weather, including hurricanes and floods, can lead to higher insurance premiums due to increased claims and repair costs. These weather events can also increase accident rates, further impacting insurance costs. Florida's weather risks are essential considerations for residents when protecting their vehicles and managing their insurance expenses.

Insurance Claims: Deceased Vehicles

You may want to see also

Explore related products

![]()

High healthcare costs

Florida's high auto insurance rates are influenced by several factors, including high healthcare costs, which are a significant contributor to the overall expense. The state's residents already face higher-than-average healthcare expenses, and these costs are reflected in auto insurance premiums.

The United States spends approximately $3 trillion on healthcare annually, and Florida residents bear a more substantial burden than most. According to the Commonwealth Fund, Florida is one of only five states where residents spend 14% or more of their income on healthcare. This is significantly higher than the national average, and insurance companies pass on these costs to consumers in the form of higher premiums.

When accidents occur, insurance providers utilise premiums to cover medical expenses for injured drivers and passengers. In "tort states", the premiums also cover treatments for the other party. As a no-fault state, Florida's insurance requirements further complicate matters. Florida mandates a minimum of $10,000 in personal injury protection (PIP) coverage, ensuring that each driver's insurance covers their own expenses regardless of who is at fault. This additional requirement further increases the cost of auto insurance in the state.

The high healthcare costs in Florida are not limited to auto insurance but also impact other forms of insurance, such as health insurance. The average monthly cost of a Silver health plan in Florida, a popular choice for consumers, is $613 without discounts. This is significantly higher than the national average.

The high healthcare costs in Florida are driven by various factors, including the state's large elderly population, the prevalence of severe and chronic health conditions, and the cost of living. These factors contribute to higher insurance premiums, making it challenging for residents to afford comprehensive coverage.

To address these challenges, Florida residents can explore various options to reduce their insurance costs. Shopping around for quotes, bundling policies, taking advantage of discounts, and adjusting their coverage levels can help lower premiums. Additionally, enrolling in telematics programs or usage-based insurance can offer safer drivers discounted rates. However, it is essential to carefully consider the potential risks and costs associated with reducing coverage levels.

Disputing Auto Insurance Claims: Can It Be Done?

You may want to see also

Frequently asked questions

There are several reasons for high auto insurance rates in Florida, including the state's no-fault auto insurance laws, high healthcare costs, high traffic density, severe weather risks, and the number of uninsured drivers.

Auto insurance rates in Florida are expected to rise in 2024, but not as steeply as in previous years. In 2023, auto insurance rates in the state surged by 24%.

The average annual cost of car insurance in Florida is around $2,400, which is significantly higher than the national average of $1,668.

To combat high insurance rates, lawmakers in Florida have proposed repealing the state's no-fault auto insurance system and requiring drivers to carry bodily injury liability insurance. This is expected to reduce insurance rates by minimizing lawsuits and eliminating fraud.