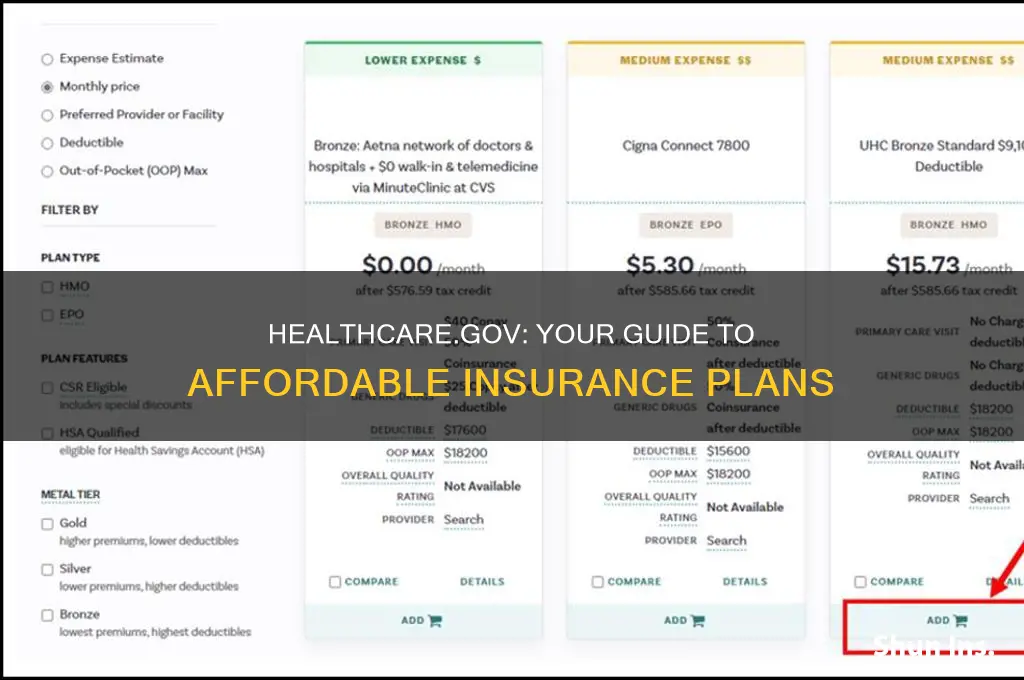

The Health Insurance Marketplace, also known as the ACA or Obamacare, is a federally operated insurance marketplace where individuals and families can purchase and compare health plans. The Marketplace is primarily accessed at www.healthcare.gov or by telephone. The website functions as a clearing house, allowing Americans to compare prices on health insurance plans in their states, to begin enrollment in a chosen plan, and to simultaneously find out if they qualify for government healthcare subsidies. The Health Insurance Marketplace is for people who don't have health insurance and is not required for those with Medicare.

| Characteristics | Values |

|---|---|

| Purpose | To help people who don't have health insurance to find and purchase insurance |

| Users | Individuals and families |

| Requirements | Must be a U.S. citizen or national (or be lawfully present) |

| Website | www.healthcare.gov |

| Contact | 800-318-2596 |

| Eligibility | Income between 100% and 400% of the federal poverty level |

| Benefits | No limit on coverage for essential health benefits; no refusal of coverage based on sex or pre-existing conditions |

| Enrollment | Annual open enrollment period |

| Dental Coverage | Available |

| Small Business Program | SHOP Marketplace |

| Tax Provisions | Premium Tax Credit |

Explore related products

What You'll Learn

- How to get insurance through the ACA Health Insurance Marketplace?

- The Health Insurance Marketplace is for people without insurance

- The Health Insurance Marketplace is a federally operated insurance marketplace

- The Health Insurance Marketplace offers subsidies to those who earn between one and four times the federal poverty line

- The Health Insurance Marketplace is also open to non-profit organisations

![]()

How to get insurance through the ACA Health Insurance Marketplace

The Affordable Care Act (ACA), also known as Obamacare, gives more people access to health insurance. The ACA's Health Insurance Marketplace provides affordable health insurance options, with no income limit. To be eligible to enroll, you must be a U.S. citizen or national, or be lawfully present.

To get started, go to Healthcare.gov to find your state Health Insurance Marketplace. Each state's Marketplace has its own enrollment instructions. During the Marketplace open enrollment period each year, you can review health care coverage options and purchase insurance. You can also learn about dental and vision coverage, as well as preventive services and essential health benefits.

If you experience a significant life event, such as moving or having a baby, you may be able to change your coverage during a special enrollment period. Additionally, reporting changes in your circumstances, such as household income or family size, may make you eligible for a special enrollment period outside of the open enrollment window.

For small businesses, the Small Business Health Options Program Marketplace (SHOP) helps provide health coverage to employees. SHOP is typically available to businesses with 50 or fewer full-time equivalent employees, but some states may offer it to businesses with up to 100 employees. Businesses can offer health and dental coverage that meets their specific needs and can enroll in SHOP at any time of the year.

Life Insurance: Dearborn Police's Entitlement and Benefits

You may want to see also

Explore related products

![]()

The Health Insurance Marketplace is for people without insurance

The Health Insurance Marketplace is an online resource for people without insurance to find and purchase affordable health insurance options. It is provided by the Affordable Care Act (ACA), also known as Obamacare, which gives more people access to health insurance. The Health Insurance Marketplace is accessible via HealthCare.gov, where users can review health care coverage options and purchase insurance.

The Health Insurance Marketplace is not just for individuals, but also for small businesses to provide health coverage to their employees. This is known as the Small Business Health Options Program Marketplace, or SHOP. SHOP was previously only available to employers with 50 or fewer full-time equivalent employees, but since 2016, some states have made it available to businesses with up to 100 employees.

There is no income limit to be eligible to enroll in health coverage through the Marketplace. However, to be eligible, you must be a U.S. citizen or national, or be lawfully present, and have a qualifying immigration status. The ACA also provides special patient protections for those insured through the Health Insurance Marketplace. For example, insurers cannot refuse coverage based on sex or a pre-existing condition, and there are no lifetime or annual limits on coverage for essential health benefits.

The Health Insurance Marketplace has an open enrollment period each year, as well as special enrollment periods for eligible taxpayers. It is important to report any changes in circumstances, such as household income or family size, as they happen, as this may affect your eligibility and advance payments of the premium tax credit.

Life Insurance Annuity: Taxable Proceeds?

You may want to see also

Explore related products

$11.1 $16.99

![]()

The Health Insurance Marketplace is a federally operated insurance marketplace

The Health Insurance Marketplace, also known as the ACA or Obamacare, is a federally operated insurance marketplace. It provides individuals and families with access to affordable health insurance options and helps small businesses provide health coverage to their employees. The Marketplace is facilitated by HealthCare.gov, where individuals can review and purchase insurance plans, and find information about eligibility, enrollment, and coverage.

The Health Insurance Marketplace offers a range of plans that include preventive services, essential health benefits, and dental coverage. It also provides special protection for certain groups, such as Deferred Action for Childhood Arrivals (DACA) recipients, ensuring nondiscrimination in health programs. The Marketplace is accessible to US citizens or nationals and those lawfully present, with no income limit.

One of the key advantages of the Health Insurance Marketplace is its flexibility. It allows individuals to enroll during open enrollment periods and offers special enrollment periods for eligible taxpayers who experience changes in circumstances, such as modifications in household income or family size. These changes may impact their advance payments of the premium tax credit, making it crucial to report them promptly.

Additionally, the Health Insurance Marketplace provides tax benefits. Individuals who purchase coverage through the Marketplace may receive advance payments of the premium tax credit, which can help reduce the cost of their health insurance. To reconcile these payments, taxpayers must file a tax return and complete Form 1095-A, the Health Insurance Marketplace Statement. This form details the total monthly health insurance premiums paid and any premium assistance received.

The Health Insurance Marketplace, as a federally operated insurance marketplace, plays a vital role in expanding access to healthcare for Americans. By offering a range of affordable health insurance options and providing special protections for certain groups, it helps ensure that individuals and families can obtain the coverage they need.

Canceling USAA Life Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

The Health Insurance Marketplace offers subsidies to those who earn between one and four times the federal poverty line

The Health Insurance Marketplace, also known as Obamacare or the Affordable Care Act (ACA), offers affordable health insurance options to US citizens or nationals. The ACA provides special patient protection, ensuring that insurers cannot refuse coverage based on gender or pre-existing conditions. There are no lifetime or annual limits on coverage for essential health benefits.

The ACA offers two types of subsidies to help individuals and families pay for health coverage: the premium tax credit and the cost-sharing subsidy. The premium tax credit helps lower monthly premium expenses, while the cost-sharing subsidy reduces deductibles and other cost-sharing amounts. These subsidies are available to those with incomes between one and four times the federal poverty level. The federal poverty level varies based on family size and location, with the 2025 poverty level set at $15,060 for a single adult and $31,200 for a family of four, with higher levels in Alaska and Hawaii.

Individuals and families with incomes between 100% and 400% of the federal poverty level may qualify for these subsidies. For example, a family of four with an income of $128,600 (four times the poverty level) would be eligible for some financial assistance. Those with incomes above this threshold would lose eligibility for subsidies and would need to pay the full price for their health plans.

The Health Insurance Marketplace provides an online calculator to help individuals and families estimate their potential savings and eligibility for subsidies. This calculator takes into account household income, including the income of the taxpayer, spouse, and, in some cases, children or dependents. By using this tool, individuals can make informed decisions about their health insurance options and choose a plan that best suits their needs and financial situation.

Hybrid Cars: More Expensive to Insure?

You may want to see also

Explore related products

![]()

The Health Insurance Marketplace is also open to non-profit organisations

The Health Insurance Marketplace, also known as Obamacare or the Affordable Care Act (ACA), is a platform that allows individuals, families, and small businesses to review healthcare coverage options and purchase insurance. It is facilitated by HealthCare.gov, which is an official US government website indicated by the "gov" domain. This platform enables users to securely share sensitive information, enrol in plans, and manage their accounts.

The ACA gives more people access to affordable health insurance, regardless of income level. To be eligible for enrolment, individuals must be US citizens or nationals or be lawfully present, with eligible immigration statuses. The ACA also provides special patient protection, preventing insurers from denying coverage based on sex or pre-existing conditions. There are no lifetime or annual limits on essential health benefits.

The Small Business Health Options Program (SHOP) Marketplace, part of the Health Insurance Marketplace, assists small businesses in providing health and dental coverage to their employees. SHOP is available to small businesses with up to 50 full-time equivalent employees, and some states may extend this to businesses with up to 100 employees. Notably, the SHOP Marketplace is also open to non-profit organisations, enabling them to offer health and dental coverage that aligns with their needs and the needs of their employees. Non-profit organisations with 1 to 50 employees can generally qualify for SHOP insurance, and they can choose to offer insurance through SHOP or alternative sources.

SHOP offers flexibility and choice, allowing organisations to offer a single plan to their employees or providing employees with multiple plan options. Additionally, SHOP enrolment is not restricted to a specific period, meaning organisations can offer SHOP coverage to their employees at any time of the year. SHOP also provides online tools, calculators, fact sheets, guides, and other resources to support employers in making informed decisions about their coverage options.

Chronic Conditions: Overlooked for Life Insurance?

You may want to see also

Frequently asked questions

The Health Insurance Marketplace is a federal health insurance program for people who don't already have health insurance.

To be eligible for the Health Insurance Marketplace, you must live in the United States, be a U.S. citizen or national (or be lawfully present), and not be incarcerated.

The Open Enrollment Period for the Health Insurance Marketplace is from November 1 to January 15.

You can enroll in a plan through the Health Insurance Marketplace by visiting the Marketplace website at HealthCare.gov and reviewing the available health care coverage options.

Enrolling in a plan through the Health Insurance Marketplace can provide financial benefits, such as tax credits and cost-sharing reductions, as well as access to regular health care services, including preventive care.