HMO POS (Health Maintenance Organization Point of Service) insurance is a hybrid health plan that combines elements of both HMO and PPO (Preferred Provider Organization) models, offering policyholders a structured yet flexible approach to healthcare. In this plan, members typically select a primary care physician (PCP) who coordinates their care and provides referrals to specialists within the HMO network. While most services require staying within the network to maximize coverage, the POS feature allows members to seek care outside the network for an additional cost, providing greater flexibility compared to traditional HMOs. This blend of managed care and out-of-network options makes HMO POS plans appealing to those seeking both cost control and the freedom to access a broader range of providers when needed.

| Characteristics | Values |

|---|---|

| Type of Plan | Hybrid of Health Maintenance Organization (HMO) and Point of Service (POS) |

| Primary Care Physician | Required; acts as a gatekeeper for specialist referrals |

| Network Restrictions | In-network providers only, except in emergencies or with referrals |

| Referrals | Needed for specialist visits, but out-of-network care allowed with referral |

| Out-of-Network Coverage | Limited; typically only with a referral or in emergencies |

| Cost Structure | Lower premiums and out-of-pocket costs compared to PPO plans |

| Deductibles | Typically lower or none for in-network services |

| Copayments/Coinsurance | Fixed copays for in-network services; higher costs for out-of-network care |

| Preventive Care | Often covered at 100% without copay or deductible |

| Flexibility | Less flexible than PPO but more than traditional HMO |

| Best For | Individuals who want lower costs and are comfortable with a primary care physician managing their care |

| Provider Choice | Limited to network providers, except with referrals |

| Emergency Care | Covered both in-network and out-of-network |

| Prescription Coverage | Typically included, with lower costs for in-network pharmacies |

| Annual Limits | No annual or lifetime limits on essential health benefits |

| Preventive Services | Fully covered under the Affordable Care Act (ACA) |

Explore related products

What You'll Learn

![]()

HMO vs. POS Comparison

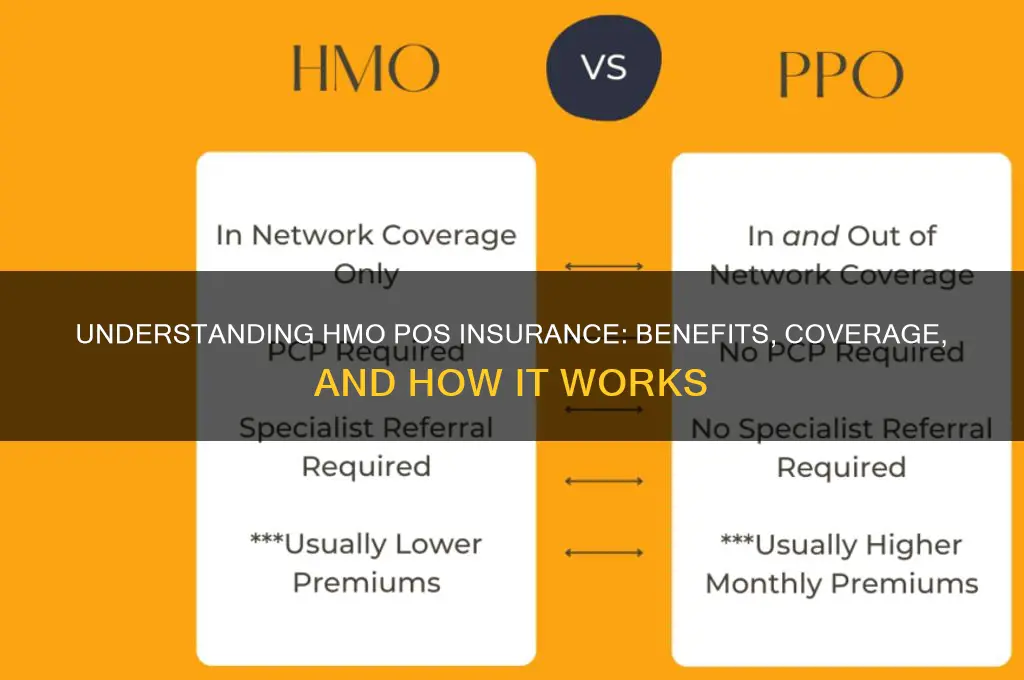

When comparing HMO (Health Maintenance Organization) and POS (Point of Service) health insurance plans, it’s essential to understand their core differences in structure, flexibility, and cost. Both plans fall under managed care but operate differently in terms of provider networks, referrals, and out-of-network coverage.

Network Restrictions and Primary Care Physicians (PCPs): In an HMO, members are required to choose a primary care physician (PCP) who acts as a gatekeeper for all healthcare services. Specialists and other medical services must be coordinated through this PCP, and out-of-network care is typically not covered except in emergencies. This strict network structure helps keep costs low but limits flexibility. In contrast, a POS plan also requires a PCP but allows members to seek out-of-network care, though at a higher cost. While the PCP still coordinates care, the option to go outside the network provides more freedom, albeit with increased out-of-pocket expenses.

Referrals and Specialist Access: With an HMO, referrals from the PCP are mandatory for specialist visits. This ensures that care is managed and unnecessary visits are minimized, which helps control costs. However, it can be inconvenient for members who prefer direct access to specialists. A POS plan also requires referrals for in-network specialists but may allow direct access to out-of-network specialists, though this will likely result in higher costs. This hybrid approach offers a balance between managed care and flexibility.

Cost and Premiums: HMO plans generally have lower premiums and out-of-pocket costs compared to POS plans because of their restrictive network and referral requirements. The trade-off is limited choice and less coverage for out-of-network services. POS plans, while more expensive, provide greater flexibility and the option to access out-of-network providers, making them suitable for individuals who prioritize choice over cost.

Coverage for Out-of-Network Services: One of the most significant differences is how each plan handles out-of-network care. HMO plans rarely cover out-of-network services except in emergencies, making them ideal for those who are comfortable staying within a specific network. POS plans, however, offer coverage for out-of-network providers, though at a higher cost and often with higher deductibles or coinsurance. This makes POS plans a better fit for individuals who may need or prefer out-of-network care.

In summary, the choice between HMO and POS depends on your priorities. If cost efficiency and simplicity are important, an HMO may be the better option. However, if you value flexibility and the ability to access out-of-network care, a POS plan might align better with your needs. Understanding these differences ensures you select the plan that best fits your healthcare requirements and budget.

Understanding Insurance Coverage for Bone Density Scans

You may want to see also

Explore related products

![]()

In-Network vs. Out-of-Network Coverage

HMO POS (Health Maintenance Organization Point of Service) insurance plans combine elements of traditional HMO and PPO (Preferred Provider Organization) plans, offering a unique approach to healthcare coverage. One of the critical aspects policyholders must understand is the difference between In-Network vs. Out-of-Network Coverage, as it directly impacts costs and access to care. In an HMO POS plan, the insurer maintains a network of healthcare providers with whom they have negotiated rates. When you receive care from an in-network provider, the plan typically covers a larger portion of the costs, and you benefit from lower out-of-pocket expenses such as copays and coinsurance. This is because in-network providers have agreed to accept the plan’s negotiated rates, ensuring cost efficiency for both the insurer and the policyholder.

In contrast, out-of-network coverage in an HMO POS plan is more restrictive and costly. While some HMO POS plans allow you to seek care outside the network, doing so usually results in significantly higher out-of-pocket costs. Out-of-network providers have not agreed to the plan’s negotiated rates, so the insurer may cover only a small portion of the charges, leaving you responsible for the remainder. Additionally, you may need to pay the provider upfront and then seek reimbursement from the insurer, which can be a cumbersome process. It’s important to note that some HMO POS plans require a referral from your primary care physician (PCP) before seeing an out-of-network specialist, adding another layer of complexity.

The choice between in-network and out-of-network care often boils down to cost and convenience. In-network care is generally more affordable and streamlined, as the plan covers a larger share of the expenses, and you typically only pay a copay at the time of service. The network also ensures that providers are pre-vetted by the insurer, offering a level of quality assurance. On the other hand, out-of-network care may be necessary if you require a specialist or treatment not available within the network. However, this flexibility comes at a premium, with higher deductibles, coinsurance, and potential balance billing, where the provider charges more than the insurer reimburses.

Understanding the nuances of In-Network vs. Out-of-Network Coverage is essential for maximizing the benefits of an HMO POS plan. To make informed decisions, policyholders should review their plan’s provider directory to identify in-network options and understand the specific out-of-network rules, including any referral requirements. By prioritizing in-network care whenever possible, you can minimize costs and ensure smoother access to healthcare services. However, in situations where out-of-network care is unavoidable, being aware of the potential financial implications allows you to plan accordingly and avoid unexpected expenses.

In summary, the In-Network vs. Out-of-Network Coverage distinction in HMO POS insurance is a key factor in managing healthcare costs and access. While in-network care offers affordability and convenience, out-of-network care provides flexibility but at a higher cost. By carefully navigating these options and understanding your plan’s specifics, you can optimize your healthcare coverage and make the most of your HMO POS insurance.

Understanding Part C Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Primary Care Physician Role

In an HMO POS (Health Maintenance Organization Point of Service) insurance plan, the Primary Care Physician (PCP) role is central to the coordination and delivery of healthcare services. The PCP serves as the policyholder’s first point of contact for medical care, acting as a gatekeeper to ensure appropriate and efficient treatment. Unlike traditional HMOs, which strictly require all care to be managed through the PCP, HMO POS plans offer more flexibility by allowing members to seek out-of-network care, though typically at a higher cost. Despite this flexibility, the PCP remains a critical figure in guiding the patient’s healthcare journey. Their primary responsibility is to provide preventive care, diagnose and treat common illnesses, and manage chronic conditions. By maintaining a comprehensive understanding of the patient’s medical history, the PCP ensures continuity of care and helps avoid redundant or unnecessary treatments.

The Primary Care Physician role in an HMO POS plan also includes coordinating referrals to specialists when necessary. While the POS model allows members to self-refer to out-of-network providers, staying within the network through PCP referrals often results in lower out-of-pocket costs. The PCP evaluates the need for specialized care, selects an appropriate in-network specialist, and ensures that the specialist has all relevant patient information. This coordination is essential for maintaining the quality and efficiency of care, as it prevents fragmented treatment and ensures that all providers are aligned in their approach to the patient’s health. Additionally, the PCP monitors the outcomes of specialist visits and integrates any new information into the patient’s overall care plan.

Preventive care is another cornerstone of the Primary Care Physician role in HMO POS insurance. PCPs are responsible for conducting routine check-ups, screenings, and immunizations to identify potential health issues early. By focusing on prevention, they help reduce the likelihood of costly and complex medical problems down the line. This proactive approach aligns with the cost-effective nature of HMO POS plans, which emphasize managing healthcare expenses through early intervention. PCPs also educate patients on healthy lifestyle choices, disease prevention, and the importance of adhering to treatment plans, empowering them to take an active role in their health.

Effective communication is a key aspect of the Primary Care Physician role within the HMO POS framework. PCPs must clearly explain treatment options, insurance coverage details, and the implications of seeking out-of-network care. This transparency helps patients make informed decisions about their healthcare while maximizing the benefits of their insurance plan. Furthermore, PCPs act as advocates for their patients, ensuring that their needs are met within the constraints of the HMO POS structure. By fostering a strong patient-physician relationship, PCPs build trust and encourage patients to seek timely care, ultimately improving health outcomes.

Finally, the Primary Care Physician role in HMO POS insurance extends to managing administrative tasks related to the patient’s care. This includes documenting medical records, submitting claims, and ensuring compliance with insurance requirements. While these tasks are often handled with the support of administrative staff, the PCP remains accountable for the accuracy and completeness of the information. Efficient management of these responsibilities ensures that patients receive timely care and that providers are appropriately reimbursed. In this way, the PCP not only delivers clinical care but also plays a vital role in the operational success of the HMO POS model.

Voluntary Term Life Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Referral Requirements Explained

HMO POS (Health Maintenance Organization Point of Service) insurance plans combine elements of traditional HMO and PPO plans, offering a unique structure for managing healthcare services. One of the key features of HMO POS plans is the referral requirement, which plays a crucial role in how policyholders access specialized care. Understanding these referral requirements is essential for maximizing the benefits of this type of insurance while avoiding unexpected costs.

In an HMO POS plan, policyholders are typically required to choose a primary care physician (PCP) who serves as the first point of contact for all healthcare needs. This PCP is responsible for coordinating care and managing the patient’s overall health. When a policyholder needs to see a specialist, such as a dermatologist, cardiologist, or physical therapist, a referral from the PCP is usually mandatory. This referral acts as authorization from the insurance plan, ensuring that the specialist visit is covered under the policy. Without a referral, the visit may not be covered, or the policyholder may be responsible for a higher out-of-pocket cost.

The referral process in HMO POS plans is designed to streamline care and ensure that specialist visits are medically necessary. When a policyholder discusses their health concerns with their PCP, the PCP evaluates whether a specialist referral is appropriate. If it is, the PCP initiates the referral, which is then submitted to the insurance provider for approval. Once approved, the policyholder can schedule an appointment with the specialist. It’s important to note that referrals are often time-limited, meaning they may expire after a certain period if not used.

While referrals are a core component of HMO POS plans, there are exceptions to the rule. In emergencies, policyholders are not required to obtain a referral before seeking care. Additionally, some plans may allow direct access to certain specialists, such as obstetricians/gynecologists or mental health providers, without a referral. However, these exceptions vary by plan, so it’s crucial to review the specific terms of your HMO POS policy to understand what is and isn’t covered without a referral.

Navigating referral requirements in an HMO POS plan requires proactive communication with your PCP and a clear understanding of your plan’s guidelines. Policyholders should always confirm whether a referral is needed before scheduling a specialist appointment to avoid unexpected expenses. Additionally, keeping track of referral expiration dates and staying informed about any changes to the plan’s referral policies can help ensure seamless access to necessary care. By adhering to these requirements, policyholders can fully leverage the benefits of their HMO POS insurance while maintaining control over their healthcare costs.

Life Insurance: 15-Year Guarantee Explained

You may want to see also

Explore related products

![]()

Cost Differences and Benefits

HMO POS (Health Maintenance Organization Point of Service) insurance plans combine elements of traditional HMO and PPO (Preferred Provider Organization) plans, offering a unique blend of cost-saving features and flexibility. One of the primary cost benefits of HMO POS plans is their typically lower premiums compared to PPO plans. This is because HMOs emphasize preventive care and require members to choose a primary care physician (PCP) who coordinates all medical services, reducing administrative costs and unnecessary procedures. The POS component allows members to seek out-of-network care, but at a higher cost, providing a balance between affordability and flexibility.

When considering cost differences, HMO POS plans generally have lower out-of-pocket expenses for in-network services. Members pay fixed copays for doctor visits and prescriptions, and the plan covers a significant portion of preventive care at no additional cost. However, if a member chooses to go out-of-network, the costs can increase substantially, often requiring higher deductibles and coinsurance. This structure incentivizes staying within the network, which can lead to substantial savings over time. For individuals who prioritize predictable healthcare costs and are comfortable with a PCP managing their care, HMO POS plans offer a cost-effective solution.

Another benefit of HMO POS plans is their emphasis on preventive care, which can lead to long-term cost savings. Regular check-ups, vaccinations, and screenings are typically covered at no additional cost, helping to identify and address health issues early. This proactive approach can prevent more serious and expensive medical conditions down the line, reducing overall healthcare expenditures. Additionally, the coordination of care through a PCP ensures that treatments are streamlined and efficient, minimizing redundant tests and procedures that can drive up costs.

For those who value flexibility, the POS feature allows members to access out-of-network providers without completely sacrificing coverage. While this option is more expensive, it provides a safety net for individuals who may need specialized care not available within the network. This flexibility can be particularly beneficial for those with specific health needs or those who travel frequently and require access to healthcare outside their plan’s network. However, it’s important to weigh the higher costs of out-of-network care against the potential benefits to determine if this flexibility aligns with your healthcare priorities and budget.

In summary, HMO POS insurance plans offer a balance of cost savings and flexibility, making them an attractive option for many individuals. The lower premiums and predictable in-network costs make them budget-friendly, while the option to seek out-of-network care provides added versatility. By focusing on preventive care and coordinated treatment through a PCP, these plans can also reduce long-term healthcare expenses. When evaluating HMO POS insurance, consider your healthcare needs, budget, and preference for network flexibility to determine if this plan aligns with your goals for cost-effective and comprehensive coverage.

UPS Insurance: Are Your Collectible Coins Covered?

You may want to see also

Frequently asked questions

HMO POS stands for Health Maintenance Organization Point of Service. It combines features of an HMO and a POS plan, offering a primary care physician (PCP) and the option to seek care outside the network for an additional cost.

Unlike a traditional HMO, which restricts care to in-network providers, HMO POS allows policyholders to visit out-of-network providers, though at a higher cost and often requiring a referral from their PCP.

Yes, HMO POS typically requires a referral from your primary care physician (PCP) to see a specialist, whether in-network or out-of-network. This helps manage costs and coordinate care.