The cost of healthcare is a significant concern for many households, with medical expenses often placing a financial burden on individuals and families. Medical expenditure rates for insurance refer to the amount of money that individuals, employers, and insurance companies spend on healthcare services and treatments. These rates can vary depending on factors such as age, health status, insurance coverage, and income. For example, older adults and individuals with chronic illnesses tend to incur higher medical costs. Additionally, the type of insurance plan, whether private or public, can also impact expenditure rates, with private plans typically paying higher prices for healthcare. Understanding medical expenditure rates is crucial for evaluating the affordability and accessibility of healthcare, as well as for making informed decisions about insurance coverage and financial planning.

Explore related products

What You'll Learn

![]()

Average medical spending increases with age

It is a well-known fact that health spending increases with age. As we grow older, we tend to have more health conditions and need more care. This results in higher medical expenditures. While it is true that a person's health status and, consequently, their need for healthcare can vary over their lifetime, older adults are more likely to require more costly healthcare. This is reflected in the data, which shows that, on average, healthcare costs are nearly triple when a person reaches the age of 65 compared to their 20s and 30s.

The Medical Expenditure Panel Survey (MEPS) provides detailed healthcare spending data segmented by age and demographics. According to the MEPS data, healthcare costs are lowest from age 5 to 17, averaging around $2,000 per year. However, from then on, costs rise steadily, reaching over $11,000 per year for those over 65. It is worth noting that these costs may be covered by private insurance or Medicare, but not all expenses are always included, and unexpected bills can have a significant financial impact.

The variation in health expenditures across different population groups is also influenced by factors such as race, ethnicity, and insurance coverage. In the United States, White people have significantly higher average total health spending than other racial and ethnic groups. This can be attributed to various factors, including health status, age distribution, and access to care. For example, Hispanic and Black people are more likely to be uninsured and report delaying or forgoing medical care due to financial constraints.

The distribution of health spending across different sectors is also noteworthy. In the United States, the federal government is the largest sponsor of health spending, accounting for 32%, followed by households at 27%. Private businesses contribute 18% to total health care spending, while state and local governments account for 16%. These proportions can vary from year to year, with projections indicating an overall increase in health spending relative to GDP over the next several years.

While health spending generally increases with age, there are exceptions to this trend. For instance, individuals aged 60-64 enrolled in large employer plans may have higher average spending than traditional Medicare beneficiaries aged 65-69. Additionally, a small portion of the population can be responsible for a large share of health spending in a given year. This variability in health spending underscores the importance of considering individual circumstances when planning for healthcare costs during retirement.

Chase Sapphire: Medical Insurance Coverage While Traveling

You may want to see also

Explore related products

$199.95 $245.95

![]()

People in the US with higher incomes spend more on healthcare

The US spends more on healthcare than any other high-income country, yet it often performs worse on measures of health and healthcare. A study by RAND found that higher-income American households pay the most to finance the nation's healthcare system. However, the burden of payments as a share of income is greatest among households with the lowest incomes. Middle-income households pay between 19.8% and 23.2% of their income towards healthcare, while the average household pays 18.7% of their income on healthcare.

The high cost of healthcare in the US is a well-documented issue, with Americans spending far more on diagnostic tools like MRIs than their international peers. The lack of universal health coverage in the US means that affordability is a significant barrier to accessing healthcare, and high out-of-pocket costs lead many adults to skip or delay necessary medical care. The RAND study also found that Americans with Medicare receive the greatest dollar value of healthcare, as older people generally use more healthcare services. Those with Medicaid have the largest dollar value of healthcare received as a percentage of income, corresponding to their lower income and poorer health.

The rising cost of healthcare in the US is a key driver of the country's unsustainable national debt, and it has also hindered the response to public health crises like the COVID-19 pandemic. Healthcare prices are a significant factor in high healthcare spending, as the cost of healthcare services typically grows faster than the cost of other goods and services in the economy. In recent years, the Consumer Price Index for All Urban Consumers (CPI-U) for medical care has been higher than the overall CPI-U. Analysts attribute this to wage increases for health workers and delays in observable price increases due to healthcare prices being set in advance.

The aging population in the US is another factor contributing to increased healthcare spending, as individuals over 65 spend more on healthcare than any other age group. As the number of older Americans grows, total healthcare costs are expected to rise. While higher-income households may be able to absorb the financial burden of high healthcare costs, lower-income households are disproportionately affected, highlighting the need for healthcare reform to ensure affordable and accessible healthcare for all Americans.

Medical Insurance Adequacy: 25,000 Enough for Vehicle Coverage?

You may want to see also

Explore related products

![]()

People of colour are younger, on average, than white people

It is important to acknowledge that while racial differences in the ageing process exist, how a person ages is not solely dependent on their race. A person will age uniquely, regardless of their racial background. However, research has shown that people of colour, particularly those with darker skin, tend to exhibit signs of ageing later than their white counterparts.

One factor contributing to this is the collagen arrangement in the skin. Collagen is a protein that provides structural support, keeping the skin firm, supple, and elastic. As people age, their collagen levels decline, leading to thinner and weaker skin. Research from 2016 found that Black people tend to have a more beneficial arrangement of collagen in their skin. The collagen bundles are more compact and help maintain structural integrity, resulting in a more youthful appearance for a longer period than white skin. Additionally, Black skin has been found to have more numerous and larger fibroblasts, which are cells that synthesise the structural elements of the skin.

Asian skin, including Chinese and Japanese skin, has also been found to exhibit slower ageing. Studies have shown that Asian skin has a thicker dermis, containing more collagen. As a result, Asian females may not notice wrinkles until they reach their 50s.

Another factor influencing the perception of age across different racial groups is skin pigmentation. Skin texture studies have shown that skin colour distribution can account for up to 20 years of perceived age. People with darker skin are generally thought to have firmer and smoother skin than those with lighter skin of the same age. However, as darker-skinned individuals age, they may experience mottled pigmentation, wrinkles, and skin laxity. Additionally, they may be more prone to developing certain skin conditions, such as dermatosis papulosa nigra and seborrheic keratoses, which are harmless skin growths.

While people of colour may exhibit signs of ageing later, it is important to note that societal perceptions of age can vary across cultures. Studies have shown that, across different cultures, women who appear younger are consistently rated as more attractive. This preference for a youthful appearance can influence societal perceptions of age and attractiveness.

Cobra Medical Insurance Premiums: Tax-Deductible Expenses?

You may want to see also

Explore related products

![]()

Private health plans pay more for healthcare than public plans

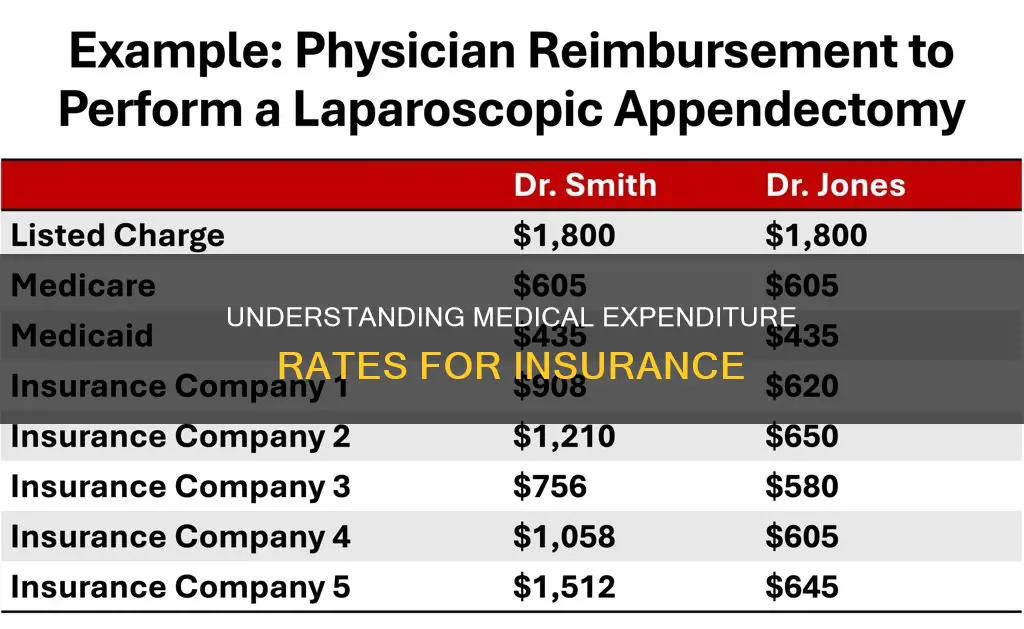

Private health insurance plans paid hospitals 224% more than public plans for inpatient and outpatient services in 2020, according to a RAND study. This significant discrepancy is driven by various factors, including mergers and acquisitions, affiliation agreements, and other consolidations that increase hospitals' pricing leverage. Private insurers paid 222% of Medicare prices in 2018, which further increased to 235% in 2019.

The growth in healthcare spending differs between government and private insurance. Government insurance programs, such as Medicare and Medicaid, made up 45% of national healthcare spending in 2023, amounting to $2.1 trillion. In contrast, private insurance programs, including employer-provided health insurance and plans purchased through the Affordable Care Act, accounted for 32%, or about $1.5 trillion. Private insurance plans are the largest single source of funding for healthcare expenditures, followed by Medicare and Medicaid.

The costs associated with private health plans include premiums, deductibles, and enrollee contributions. In 2022, the average monthly premiums for employer-sponsored plans were lower than for Marketplace plans. However, after employer contributions and tax credits, the average enrollee contributions for employer-sponsored plans were higher. Private health plan spending is projected to surpass $1.5 trillion in 2024, impacting enrollees, employers, and the federal government.

While the pricing between private and public health plans varies, the services rendered and the population enrolled in each type of program also influence the overall costs. Medicare, for example, does not provide coverage for hearing aids or dentures. Additionally, the growth in Medicaid payments is driven by spending on dental services, professional services, and health and personal care expenditures. The complexity of the healthcare system and the lack of transparency in pricing make it challenging to directly compare the costs of private and public health plans.

Lucrative Medical Coding and Billing: Salary Insights

You may want to see also

Explore related products

![]()

Medical expenses can be claimed as tax deductions

To claim medical expense deductions, you must itemize your deductions on Schedule A (Form 1040). This means that your total itemized deductions should exceed the standard deduction to make itemizing more beneficial. The IRS allows taxpayers to deduct qualified unreimbursed medical care expenses that exceed 7.5% of their adjusted gross income (AGI). For example, if your AGI is $45,000 and your medical expenses are $5,475, you would multiply $45,000 by 0.075, resulting in $3,375. Therefore, only expenses exceeding this amount can be included as itemized deductions, leaving you with a medical expense deduction of $2,100.

Deductible medical expenses can include fees paid to doctors, dentists, surgeons, chiropractors, psychiatrists, psychologists, and non-traditional medical practitioners. Inpatient hospital care or residential nursing home care expenses may also be deductible, provided that the availability of medical care is the principal reason for residence. Additionally, amounts paid for acupuncture, inpatient treatment for drug or alcohol addiction, smoking cessation programs, and prescription drugs to alleviate nicotine withdrawal can be deducted.

Transportation expenses primarily for and essential to medical care may also qualify for the medical expense deduction. This includes out-of-pocket costs for personal vehicles, such as gas and oil, as well as the standard mileage rate for medical expenses, tolls, parking fees, and taxi, bus, or train fares. Self-employed individuals may also be eligible for the self-employed health insurance deduction, which is an adjustment to income for premiums paid on a health insurance policy covering medical care for themselves and their dependents.

Life Insurance Medicals: What to Expect

You may want to see also

Frequently asked questions

The medical expenditure rate for insurance varies depending on factors such as age, race, income, and type of insurance plan. For example, in 2021, people aged 55 and over accounted for 55% of total health spending, despite only making up 31% of the population. On the other hand, people under 35 made up 44% of the population but were responsible for only 21% of health spending. In terms of race and ethnicity, differences in health spending may be driven by factors such as health status, insurance coverage, and access to care. Private health plans also tend to pay higher prices for healthcare than public plans.

Medical expenses that are not fully covered by your insurance may be tax-deductible. The IRS allows deductions for unreimbursed expenses for preventative care, treatment, surgeries, dental and vision care, and mental health services. Additionally, unreimbursed payments for prescription medications and medical appliances, such as glasses and hearing aids, are also deductible. To claim the medical expense deduction, you must itemize your deductions and ensure they exceed 7.5% of your adjusted gross income.

Any medical expenses that are reimbursed, such as by insurance or an employer, are generally not tax-deductible. The IRS typically disallows expenses for cosmetic procedures and nonprescription drugs (except insulin). Other non-deductible purchases include general health items like toothpaste, health club dues, vitamins, diet food, and nonprescription nicotine products. Medical expenses paid in a different year or with funds from a flexible spending or health savings account are also not deductible.