Your credit score is a key factor in determining the rate you will pay for your mortgage insurance. The higher your credit score, the lower your PMI premium will be. Generally, a higher credit score means a lower mortgage rate. Credit scores for a conventional mortgage loan typically need to be at least 620, but FHA loans may accept as low as 500 with a larger down payment. The average cost of private mortgage insurance PMI for a conventional home loan ranges from 0.46% to 1.5% of the original loan amount per year, according to the Urban Institute's Housing Finance Policy Center. However, PMI can cost as much as 6% depending on factors such as the type of loan and whether it is a fixed-rate or adjustable-rate mortgage.

| Characteristics | Values |

|---|---|

| What is PMI? | Private mortgage insurance (PMI) is a type of insurance policy that protects lenders from the risk of default or nonpayment by the borrower. |

| Who needs PMI? | PMI is required when the down payment is less than 20% of the home price. |

| How much does PMI cost? | PMI rates typically range from 0.5% to 1.5% of the loan amount annually, but can be as high as 6%. The cost depends on factors such as credit score, loan term, loan type, and debt-to-income ratio. |

| How to calculate PMI cost? | A PMI calculator can be used to estimate the cost of PMI based on loan amount, down payment, and credit score. |

| How to lower PMI cost? | A larger down payment, a higher credit score, and a lower debt-to-income ratio can help reduce PMI costs. |

| Alternatives to PMI | Lender-paid PMI (LPMI) is an option where the lender pays the PMI upfront and the borrower repays with a higher interest rate. Another alternative is a piggyback loan, which involves a second mortgage to cover the additional amount needed to reach 20% equity. |

Explore related products

What You'll Learn

![]()

Credit score

A credit score is a numerical representation of an individual's creditworthiness and their ability to repay debts on time and in full. Credit scores are based on credit history, including the number of late payments and the total amount of debt outstanding. A credit score can range from 300 to 850.

Lenders will use your credit score to determine the mortgage rate you qualify for. Generally, a higher credit score means a lower mortgage rate. For example, individuals with excellent credit (720 and above) usually secure the best rates, while scores below 640 can lead to significantly higher rates.

In addition to the mortgage rate, your credit score can also impact the cost of private mortgage insurance (PMI). PMI is a type of insurance policy that protects lenders from the risk of default or nonpayment by the borrower. The higher your credit score, the lower your PMI premium will be. This is because a higher credit score indicates that you are more creditworthy and less likely to default on your loan. Conversely, a lower credit score may lead to a higher PMI premium as the lender may have less faith in your ability to manage your debt responsibly.

It is important to note that PMI is typically only required when the down payment on a house is less than 20% of the selling price. In this case, the lender will require the borrower to purchase PMI from a PMI company prior to signing off on the loan. The PMI premium can range from 0.5% to 6% of the loan balance annually, depending on various factors, including the loan type and the borrower's credit score.

To avoid paying PMI, individuals can opt for a conventional mortgage, which typically requires a higher down payment of at least 20%. Additionally, building your credit score, paying down debt, and making a larger down payment may help reduce your overall PMI costs.

Speeding Tickets: Impact on Insurance and What to Know

You may want to see also

Explore related products

![]()

Loan type

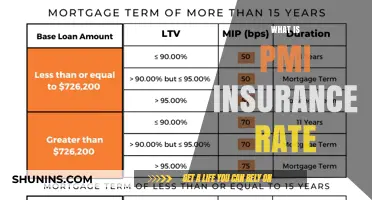

The type of loan you take out will determine the type of mortgage insurance you need and how much it will cost. The most common types of mortgage insurance are private mortgage insurance (PMI) and mortgage insurance premium (MIP).

Private Mortgage Insurance (PMI)

Private mortgage insurance is a type of insurance that you might need to buy if you take out a conventional loan with a down payment of less than 20% of the purchase price. PMI is arranged by the lender and provided by private insurance companies. It insures the lender against loss caused by borrowers failing to make loan payments.

Mortgage Insurance Premium (MIP)

Mortgage Insurance Premium (MIP) is a special type of mortgage insurance for loans backed by the Federal Housing Administration (FHA). MIP is required for every FHA loan, not just loans with a down payment of less than 20%. FHA mortgage insurance includes both an upfront cost, paid as part of your closing costs, and a monthly cost, included in your monthly payment.

Other Types of Loan

If you get a Department of Veterans’ Affairs (VA)-backed loan, the VA guarantee replaces mortgage insurance. With VA-backed loans, there is no monthly mortgage insurance premium, but you pay an upfront “funding fee”. The amount of the fee varies depending on several factors.

If you get a U.S. Department of Agriculture (USDA) loan, the program is similar to the Federal Housing Administration, but typically cheaper. You pay for the insurance both at closing and as part of your monthly payment.

Understanding Auto Insurance Vehicle Symbols and Their Meanings

You may want to see also

Explore related products

![]()

Down payment

A down payment is the percentage of the purchase price of a home that the buyer pays upfront. Typically, down payments are between 5% and 20% of the home's purchase price, but this can be as little as 3%. The amount of the down payment can impact the terms of the mortgage loan. For example, a larger down payment can result in a lower interest rate on the loan.

If a buyer makes a down payment of less than 20% of the home's value, they may be required to purchase private mortgage insurance (PMI). PMI is a type of insurance that protects the lender in case the borrower defaults on their loan payments. The cost of PMI can vary depending on the down payment amount and credit score, but it typically ranges from 0.1% to 2% of the loan balance per year. PMI is usually paid monthly and can add a significant amount to the overall cost of the loan.

There are ways to avoid paying PMI, even with a down payment of less than 20%. One option is lender-paid mortgage insurance (LPMI), where the lender covers the cost of the insurance, but the borrower pays a higher interest rate on the loan. Another option is a piggyback mortgage or 80-10-10 loan, where the buyer puts down 10% in cash and takes out a second mortgage loan for the remaining 10%, resulting in a total down payment of 20%.

It's important to carefully evaluate your finances and consider all your options before deciding on a down payment amount. There are various types of loans available, and the down payment requirements and costs can vary depending on the lender and market conditions. Additionally, many state, county, and city governments offer down payment assistance programs to qualified individuals.

Understanding Cmp Auto Insurance: What Does It Cover?

You may want to see also

Explore related products

![]()

Debt-to-income ratio

Your debt-to-income ratio, or DTI ratio, is an important part of your overall financial health. It is calculated by dividing your monthly debt payments by your monthly gross income (before taxes). The ratio is expressed as a percentage, and lenders use it to determine the risk associated with lending to you. A higher DTI ratio presents more risk for a lender and could prevent you from getting a loan or mortgage.

When calculating your DTI ratio, you should include monthly debt payments such as rent, mortgage, credit card payments, car payments, student loans, and other debt obligations. It is important to note that expenses like groceries, utilities, and gas are generally not included.

There are two components that lenders use to calculate the DTI ratio: the front-end ratio and the back-end ratio. The front-end ratio, also known as the housing ratio, shows what percentage of your monthly gross income would go towards your housing expenses, including your mortgage payment, property taxes, homeowners insurance, and any homeowners association dues. The back-end ratio, or total debt ratio, shows what percentage of your income is needed to cover all of your monthly debt obligations.

Keeping your DTI ratio low is beneficial, as it can help you secure better mortgage rates and loan terms. Lenders typically view borrowers with lower DTIs as less risky. To improve your DTI ratio, you can focus on increasing your income, reducing your debt, or both. It is also important to consider your budget and create a plan to reduce debt, such as the snowball or avalanche methods.

Additionally, your DTI ratio can impact the cost of private mortgage insurance (PMI). PMI is required when the down payment on a house is less than 20% of the selling price. Borrowers with higher credit scores and lower DTIs typically pay lower PMI rates.

Auto Insurance and Personal Injury: What's Covered?

You may want to see also

Explore related products

![]()

Property value

For example, if an individual purchases a property worth $200,000 and takes out a mortgage loan of $160,000, the LTV ratio would be 80% ($160,000 / $200,000). In this case, the lender may consider the loan to be relatively low risk, as the borrower has a substantial amount of equity in the property. However, if the same individual only made a down payment of $10,000, resulting in a loan amount of $190,000, the LTV ratio would increase to 95% ($190,000 / $200,000). This higher LTV ratio would likely lead to a higher PMI rate, as the lender is assuming more risk by financing a larger portion of the property's value.

It's important to note that the LTV ratio is not the sole factor in determining PMI rates. Credit score also plays a significant role, with higher credit scores generally resulting in lower PMI costs. Additionally, the type of loan, such as a fixed-rate or adjustable-rate mortgage, can impact the PMI rate. Adjustable-rate mortgages are often considered riskier for lenders, leading to potentially higher PMI payments.

Furthermore, property value fluctuations can impact the timeline for PMI removal. If property values in the area increase, the borrower may reach the required 20% equity threshold sooner, even without making additional payments toward the principal. On the other hand, if property values decline, it may take longer to reach the necessary equity level.

In summary, property value is a critical component in determining PMI rates and the duration of PMI payments. Lenders use the LTV ratio, which is influenced by the property value, to assess the risk associated with the loan. Higher property values relative to the loan amount can lead to lower PMI rates, while lower property values or higher loan amounts can result in higher PMI costs. Additionally, property value appreciation or depreciation can impact the timeline for removing PMI from the loan.

Auto Body Repair Shops: Waiving Insurance Deductibles and Ethical Implications

You may want to see also

Frequently asked questions

Private mortgage insurance rates typically range from 0.5% to 1.5% of the loan amount annually. However, the rate can be as high as 6% depending on factors such as the type of loan and credit score.

The higher the credit score, the lower the PMI premium. Borrowers with lower credit scores pay more for PMI than borrowers with higher credit scores.

Fixed-rate loans usually have lower mortgage insurance rates than adjustable-rate mortgages (ARMs) because they reduce the amount of risk involved with the loan.

In addition to the loan type and credit score, the PMI rate also depends on the size of the loan, the down payment amount, debt-to-income ratio, and loan-to-value ratio.