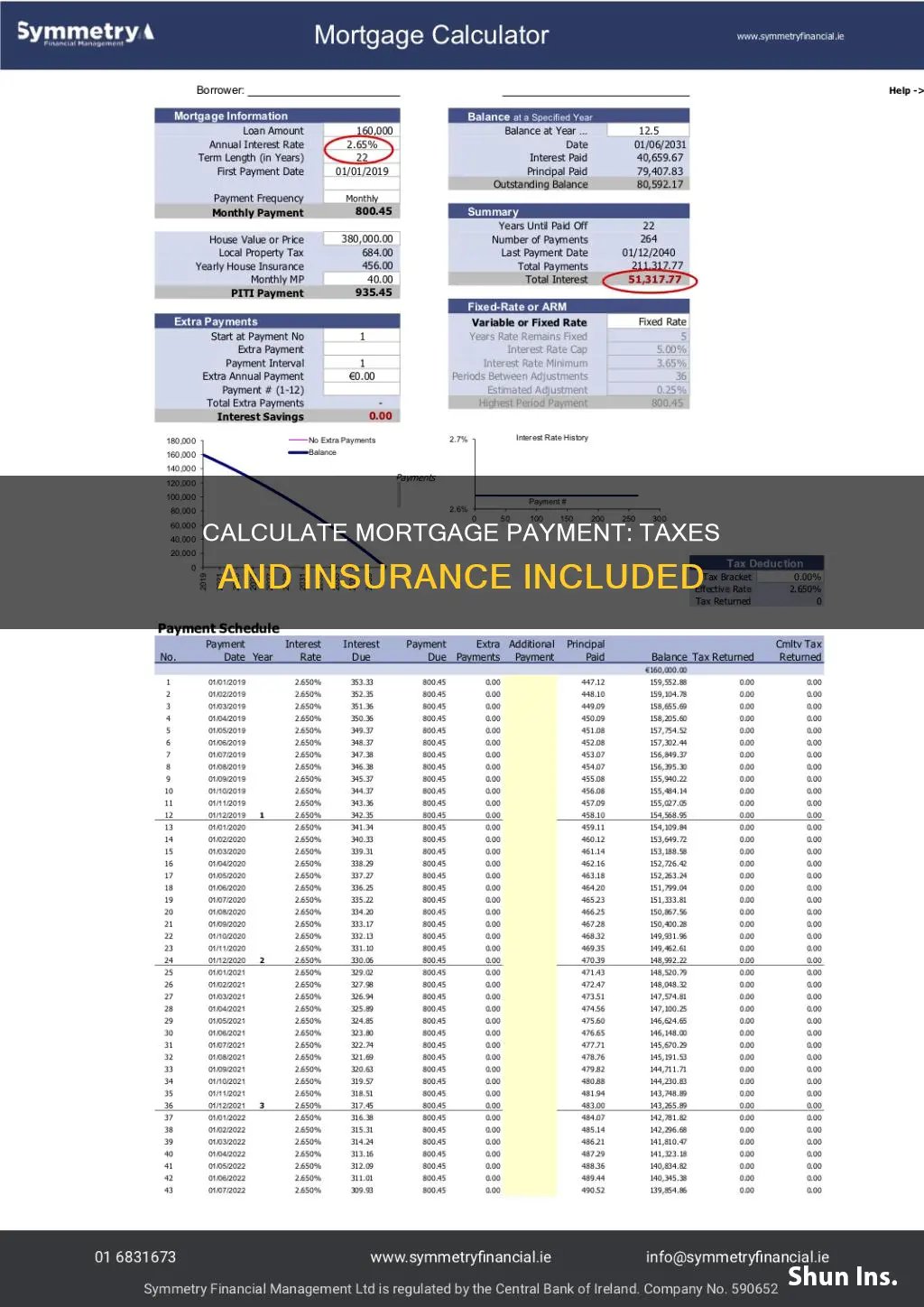

When taking out a mortgage, it is important to understand the monthly costs involved. Mortgage calculators can help you to estimate your monthly payments, including property taxes, insurance and other fees. These calculators take into account the home price, mortgage rate, loan term and down payment to calculate the monthly payments you can expect to make towards principal and interest. By using a mortgage calculator, you can determine if you are spending more than you can afford and make informed decisions about your mortgage options. It is also important to consider other financial considerations such as upfront costs and recommended income to safely afford your new home.

| Characteristics | Values |

|---|---|

| Purpose | To estimate monthly mortgage payments, including principal, interest, taxes, insurance, and other fees. |

| Inputs | Home price, down payment, mortgage rate, loan term, property taxes, insurance, HOA fees, extra payments, etc. |

| Outputs | Monthly payment, payment schedule, total interest paid, amortization period, etc. |

| Assumptions | Typically assumes a 20% down payment unless specified otherwise. May assume national averages for taxes and insurance if not overridden. |

| Considerations | Upfront costs, recommended income, loan term options, debt-to-income ratio, and other financial considerations. |

| Additional Features | Ability to fine-tune payments, compare scenarios, and calculate without accounting for home value appreciation or inflation. |

| Limitations | Does not include all costs and savings, e.g., utilities, home maintenance, tax deductions, etc. |

| Intended Users | Prospective homeowners, refinancing homeowners, financial advisors, mortgage loan officers, etc. |

Explore related products

What You'll Learn

![]()

Down payments and their impact on monthly payments

The amount of your down payment will directly impact your monthly mortgage payments. A higher down payment will result in lower monthly payments and vice versa. A larger down payment shrinks the loan balance upfront, which means you'll pay less each month.

A down payment of 20% or more is ideal as it can help you avoid mortgage insurance and earn a lower interest rate. Private mortgage insurance (PMI) is usually required when you take out a conventional loan and make a down payment of less than 20% of the home's purchase price. PMI serves to protect the lender if the buyer stops making payments on the loan. The cost of PMI is typically anywhere from 0.2% to 1.5% of the total loan amount.

A larger down payment can also increase your home equity. Your down payment immediately gives you equity in your home, which can help you avoid going underwater on your loan and is available to borrow against later.

However, a larger down payment may not always be feasible or desirable. It may push out your home purchase timeline and deplete your savings. A lower down payment can help you buy a home sooner and allow you to put money toward other financial goals, such as retirement or investments.

Additionally, the required down payment amount will vary depending on the loan type and your financial situation. Some government-backed loan programs, such as USDA loans, require no down payment or mortgage insurance. Other lenders offer low down payment options, but you may pay a higher interest rate.

It's important to weigh the advantages and disadvantages of both large and small down payments and consider your long-term homeownership goals when deciding on the down payment amount that's right for you.

Mortgage Insurance: When Does It End?

You may want to see also

Explore related products

![]()

How to calculate your DTI

When applying for a mortgage, lenders will calculate your debt-to-income (DTI) ratio to determine whether you can repay your loan. The DTI ratio is the percentage of your gross monthly income that goes toward paying off debts. It is calculated by dividing your monthly debt payments by your monthly gross income.

To calculate your DTI, first, add up your monthly debt payments, including car loan payments, credit card minimum payments, student loan payments, and personal loan payments. If you are taking out the mortgage with a co-borrower, include their debt payments as well. You can also include your estimated mortgage payment, homeowners insurance premium, and property tax payment.

Next, calculate your monthly gross income before deductions for taxes, retirement savings, and other items. Finally, divide your total monthly debt obligations by your monthly gross income. The result is your DTI ratio, expressed as a percentage.

For example, let's say your monthly debt payments total $300, and your monthly gross income is $1,000. Dividing $300 by $1,000 gives you 0.3. To get the percentage, multiply by 100, resulting in a DTI of 30%.

Lenders use both the front-end and back-end ratios to calculate your DTI. The front-end ratio, or housing ratio, shows what percentage of your monthly gross income would go toward housing expenses, including your mortgage payment, property taxes, and insurance. The ideal front-end ratio is no more than 28%.

The back-end ratio, or total debt ratio, includes all your monthly debt obligations, plus your mortgage payments and other housing expenses. The ideal back-end ratio is no more than 36%, although lenders may accept higher ratios, sometimes up to 45% or 50%. It is generally better to keep your DTI ratio lower, as it improves your chances of securing a mortgage and can lead to better mortgage rates and loan terms.

Mini Tyre Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Property taxes

The amount of property tax varies depending on the location of the property. The national average in the US is 0.90% of the property's value, but this can differ significantly from state to state and even county to county. For example, New Jersey has the highest average effective property tax rate in the country, with homeowners paying 2.33% of the median home value.

When using a mortgage calculator, you can input the annual property tax amount, which will then be reflected in the monthly payment estimate. This can be useful in helping you understand the overall affordability of a property, as well as how much of your income will be dedicated to housing costs.

It is important to note that property taxes are recurring costs that increase over time due to inflation. Therefore, when calculating mortgage payments, it is advisable to consider not only the current property tax rate but also potential future increases.

Mortgage Insurance: APR's Lingering Cost?

You may want to see also

Explore related products

![]()

Homeowners insurance

It is important to note that the specific coverage provided by homeowners insurance can vary, and additional coverage may be required for certain risks. For example, if you live in an area prone to flooding or other natural disasters, you may need to purchase extra coverage. Similarly, if you have valuable possessions such as fine art or jewelry, you may need to request special endorsements to ensure they are covered by your policy.

The cost of homeowners insurance can depend on several factors, including the location and value of the home, as well as any additional coverage or endorsements required. By using online tools and calculators, you can estimate the potential cost of homeowners insurance and factor this into your mortgage payment calculations.

When considering homeowners insurance, it is advisable to shop around and compare quotes from multiple providers to find the best coverage and rates that fit your budget and specific needs. You may also be able to save money by bundling your homeowners insurance with other types of insurance, such as car insurance. Additionally, having security systems, smoke detectors, and fire safety equipment in your home may qualify you for discounts on your insurance premiums.

Insuring Personal Articles: What's Worth Your Money?

You may want to see also

Explore related products

![]()

Private mortgage insurance

PMI is not the same as homeowners insurance, which provides financial protection from damages to your home. PMI is an additional monthly cost that's rolled into your mortgage payment and protects only the lender, not the borrower. It's important to note that PMI does not protect you if you fall behind on your mortgage payments, and you can still lose your home through foreclosure.

The requirement to buy PMI usually applies when taking out a conventional loan or refinancing one when your equity is less than 20 percent of the home's value. Lenders are required to cancel PMI when the mortgage balance drops to 78% of the home's original value or once the borrower is halfway through the loan term, whichever comes first. This can be done by contacting the loan servicer to discuss options for termination. In some cases, the borrower may need to demonstrate a consistent payment history to be eligible for PMI cancellation.

PMI can help borrowers qualify for a loan they might not otherwise be able to get. It allows buyers to enter a challenging housing market even if they haven't saved up a large down payment. However, it increases the overall cost of the loan. Borrowers considering PMI should carefully weigh the pros and cons based on their financial situation and seek detailed pricing information from lenders to make an informed decision.

Untangling the Web: Navigating the Termination of Sub-Producer Contracts with Farmers Insurance

You may want to see also

Frequently asked questions

Your monthly mortgage payment is made up of the principal, which is the original amount borrowed, and interest, which is the cost of borrowing the principal. It may also include property taxes, homeowners insurance, and homeowners association (HOA) fees.

Property taxes are an annual tax assessed by a government authority on your home and land. You pay a portion of your annual tax bill with each mortgage payment, and the servicer saves it in an escrow account. When the taxes are due, the loan servicer pays them.

Homeowners insurance is an annual fee you pay for a policy that covers damage to your property and the things you keep in it. It can also contain personal liability coverage, which protects against lawsuits involving injuries that occur on and off the property.

HOA fees are monthly dues that are used by a homeowners association — a group that manages planned neighbourhoods or condo communities. Payments go toward the maintenance of common areas used by all homeowners.