Self-insurance is a risk management strategy where an individual or organization chooses to set aside funds to cover potential losses instead of purchasing traditional insurance policies. By assuming the financial responsibility for claims, self-insured entities avoid paying premiums to external insurers, potentially saving costs if claims are minimal. However, this approach also exposes them to higher financial risks in the event of significant or unexpected losses. Self-insurance is commonly adopted by large corporations, government entities, and individuals with substantial assets, often in conjunction with high-deductible plans or stop-loss insurance to mitigate extreme liabilities. Understanding self-insurance requires evaluating its benefits, risks, and suitability based on financial stability, risk tolerance, and long-term goals.

| Characteristics | Values |

|---|---|

| Definition | A self-insured entity retains the financial risk of providing health, liability, or other benefits directly, rather than purchasing traditional insurance. |

| Common Users | Large employers, government entities, and organizations with significant financial resources. |

| Risk Retention | The entity assumes the risk of paying claims instead of transferring it to an insurance company. |

| Cost Control | Allows for greater control over claims management and administrative costs. |

| Funding Mechanism | Funds are set aside in a reserve or trust to cover anticipated claims. |

| Stop-Loss Insurance | Often paired with stop-loss insurance to limit catastrophic loss exposure. |

| Regulatory Compliance | Must comply with state and federal regulations, such as ERISA for employee benefits. |

| Administrative Burden | Requires dedicated resources for claims processing, compliance, and risk management. |

| Flexibility | Offers customization in benefit design and plan administration. |

| Financial Stability | Requires strong financial stability to cover potential large claims. |

| Tax Advantages | Self-insured plans may offer tax benefits, such as exempting premiums from payroll taxes. |

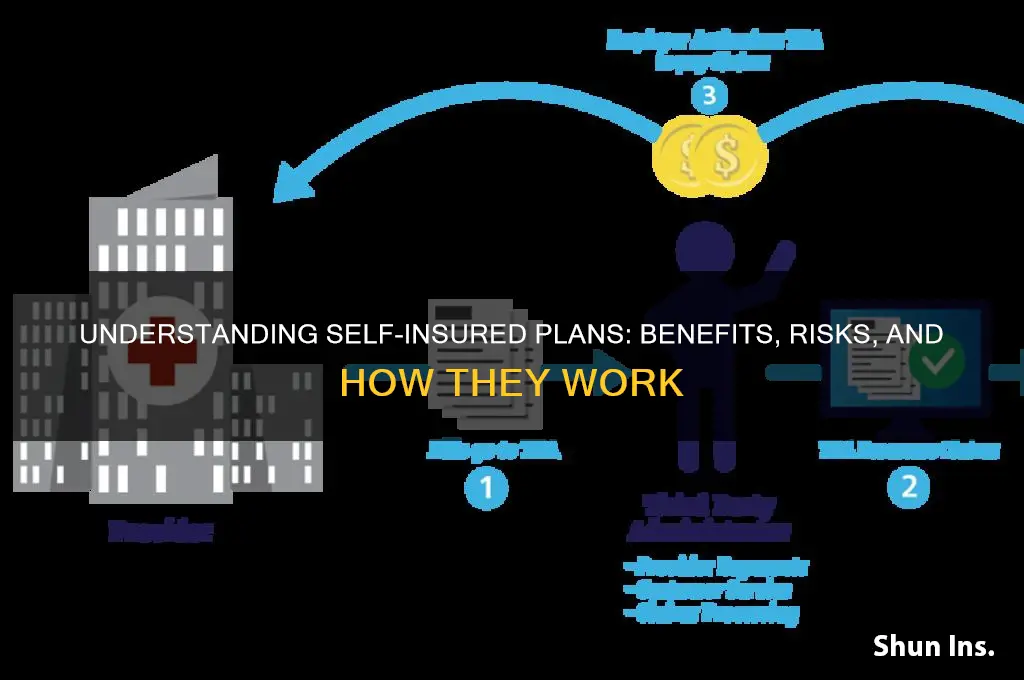

| Third-Party Administrators (TPAs) | Often use TPAs to handle claims processing and plan administration. |

| Data and Analytics | Access to detailed claims data allows for better risk management and cost analysis. |

| Employee Perception | Employees may perceive self-insured plans as more stable and employer-backed. |

| Market Trends | Increasingly popular among large employers due to rising insurance costs and desire for control. |

Explore related products

What You'll Learn

- Definition of Self-Insurance: Self-insurance means covering risks using own funds instead of purchasing external insurance policies

- Advantages of Self-Insurance: Reduces costs, increases control, and allows retention of investment income from reserves

- Disadvantages of Self-Insurance: Higher financial risk, requires large reserves, and lacks risk diversification benefits

- Self-Insurance vs. Traditional Insurance: Compares cost, risk exposure, and administrative responsibilities between the two methods

- Industries Using Self-Insurance: Common in healthcare, large corporations, and industries with predictable, manageable risks

![]()

Definition of Self-Insurance: Self-insurance means covering risks using own funds instead of purchasing external insurance policies

Self-insurance is a risk management strategy where an individual or organization chooses to set aside their own funds to cover potential losses instead of purchasing traditional insurance policies from external providers. This approach involves retaining the financial responsibility for risks rather than transferring it to an insurance company. By doing so, the self-insured party assumes the role of the insurer, using their own resources to pay for claims or liabilities as they arise. This method is often adopted when the cost of external insurance is deemed too high or when the entity believes it can manage the risks more efficiently on its own.

The decision to self-insure is typically based on a thorough assessment of the potential risks and the financial capacity to absorb losses. For businesses, this might involve analyzing historical claims data, industry trends, and the overall financial health of the organization. Individuals, on the other hand, might consider their personal savings, income stability, and the likelihood of facing significant expenses. Self-insurance is most viable when the risks are predictable and the entity has sufficient liquidity to handle unexpected costs without jeopardizing its operations or financial stability.

One of the key advantages of self-insurance is the potential for cost savings. Traditional insurance policies include premiums, administrative fees, and profit margins for the insurer, which can make them expensive. By self-insuring, entities can avoid these additional costs and retain control over their funds. Additionally, self-insurance allows for greater flexibility in managing claims, as the entity can set its own policies and procedures for handling losses without being bound by the terms of an external insurance contract.

However, self-insurance also comes with significant risks and responsibilities. Without the financial backing of an insurance company, the self-insured party must be prepared to cover all losses out of pocket. This can be particularly challenging in the event of a catastrophic claim, which could deplete reserves and threaten the financial health of the individual or organization. Therefore, self-insurance is often paired with risk mitigation strategies, such as implementing safety measures, maintaining emergency funds, or purchasing stop-loss insurance to limit exposure to extremely large losses.

In practice, self-insurance is commonly used by large corporations, government entities, and high-net-worth individuals who have the financial resources and risk management expertise to handle potential liabilities. For example, a multinational company might self-insure its workers' compensation claims or property damage risks, while an individual with substantial savings might choose to self-insure against minor medical expenses. Despite its benefits, self-insurance requires careful planning, disciplined financial management, and a clear understanding of the risks involved to be effective.

Clinical Trials: Life Insurance Impact and Influence

You may want to see also

Explore related products

![]()

Advantages of Self-Insurance: Reduces costs, increases control, and allows retention of investment income from reserves

Self-insurance is a risk management strategy where an individual or organization sets aside funds to cover potential losses instead of purchasing traditional insurance policies. This approach offers several distinct advantages, particularly in terms of cost reduction, increased control, and the ability to retain investment income from reserves. By opting for self-insurance, entities can avoid the overhead costs associated with insurance premiums, which often include administrative fees, profit margins for insurers, and other expenses. Over time, these savings can be substantial, especially for organizations with predictable and manageable risk profiles. This cost-efficiency is one of the primary reasons businesses and individuals consider self-insurance as a viable alternative to traditional coverage.

Another significant advantage of self-insurance is the increased control it provides over claims management and risk mitigation strategies. When self-insured, entities have the autonomy to design and implement their own claims processes, ensuring they align with their specific needs and operational standards. This control can lead to faster claims resolution, reduced administrative burdens, and a more personalized approach to handling losses. Additionally, self-insured entities can directly influence their risk management practices, investing in preventive measures and safety programs to minimize the likelihood of claims. This proactive approach not only reduces potential losses but also fosters a culture of accountability and risk awareness within the organization.

Self-insurance also allows entities to retain investment income generated from the reserves set aside to cover potential losses. In traditional insurance arrangements, premiums paid to insurers are often invested by the insurance company, with the returns benefiting the insurer rather than the policyholder. In contrast, self-insured entities can invest their reserves in financial instruments that align with their risk tolerance and financial goals, potentially earning significant returns over time. This retained investment income can offset the costs of self-insurance and even contribute to overall financial growth, making it an attractive financial strategy for those with sufficient capital and risk management capabilities.

Furthermore, self-insurance can enhance cash flow management by eliminating the need for large, periodic premium payments. Instead of paying premiums to an insurer, self-insured entities can allocate funds to reserves on a more flexible schedule, often in smaller, more manageable increments. This flexibility can improve liquidity and allow for better allocation of resources to other critical areas of the business. Additionally, self-insured entities are not subject to premium increases or policy cancellations, providing greater financial stability and predictability in the long term.

Lastly, self-insurance fosters a deeper understanding of an entity’s risk profile, encouraging a data-driven approach to risk management. By analyzing claims data and loss trends, self-insured organizations can identify areas of vulnerability and implement targeted interventions to mitigate risks. This analytical approach not only reduces the frequency and severity of losses but also positions the entity to make informed decisions about whether to retain certain risks or transfer them through alternative risk financing mechanisms. In this way, self-insurance serves as both a cost-saving strategy and a tool for enhancing overall risk resilience.

Understanding Insurance Cancellation: Qualifying Life Event?

You may want to see also

Explore related products

![]()

Disadvantages of Self-Insurance: Higher financial risk, requires large reserves, and lacks risk diversification benefits

Self-insurance, where an individual or organization assumes the financial risk of potential losses instead of purchasing traditional insurance, comes with several notable disadvantages. One of the most significant drawbacks is the higher financial risk it imposes. Unlike traditional insurance, where the risk is spread across a large pool of policyholders, self-insurance places the entire burden of a claim on the self-insured party. This means that a single catastrophic event, such as a major lawsuit or a severe accident, can result in substantial financial losses. For businesses, this could jeopardize their financial stability or even lead to bankruptcy if they are not adequately prepared to cover such expenses.

Another major disadvantage of self-insurance is that it requires large reserves to be set aside to cover potential claims. These reserves must be substantial enough to handle both expected and unexpected losses, which can tie up significant amounts of capital. For businesses, this means diverting funds that could otherwise be invested in growth, innovation, or operational improvements. Maintaining such reserves also requires careful financial management and forecasting, adding complexity to the organization’s financial planning. Small businesses or individuals with limited resources may find it particularly challenging to allocate sufficient funds for self-insurance.

Self-insurance also lacks the risk diversification benefits that traditional insurance provides. Traditional insurance pools risks across a wide range of policyholders, reducing the impact of any single claim on the insurer and the insured. In contrast, self-insurance concentrates the risk entirely on the individual or organization, leaving them vulnerable to the full financial impact of a loss. This lack of diversification can be especially problematic for entities operating in high-risk industries or those exposed to unpredictable events, as they bear the entire cost without the buffer of a shared risk pool.

Furthermore, self-insurance often requires a high level of expertise in risk management and claims handling, which can be a disadvantage for those without the necessary resources or experience. Managing claims internally can be time-consuming and complex, potentially leading to inefficiencies or errors. Traditional insurers, on the other hand, have specialized teams and processes to handle claims effectively, which self-insured entities may struggle to replicate. This can result in additional costs or complications when dealing with claims, further exacerbating the financial and operational challenges of self-insurance.

Lastly, self-insurance may not provide the same level of financial predictability as traditional insurance. With traditional insurance, premiums are fixed and known in advance, allowing for better budgeting and financial planning. In self-insurance, however, the costs are variable and depend entirely on the frequency and severity of claims. This unpredictability can make it difficult for individuals or organizations to manage their finances effectively, particularly in years with high claim volumes. For these reasons, while self-insurance offers certain advantages, its disadvantages—higher financial risk, the need for large reserves, and the lack of risk diversification—must be carefully considered before opting for this approach.

Term Life Insurance: 20-Year Policy Explained

You may want to see also

Explore related products

![]()

Self-Insurance vs. Traditional Insurance: Compares cost, risk exposure, and administrative responsibilities between the two methods

Self-Insurance vs. Traditional Insurance: A Comparative Analysis

Self-insurance is a risk management strategy where an individual or organization sets aside funds to cover potential losses instead of purchasing traditional insurance policies. When comparing self-insurance to traditional insurance, cost is a primary consideration. Traditional insurance involves paying premiums to a third-party insurer, which pools risk across many policyholders. While this provides predictable costs, premiums can be high, especially for businesses with low claims histories. Self-insurance, on the other hand, eliminates premium payments but requires setting aside a reserve fund. For entities with stable cash flows and low risk exposure, self-insurance can be cost-effective in the long term, as they retain funds that would otherwise go to insurers. However, it requires careful financial planning to ensure sufficient reserves are available when needed.

Risk exposure is another critical factor in the self-insurance vs. traditional insurance debate. Traditional insurance transfers risk to the insurer, capping potential losses at the policy deductible. This provides a safety net, particularly for catastrophic events. Self-insurance, however, retains all risk internally. While this can be advantageous for minor, predictable claims, it exposes the entity to significant financial liability in the event of a large loss. For example, a self-insured business facing a major lawsuit or natural disaster may deplete its reserves, threatening its financial stability. Thus, self-insurance is best suited for entities with strong risk management practices and the financial capacity to absorb potential losses.

Administrative responsibilities differ markedly between the two methods. Traditional insurance offloads much of the administrative burden to the insurer, including claims processing, compliance, and risk assessment. This allows businesses to focus on core operations. Self-insurance, however, requires substantial in-house administration. Entities must establish claims management processes, ensure compliance with regulations (such as those governing self-insured health plans), and monitor reserve adequacy. This can be resource-intensive, necessitating dedicated staff or external consultants. For smaller organizations, the administrative complexity of self-insurance may outweigh its potential cost savings.

In terms of flexibility, self-insurance offers greater control over coverage terms and claims handling. Traditional insurance policies often come with standardized terms and conditions, limiting customization. Self-insured entities can tailor their risk management strategies to their specific needs, such as adjusting deductibles or implementing preventive measures to reduce claims. However, this flexibility comes with the responsibility of staying informed about regulatory changes and industry best practices. Traditional insurance, while less flexible, provides the advantage of expert risk management from insurers, which can be particularly valuable for entities lacking specialized knowledge.

Finally, the decision between self-insurance and traditional insurance depends on an entity’s financial health, risk tolerance, and operational capacity. For large organizations with predictable losses and robust financial resources, self-insurance can reduce costs and increase control. However, smaller entities or those with high risk exposure may find traditional insurance more suitable due to its risk transfer benefits and lower administrative demands. Ultimately, a thorough analysis of cost, risk exposure, and administrative capabilities is essential to determine the most appropriate approach.

Assisted Death and Life Insurance: What's the Impact?

You may want to see also

Explore related products

![]()

Industries Using Self-Insurance: Common in healthcare, large corporations, and industries with predictable, manageable risks

Self-insurance is a risk management strategy where an entity, rather than purchasing traditional insurance, sets aside funds to cover potential losses directly. This approach is particularly common in industries with predictable and manageable risks, as it allows organizations to retain control over claims handling and reduce costs associated with premiums and insurer profit margins. Among the sectors that frequently adopt self-insurance, healthcare stands out prominently. Healthcare providers, including hospitals and large medical groups, often self-insure due to their ability to accurately predict claim frequencies and costs. By leveraging their extensive patient data and risk management expertise, these organizations can effectively manage liabilities while avoiding the overhead of commercial insurance policies.

Large corporations are another significant adopter of self-insurance, particularly for employee benefits like health and workers' compensation. Companies with substantial workforces, such as those in manufacturing, technology, and retail, find self-insurance advantageous because it allows them to tailor benefit plans to their employees' needs while minimizing administrative costs. Additionally, these corporations often have the financial stability to absorb potential losses, making self-insurance a viable and cost-effective option. For instance, workers' compensation self-insurance is common in industries with high injury rates but predictable claim patterns, enabling companies to implement proactive safety measures and manage claims more efficiently.

Industries with predictable, manageable risks are natural fits for self-insurance. For example, utilities and transportation companies often self-insure against property damage and liability claims due to their ability to forecast risks based on historical data and operational insights. Similarly, educational institutions, such as universities, may self-insure for property and liability risks, given their stable environments and risk mitigation strategies. These industries benefit from self-insurance by avoiding the volatility of insurance premiums and retaining funds that would otherwise be paid to insurers, which can then be reinvested into their operations.

The public sector, including municipalities and government agencies, also frequently employs self-insurance for various risks, such as property damage, liability, and employee benefits. Local governments, in particular, may self-insure to manage costs associated with maintaining public infrastructure and services. By pooling resources and establishing dedicated risk management departments, these entities can effectively handle claims and reduce reliance on external insurers. This approach not only saves costs but also ensures greater flexibility in addressing community-specific needs.

In summary, self-insurance is a strategic choice for industries with predictable, manageable risks, including healthcare, large corporations, and sectors like utilities, transportation, and the public sector. By retaining control over risk management and claims processing, these organizations can achieve cost savings, customize coverage, and reinvest retained funds into their operations. However, successful self-insurance requires robust financial planning, risk assessment capabilities, and compliance with regulatory requirements to ensure long-term sustainability.

Globe Life Insurance: What You Need to Know

You may want to see also

Frequently asked questions

Being self-insured means an individual or organization assumes the financial risk for potential losses instead of purchasing traditional insurance. They set aside funds to cover claims or expenses directly, rather than paying premiums to an insurance company.

Large corporations, government entities, and individuals with substantial assets often choose self-insurance. It’s common in industries like healthcare, workers’ compensation, and liability coverage, where the entity can predict and manage risks effectively.

Advantages include cost savings by avoiding insurance premiums, greater control over claims management, and the ability to retain investment income from reserved funds. It also allows for customization of coverage to fit specific needs.

The primary risk is the potential for catastrophic losses that exceed reserved funds, which could financially strain the self-insured entity. Additionally, self-insurance requires administrative resources to manage claims and compliance with regulations.