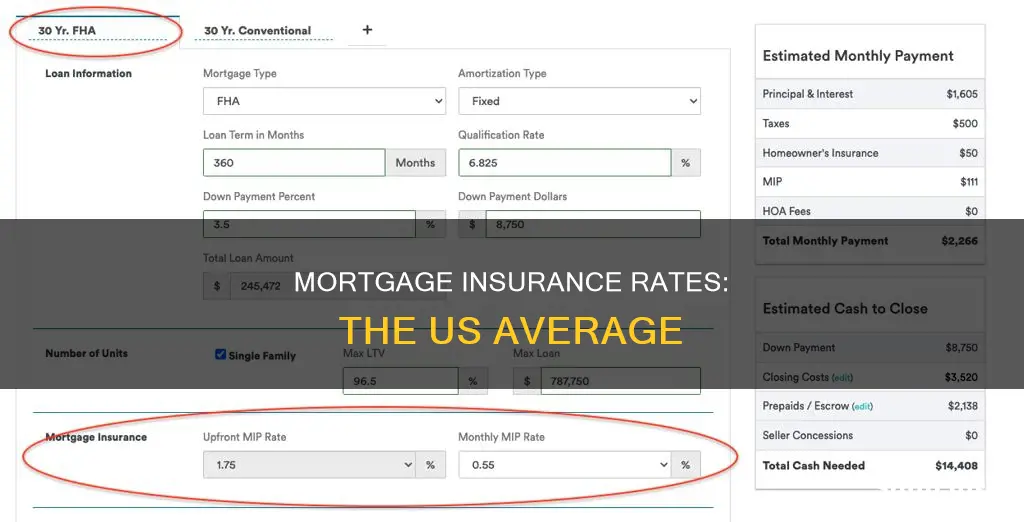

Mortgage insurance is an additional cost that you may face when buying a home. It is a type of insurance that protects the lender against the borrower not making payments. The average cost of homeowners insurance in the U.S. is about $2,110 a year for $300,000 worth of dwelling coverage, but rates vary by state. The average cost of private mortgage insurance, or PMI, for a conventional home loan ranges from 0.46% to 1.50% of the original loan amount per year, according to the Urban Institute's Housing Finance Policy Center. The cost of mortgage insurance depends on several factors, including the size of the loan, the down payment amount, debt-to-income ratio, and credit score. Lender-paid mortgage insurance is when the lender covers the mortgage insurance, but it usually results in a higher interest rate.

| Characteristics | Values |

|---|---|

| What is mortgage insurance? | A type of insurance that protects a mortgage lender against a borrower not making payments. |

| Who does it apply to? | Borrowers making smaller down payments (less than 20%). |

| Who does it protect? | The lender and its investment in the home, not the borrower. |

| Who pays the premiums? | The borrower. |

| How much does it cost? | The amount varies based on factors such as credit score, debt-to-income ratio, loan-to-value ratio, and down payment amount. |

| Average cost | According to the Urban Institute's Housing Finance Policy Center, the average cost of private mortgage insurance (PMI) for a conventional home loan ranges from 0.46% to 1.50% of the original loan amount per year. |

| How to avoid it | Put at least 20% down, choose a single premium PMI, request removal after the mortgage balance is 80% of the home's value, or opt for lender-paid PMI (which may result in a higher interest rate). |

| Home insurance rates | The average cost of homeowners insurance in the US is about $2,110 per year for $300,000 worth of dwelling coverage, but rates vary by state. |

Explore related products

What You'll Learn

- Mortgage insurance protects the lender from the buyer defaulting on their loan

- Lender-paid mortgage insurance is when the lender covers the insurance, usually resulting in a higher interest rate

- The average cost of private mortgage insurance is 0.46% to 1.50% of the original loan amount per year

- Mortgage insurance is usually required when the down payment is less than 20%

- The cost of mortgage insurance is influenced by factors such as credit score, debt-to-income ratio, and loan-to-value ratio

![]()

Mortgage insurance protects the lender from the buyer defaulting on their loan

Mortgage insurance is an insurance policy that protects the lender in the event of the buyer defaulting on their loan. It does not protect the buyer. The insurance pays the lender a portion of the balance due, and the lender may also require insurance if the borrower is refinancing with a conventional loan and has less than 20% equity in the home.

Mortgage insurance is usually required when the buyer's down payment is less than 20% of the purchase price of the home. This is because lenders typically lend an amount that equals 80% of the property's selling price, so the buyer must come up with the remaining 20% as a down payment. However, if the buyer cannot afford this, they can take out mortgage insurance to protect the lender, and therefore qualify for a loan that they may not otherwise have been able to get.

There are several types of mortgage insurance, including private mortgage insurance (PMI), qualified mortgage insurance premium (MIP) insurance, and mortgage title insurance. The type of insurance will determine who the policy protects in the event of specific cases of loss. For example, mortgage life insurance is designed to protect the heirs of the borrower if they die while still owing mortgage payments. The policy may pay off either the lender or the heirs, depending on the terms.

The average cost of private mortgage insurance for a conventional home loan ranges from 0.46% to 1.50% of the original loan amount per year, according to the Urban Institute's Housing Finance Policy Center. The cost varies depending on the size of the loan, the down payment amount, debt-to-income ratio, and credit score. For example, at an average rate of 0.46% to 1.50%, PMI on a $300,000 mortgage would cost $1,380 to $4,500 per year, or $115 to $375 per month.

There are ways to avoid paying for mortgage insurance. For example, buyers can save up to make a 20% down payment, or choose a single premium PMI, where a single payment is made to remove the PMI from a conventional mortgage. Buyers can also opt for a lender-paid PMI, but this usually results in a higher interest rate.

Auto Insurance Interest: Can You Charge It?

You may want to see also

Explore related products

![]()

Lender-paid mortgage insurance is when the lender covers the insurance, usually resulting in a higher interest rate

Lender-paid mortgage insurance (LPMI) is when the lender covers the mortgage insurance cost. This is usually in exchange for a higher interest rate on the loan. LPMI is an option for buyers who cannot afford a 20% down payment, which is the minimum amount required to avoid paying mortgage insurance. With LPMI, the lender assumes the cost of the insurance and then charges the buyer a higher interest rate on the loan to recoup the cost. This option may be appealing to high-income earners as mortgage interest is deductible on federal taxes.

The average cost of private mortgage insurance (PMI), for a conventional home loan ranges from 0.46% to 1.50% of the original loan amount per year, according to the Urban Institute's Housing Finance Policy Center. The cost varies depending on factors such as credit score, debt-to-income ratio, and loan-to-value ratio. Those with higher credit scores and lower debt-to-income ratios typically pay lower rates.

Lender-paid mortgage insurance is not a separate line item on your monthly bill. Instead, the cost is built into the interest rate of the loan. This means that you cannot cancel LPMI; it stays with the mortgage for the life of the loan unless you refinance. If you refinance and your loan-to-value ratio (LTV) is 80% or lower, you won't need to pay for LPMI or PMI. However, ridding yourself of mortgage insurance is usually not a good reason to refinance unless you can also qualify for a lower underlying rate.

LPMI can be a good option for buyers who don't want to pay high monthly PMI costs. For example, if you plan to sell your home after a few years, you may not reach the 20% equity mark required to drop the monthly PMI. In this case, LPMI may be more cost-effective, even with the higher interest rate.

It's important to note that LPMI may cost more over the life of the loan compared to PMI, which can be cancelled once certain conditions are met. When considering LPMI, it's advisable to compare multiple lenders to find the most favourable terms and rates.

Becoming an Auto Insurance Underwriter: Steps to Success

You may want to see also

Explore related products

![]()

The average cost of private mortgage insurance is 0.46% to 1.50% of the original loan amount per year

The cost of mortgage insurance is an additional expense that prospective homeowners may face when buying a home. Mortgage insurance, also known as private mortgage insurance (PMI), is typically required when a borrower makes a down payment of less than 20% on a conventional mortgage. In such cases, the borrower pays monthly premiums to protect the lender in the event of defaulting on the loan. While mortgage insurance allows borrowers to secure a loan with a smaller down payment, it increases their monthly payments and closing costs.

The average cost of private mortgage insurance for a conventional home loan ranges from 0.46% to 1.50% of the original loan amount per year. For example, on a $300,000 mortgage, the PMI would cost $1,380 to $4,500 per year, or approximately $115 to $375 per month. The specific rate within this range depends on several factors, including the size of the loan, the down payment amount, credit score, debt-to-income ratio, and loan-to-value ratio.

Borrowers with lower credit scores, higher debt-to-income ratios, and smaller down payments generally pay higher mortgage insurance rates. Conversely, those with higher credit scores, lower debt-to-income ratios, and larger down payments benefit from lower PMI costs. By building their credit score, reducing debt, and increasing their down payment, borrowers may be able to lower their PMI expenses.

It is worth noting that there are alternative options to avoid paying PMI. One option is to make a down payment of at least 20% on a conventional mortgage, eliminating the need for mortgage insurance altogether. Additionally, borrowers can explore lender-paid mortgage insurance, where the lender covers the PMI, but this usually results in a higher interest rate on the mortgage. Another option is a single premium PMI, which allows borrowers to make a one-time payment to remove PMI from a conventional mortgage. Lastly, borrowers can request the removal of PMI once their mortgage balance reaches 80% of the home's value.

Michigan Auto Insurance: Lowering Rates and Reform

You may want to see also

Explore related products

![]()

Mortgage insurance is usually required when the down payment is less than 20%

Mortgage insurance, also known as private mortgage insurance (PMI), is a type of insurance that is usually required when homebuyers make a down payment of less than 20% of the home's value. PMI protects the lender in the event that the borrower defaults on their loan. It is important to note that PMI does not protect the homebuyer; if they fall behind on mortgage payments, they can still lose their home through foreclosure.

The cost of PMI varies depending on several factors, including the size of the loan, the down payment amount, credit score, debt-to-income ratio, and loan-to-value ratio. According to the Urban Institute's Housing Finance Policy Center, the average cost of PMI for a conventional home loan ranges from 0.46% to 1.50% of the original loan amount per year. For example, PMI on a $300,000 mortgage would cost $1,380 to $4,500 per year, or $115 to $375 per month.

There are ways to avoid paying PMI, even if you make a down payment of less than 20%. One option is to choose a conventional loan with a higher interest rate, as some lenders offer loans with smaller down payments that do not require PMI. Another option is to use a piggyback loan, which can help you avoid PMI without increasing your mortgage rate. Additionally, once your home equity reaches 20%, you can request to cancel PMI payments.

It is worth noting that PMI can be beneficial for homebuyers as it may help them qualify for a loan that they might not otherwise be able to obtain. However, it is important to consider the additional cost of PMI when deciding on a mortgage.

New Vehicle, New Premium: Understanding Auto Insurance Hikes

You may want to see also

Explore related products

![]()

The cost of mortgage insurance is influenced by factors such as credit score, debt-to-income ratio, and loan-to-value ratio

The cost of mortgage insurance is influenced by a variety of factors, and it is important to understand how these factors interact to determine your monthly mortgage payment. Lenders will conduct a comprehensive review of your finances to determine your loan eligibility and the mortgage rate you are able to obtain.

One key factor is the loan-to-value (LTV) ratio, which is the comparison between the value of the loan and the appraised value of the home. A higher LTV ratio, coupled with a lower credit score, generally leads to higher mortgage insurance premiums. This is because a higher LTV indicates less equity in the home and poses a greater risk to the lender.

The debt-to-income ratio (DTI) is another important consideration. Lenders use this to assess the likelihood of the borrower being able to pay off the loan. The DTI calculates the percentage of monthly gross income that goes towards debt payments, including the future monthly mortgage payment. A lower DTI indicates lower risk and can lead to better mortgage rates.

Additionally, credit score plays a significant role in determining mortgage insurance costs. Higher credit scores reflect a better credit history and make borrowers eligible for lower interest rates. Most mortgage lenders use FICO scores and consider scores from the three major credit reporting companies (Equifax, Experian, and TransUnion), using the middle score to determine the rate.

It is worth noting that there are ways to avoid or reduce mortgage insurance costs. For example, putting at least 20% down on a conventional mortgage can eliminate the need for mortgage insurance. Alternatively, lender-paid mortgage insurance can be an option, although this usually results in a higher interest rate.

Insurance Rates for Teen Drivers: What's the Average?

You may want to see also

Frequently asked questions

Mortgage insurance is a type of insurance that protects the lender against a borrower not making payments. It is generally required when the borrower is making a small down payment.

The average cost of private mortgage insurance (PMI) for a conventional home loan ranges from 0.46% to 1.50% of the original loan amount per year. The cost varies depending on factors such as the size of the loan, the down payment amount, credit score, debt-to-income ratio, and loan-to-value ratio.

There are several ways to avoid or eliminate mortgage insurance:

- Make a down payment of at least 20%.

- Choose a single premium PMI, which allows you to make a single payment to remove PMI.

- Opt for lender-paid PMI, but be aware that this usually results in a higher interest rate.

- Request the removal of PMI once your mortgage balance reaches 80% of the value of your home.

Mortgage insurance protects the lender in case the borrower defaults on their loan, while homeowners insurance protects the homeowner's financial investment in their property. Homeowners insurance rates vary depending on factors such as location, age, square footage, and coverage limits. The national average cost of homeowners insurance is around $2,000 to $2,500 per year.

![NMLS Study Guide 2024-2025: 5 Full-Length MLO Practice Exams, SAFE Mortgage Loan Originator Test Prep Secrets Book with Detailed Answer Explanations: [3rd Edition]](https://m.media-amazon.com/images/I/61zi0BJms+L._AC_UL320_.jpg)