Cash value life insurance is a form of permanent life insurance that features a cash value savings component. This means that the policyholder can use the cash value for a variety of purposes, including borrowing or withdrawing cash from it, or using it to pay policy premiums. Cash value life insurance is more expensive than term life insurance, but it doesn't expire after a specific number of years.

| Characteristics | Values |

|---|---|

| Type | Permanent life insurance |

| Duration | Lifetime of the holder |

| Features | Cash value savings component |

| Cash value uses | Borrowing, withdrawing, paying policy premiums |

| Policy types | Whole life, universal life, variable life, indexed life |

| Cost | More expensive than term life insurance |

| Expiry | Does not expire after a specific number of years |

| Borrowing | You may borrow against the policy |

| Interest | Earns interest |

| Taxes | Deferred on accumulated earnings |

| Risk | As cash value increases, insurance company's risk decreases |

Explore related products

What You'll Learn

![]()

How does cash value life insurance work?

Cash value life insurance is a form of permanent life insurance that features a cash value savings component. This means that the policyholder can borrow or withdraw cash from the policy, or use it to pay premiums. The cash value of life insurance earns interest, and taxes are deferred on the accumulated earnings. This means that the cash value builds over time.

Cash value life insurance is more expensive than term life insurance, but unlike term life insurance, cash value insurance policies don't expire after a specific number of years. Whole life, variable life, and universal life insurance are all examples of cash value life insurance.

The cash value can be used for many purposes, including borrowing or withdrawing cash, or using it to pay policy premiums. The policyholder can typically access this cash value before the policy ends. For example, they could take out a loan to pay for other life expenses.

The two main components that make up a life insurance policy are the death benefit and the cash value. The death benefit is the part of the plan that the beneficiaries receive. You can predetermine what you would like this face value to be upfront.

Get Life Insurance for Your Boyfriend: A Step-by-Step Guide

You may want to see also

Explore related products

$15.95

$2.99 $12.95

$8.99

![]()

What are the benefits of cash value life insurance?

Cash value life insurance is a form of permanent life insurance that features a cash value savings component. This means that the policyholder can use the cash value for many purposes, including borrowing or withdrawing cash from it, or using it to pay policy premiums.

The cash value of life insurance earns interest, and taxes are deferred on the accumulated earnings. While premiums are paid and interest accrues, the cash value builds over time. As the life insurance cash value increases, the insurance company’s risk decreases, because the accumulated cash value offsets part of the insurer’s liability.

Cash value life insurance is more expensive than term life insurance. However, unlike term life insurance, cash value insurance policies don't expire after a specific number of years. You may borrow against a cash value life insurance policy.

Cash value can function in a variety of permanent plans, including whole, universal, variable, and indexed life insurance. The two main components that make up a life insurance policy are the death benefit and the cash value. The death benefit is the part of the plan that the beneficiaries receive later on. You can predetermine what you would like this face value to be upfront.

Life Insurance Proceeds: When to Declare and Why

You may want to see also

Explore related products

![]()

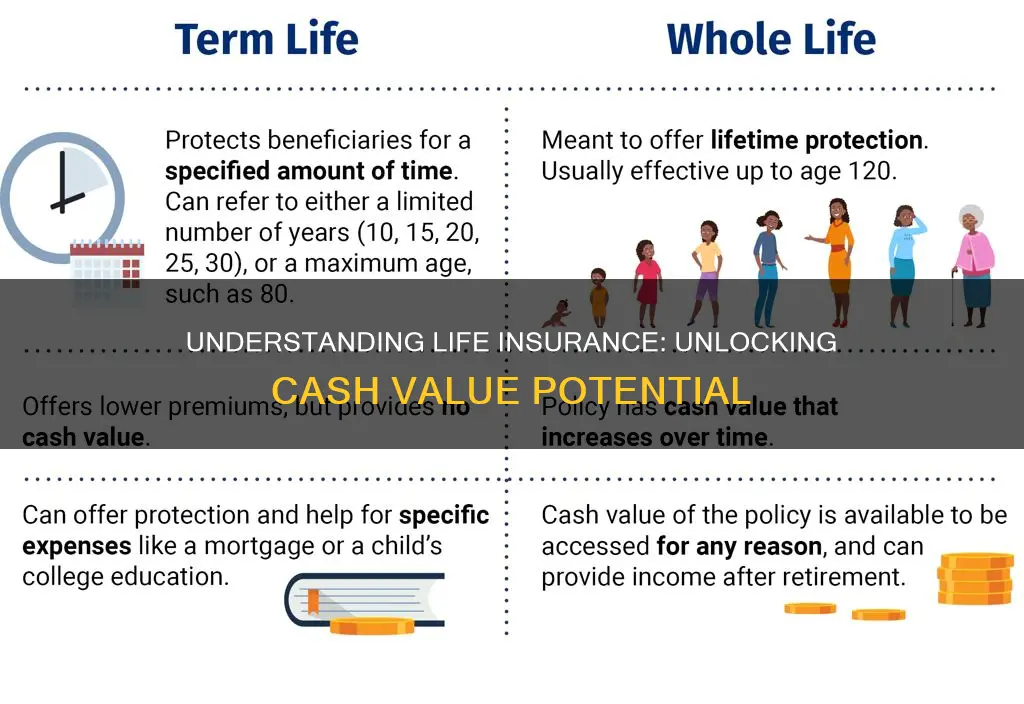

How does cash value life insurance compare to term life insurance?

Cash value life insurance is a form of permanent life insurance that features a cash value savings component. This means that the policyholder can use the cash value for many purposes, including borrowing or withdrawing cash from it, or using it to pay policy premiums. Cash value life insurance is more expensive than term life insurance, but unlike term life insurance, cash value insurance policies don't expire after a specific number of years.

Cash value life insurance policies can accumulate cash value over time. Whole life, variable life, and universal life insurance are all examples of cash value life insurance. The cash value of life insurance earns interest, and taxes are deferred on the accumulated earnings. While premiums are paid and interest accrues, the cash value builds over time. As the life insurance cash value increases, the insurance company’s risk decreases, because the accumulated cash value offsets part of the insurer’s liability.

Term life insurance, on the other hand, is a type of insurance that covers the policyholder for a specific period of time, usually between 10 and 30 years. During this time, the policyholder pays a fixed premium, and their beneficiaries will receive a death benefit if the policyholder dies within the policy term. However, term life insurance does not have a cash value component, and the policy does not accumulate any cash value over time.

When comparing cash value life insurance to term life insurance, it's important to consider the needs and financial goals of the individual. Cash value life insurance can be a good option for those who want lifelong coverage and the ability to access cash value during their lifetime. It can also provide additional financial protection for loved ones, as the death benefit is typically higher than the accumulated cash value. However, term life insurance may be more suitable for those who only need coverage for a specific period, such as during their working years or when they have young children. Term life insurance is generally more affordable than cash value life insurance, making it a cost-effective option for those on a budget. Ultimately, the decision between cash value and term life insurance depends on individual circumstances and financial priorities.

Term Life Insurance Lapse: What Happens and What to Do?

You may want to see also

Explore related products

![]()

What are the different types of cash value life insurance?

Cash value life insurance is a form of permanent life insurance that features a cash value savings component. The policyholder can use the cash value for many purposes, including borrowing or withdrawing cash from it, or using it to pay policy premiums. Cash value life insurance is more expensive than term life insurance, but unlike term life insurance, cash value insurance policies don't expire after a specific number of years.

There are several different types of cash value life insurance, including:

- Whole life insurance: This is a type of permanent life insurance that can build funds over time through the cash value component. Whole life insurance policies typically have a fixed premium and a guaranteed death benefit.

- Universal life insurance: This type of policy offers flexible premiums and death benefits, and the cash value earns interest.

- Variable life insurance: This type of policy invests the cash value in stocks, bonds, or other investment options, which can lead to higher returns but also carries more risk.

- Indexed life insurance: This type of policy ties the cash value to a stock market index, such as the S&P 500, and the returns are based on the performance of the index.

Power of Attorney: Can They Cash in Life Insurance?

You may want to see also

Explore related products

![]()

How does cash value life insurance protect your loved ones?

Cash value life insurance, also known as permanent life insurance, includes a cash component in addition to a death benefit. This cash value can be used for many purposes, including borrowing or withdrawing cash, or using it to pay policy premiums. The cash value can also be used to protect your loved ones from financial strain in the event of your death.

Permanent life insurance policies such as whole life, variable life, and universal life can accumulate cash value over time. This cash value earns interest, and taxes are deferred on the accumulated earnings. As the life insurance cash value increases, the insurance company’s risk decreases, because the accumulated cash value offsets part of the insurer’s liability.

For example, consider a policy with a $25,000 death benefit. The policy has no outstanding loans or prior cash withdrawals and an accumulated cash value of $5,000. Upon the death of the policyholder, the insurance company pays the full death benefit of $25,000. The money accumulated in the cash value becomes the property of the insurer, reducing their liability.

The cash value of life insurance can be a valuable tool to protect your loved ones financially. It can provide them with the funds they need to cover expenses and maintain their standard of living in the event of your death. Additionally, the cash value can be accessed before the policy ends, providing flexibility and financial support during the policyholder's lifetime.

Prospecting for Life Insurance: Strategies for Success

You may want to see also

Frequently asked questions

Cash value life insurance is a form of permanent life insurance that features a cash value savings component. The policyholder can use the cash value for many purposes, including borrowing or withdrawing cash from it, or using it to pay policy premiums.

Cash value life insurance, also known as permanent life insurance, includes a cash component in addition to a death benefit. The cash value can be used for many purposes, including borrowing or withdrawing cash, or using it to pay policy premiums.

Cash value life insurance offers several benefits, including the ability to build funds over time, access to cash value before the policy ends, and the potential to accumulate cash value over time.

Cash value life insurance is more expensive than term life insurance, and it doesn't expire after a specific number of years. Unlike term life insurance, you may borrow against a cash value life insurance policy.

Whole life, variable life, and universal life insurance are all examples of cash value life insurance. Cash value can also function in permanent plans, including whole, universal, variable, and indexed life insurance.