There is a correlation between auto insurance and credit score. In most states, car insurance companies use credit-based insurance scores, which means your credit score can impact your car insurance premium. In general, drivers with excellent credit pay the lowest rates, whereas drivers with poor credit pay the highest rates. A higher credit score decreases your car insurance rate with almost every insurance company and in most states. However, it's important to note that this practice is controversial and banned in some states, including California, Hawaii, Massachusetts, and Michigan.

| Characteristics | Values |

|---|---|

| Credit score impact on auto insurance | In most states, auto insurance companies use credit-based insurance scores, which means your credit score can impact your auto insurance premium. |

| Credit score range | Credit scores range from 300 to 850. |

| Credit score tiers | Excellent, good, average, poor |

| Credit score impact on insurance premium | Drivers with poor credit pay higher insurance premiums compared to those with good credit. |

| Credit-based insurance score | Auto insurance providers use a credit-based insurance score to reflect the likelihood of making a claim. |

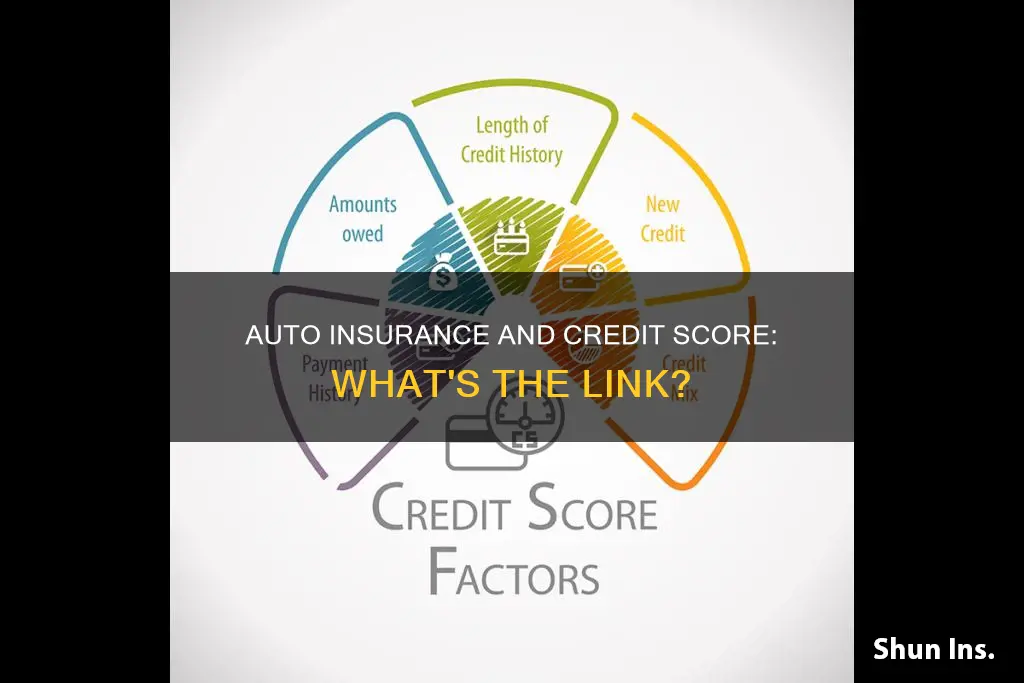

| Factors considered for credit-based insurance score | Payment history, outstanding debt, credit history length, pursuit of new credit, credit mix |

| Credit score impact on insurance score | A higher credit score generally leads to a higher insurance score. |

| Insurance credit score range | LexisNexis offers credit-based insurance scores through Experian, ranging from 200 to 997. |

| Good insurance credit score | A good insurance credit score is typically considered to be 750 or above, but it may vary across companies. |

| Poor insurance credit score | A poor insurance credit score is typically considered to be 625 or below, but it may vary across companies. |

| Average insurance rates for poor credit | $3,455 per year for full coverage and $1,118 per year for minimum coverage. |

| Average insurance rates for good credit and driving record | $2,148 per year for full coverage and $685 per year for minimum coverage. |

| States prohibiting credit-based insurance scores | California, Hawaii, Massachusetts, Michigan |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

![]()

How credit-based insurance scores are calculated

Credit-based insurance scores are calculated using several factors, including:

- Payment history: How well you have made payments on your outstanding debt in the past. This is the most important factor, making up 40% of your credit-based insurance score.

- Outstanding debt: The amount of debt you currently have. This is the second most important factor, accounting for 30% of your score.

- Length of credit history: How long you have had an open line of credit. This factor makes up 15% of your score.

- Pursuit of new credit: Whether you have recently applied for new lines of credit. This accounts for 10% of your score.

- Credit mix: The different types of credit you have, such as credit cards, mortgage loans, and auto loans. This is the least important factor, making up only 5% of your score.

It's important to note that a credit-based insurance score is not the same as a typical credit score, like a FICO score. While they consider similar factors, they weigh them differently. A credit-based insurance score specifically measures how risky you are from an auto insurance claim perspective, based on your creditworthiness.

U.S. Auto Insurance: Adding a Driver Made Easy

You may want to see also

Explore related products

![]()

How credit scores impact insurance premiums by state

In most states, insurance companies can use credit-based insurance scores to determine your premiums. These scores are different from typical credit scores and are based on consumer credit data. While the impact of a credit record on insurance premiums varies across states, the practice is banned in California, Hawaii, Massachusetts, and Michigan.

Here's how credit scores impact insurance premiums in different states:

California, Hawaii, Massachusetts, and Michigan

In these states, the use of credit-based insurance scores to set car insurance rates is prohibited or limited. Instead, insurance companies base rates on factors such as driving records, location, and other characteristics. As a result, credit scores have no impact on insurance premiums in these states.

Washington, D.C.

Poor credit significantly raises insurance rates in Washington, D.C., with rates being two and a half times higher than average for drivers with poor credit.

New York

Drivers with poor credit in New York pay one of the highest average rates for full coverage car insurance, at $7,625 per year.

New Jersey, Texas, and Florida

These states are among those where poor credit more than doubles insurance rates.

Vermont

A 2016 study by the Vermont Department of Financial Regulation found that about 66% of policyholders had lower car insurance rates when credit scoring was used in pricing. Conversely, 16% of policyholders had higher rates, and 18% saw no difference.

Arkansas

A 2017 study by the Arkansas Insurance Department found that about 57% of policyholders saw a decrease in their car insurance premiums when credit scoring was used, while 23% saw an increase, and 19% saw no change.

Oregon

Oregon has some restrictions on the use of credit-based insurance scores for car insurance. Insurers cannot use credit to raise premiums at policy renewal or cancel/refuse to renew a policy due to credit history problems. However, there is a proposed bill to prohibit the use of credit in determining rates.

Other States

In most other states, credit scores can impact insurance premiums, with drivers with poor credit paying significantly higher rates than those with good credit. The impact varies depending on the insurance company and the state, with rates for full coverage policies differing by credit tier.

Auto Insurance for Minors in Rhode Island

You may want to see also

Explore related products

![]()

Why insurance providers use credit scores

Credit scores are a key factor in determining auto insurance rates. While it is not the sole determinant, it is an important consideration for insurance providers when assessing the risk of insuring an individual and their vehicle. Here are several reasons why insurance providers use credit scores:

To Assess Risk and Probability of Claims:

Insurance providers use credit scores as a tool to evaluate the likelihood of an individual filing an insurance claim. A credit-based insurance score is calculated to predict the probability of a person making a claim and costing the insurance company money. A lower credit score may indicate a higher risk of filing claims, which could lead to higher insurance premiums.

To Determine Insurance Rates:

Credit-based insurance scores help insurance providers set insurance rates accordingly. Individuals with higher credit scores are often offered lower insurance rates, while those with poor credit scores may face higher premiums. This pricing structure incentivizes customers who are less likely to file claims and rewards them with preferential rates.

To Evaluate Financial Responsibility:

Credit scores provide insurance providers with insights into an individual's financial behaviour and responsibility. Factors such as payment history, credit utilization, and debt management are considered when calculating credit-based insurance scores. These factors can indicate an individual's ability to manage their finances effectively, which may extend to their approach to vehicle maintenance, safety, and insurance claims.

To Make Informed Underwriting Decisions:

Credit-based insurance scores are used in conjunction with other factors, such as driving history, vehicle information, and personal details, to make comprehensive underwriting decisions. By considering credit scores, insurance providers can assess the overall risk profile of a potential customer and determine whether to offer coverage and at what rate.

To Identify Potential High-Risk Customers:

Insurance providers aim to identify customers who may pose a higher risk of filing frequent or costly claims. While credit scores are not a perfect predictor of accident risk, they can provide a data-driven approach to assessing an individual's overall risk profile. This information helps insurance providers make informed decisions about coverage and pricing.

It is important to note that the use of credit scores in auto insurance is not without controversy. Some states, such as California, Hawaii, Michigan, and Massachusetts, have prohibited or limited the use of credit scores in determining insurance rates. Additionally, insurance providers should not rely solely on credit scores but consider other relevant factors to ensure a comprehensive evaluation of each customer's risk profile.

Can Do Auto Insurance: Boise, Idaho's Best

You may want to see also

Explore related products

![]()

What constitutes a bad credit score

A bad credit score can be defined as a FICO score below 580 or a VantageScore below 600. FICO (Fair Isaac Corporation) is the most widely used scoring model, with scores ranging from 300 to 850. A score of 300-579 is considered poor, while 580-669 is deemed fair.

VantageScore, on the other hand, is another scoring model that uses the same 300-850 range but with slightly different categorisations. A VantageScore of 300-499 is considered very poor, 500-600 is poor, and 601-660 is fair.

The impact of a bad credit score can be far-reaching. It can lead to higher interest rates and more restrictive terms on loans and credit cards. Additionally, it may result in higher insurance premiums, as home and auto insurance carriers in most states are permitted to consider credit scores in their risk analysis. A bad credit score can also make renting an apartment more challenging, as landlords often conduct background checks that include credit information. In some cases, it could even impact career opportunities, as employers in certain states can legally review credit reports when making hiring decisions.

To summarise, a bad credit score generally falls within the poor or very poor categories of the FICO or VantageScore models. The specific thresholds for these categories differ slightly between the two scoring models.

Driver's License and Auto Insurance: What's the Connection?

You may want to see also

Explore related products

![]()

How to improve your credit score

Improving your credit score can take time and consistency, but there are several strategies you can employ to achieve this. Here are some ways to enhance your credit score:

- Pay your bills on time: Making timely payments is crucial for improving your credit score. Late payments can stay on your credit report for up to seven years and have a negative impact. Set up autopay or calendar reminders to ensure you never miss a due date.

- Keep credit card balances low: Aim to use less than 30% of your credit limit on any card, as the credit utilization rate is a significant factor in calculating your score. Consider paying off credit card debt through various strategies such as debt consolidation loans or balance transfer credit cards.

- Don't close your oldest credit account: The length of your credit history matters and accounts for 15% of your FICO score. Keeping your oldest account open, even if you don't use it often, can help maintain a longer credit history.

- Diversify your credit mix: Having different types of credit, such as credit cards, loans, and mortgages, can strengthen your credit profile. However, avoid taking on unnecessary debt just for the sake of building credit.

- Limit hard credit inquiries: When applying for new credit, multiple hard inquiries in a short period can negatively impact your score. Only apply for credit when necessary, and consider prequalification options that use soft credit checks instead.

- Dispute inaccurate information: Errors on your credit report can pull down your score. Regularly review your reports from the three major credit bureaus (Equifax, Experian, and TransUnion) and dispute any inaccuracies.

- Become an authorized user: If you have a relative or friend with a good credit history, you can ask to be added as an authorized user on their credit card. This can help improve your score, especially if you're new to credit.

- Monitor your score and credit reports regularly: Keeping track of your credit score and reports can help you identify areas for improvement and spot any signs of identity theft or errors.

- Be mindful of your credit utilization ratio: This ratio measures how much of your available credit you're using. Aim to keep your utilization below 30% by paying off debt or increasing your credit limits.

Auto Insurance in California: Easy or Difficult?

You may want to see also

Frequently asked questions

In most states, auto insurance companies use credit-based insurance scores, meaning your credit score can impact your auto insurance premium. Generally, drivers with excellent credit pay lower rates, while drivers with poor credit pay higher rates.

Your credit score is one of many factors that determine your auto insurance premium. A higher credit score can lead to lower insurance rates, while a lower credit score can result in higher rates.

No, auto insurance providers use a credit-based insurance score, which is different from the typical FICO credit score used by lenders. This score reflects the likelihood of filing an insurance claim and helps determine insurance rates.

Insurance providers use credit-based scores to assess the risk of insuring you and your vehicle. A low score may indicate a higher risk of filing insurance claims, potentially costing the insurer more money.

Improving your credit score involves demonstrating financial responsibility. This can be achieved by paying your bills on time, reducing credit card debt, and maintaining a low credit utilization ratio. Monitoring your credit report for errors and disputes can also help maintain a good score.