Medicare is a federal health insurance program for individuals aged 65 and older, as well as certain individuals under 65 with disabilities or specific conditions. There are several parts to Medicare, including Part A (Hospital Insurance), Part B (Medical Insurance), and Part C (Medicare Advantage). Supplemental insurance, or Medigap, is extra insurance purchased from a private company to help cover costs not covered by Original Medicare (Parts A and B). While Part C is an alternative to Original Medicare, providing bundled coverage, Medigap serves as a supplement to Original Medicare and cannot be used with Part C.

| Characteristics | Values |

|---|---|

| Type | Part C is Medicare Advantage, an alternative to Parts A and B. Supplemental insurance is also known as Medigap, which is an addition to Original Medicare. |

| Coverage | Part C includes Parts A, B, and usually D. Supplemental insurance does not include drug coverage, but you can join a separate Medicare drug plan (Part D). |

| Cost | Part C may have different out-of-pocket costs than Original Medicare. Supplemental insurance helps pay your share of costs in Original Medicare. |

| Availability | You must have Parts A and B to join Part C. You must have Original Medicare (Parts A and B) to buy a supplemental insurance policy. |

| Provider | Part C is run by private companies. Supplemental insurance is provided by private companies. |

| Choice of healthcare provider | Part C may restrict you to doctors within the plan's network. Supplemental insurance allows you to see any doctor or hospital that accepts Medicare. |

Explore related products

What You'll Learn

![]()

Medicare Part C is also known as Medicare Advantage

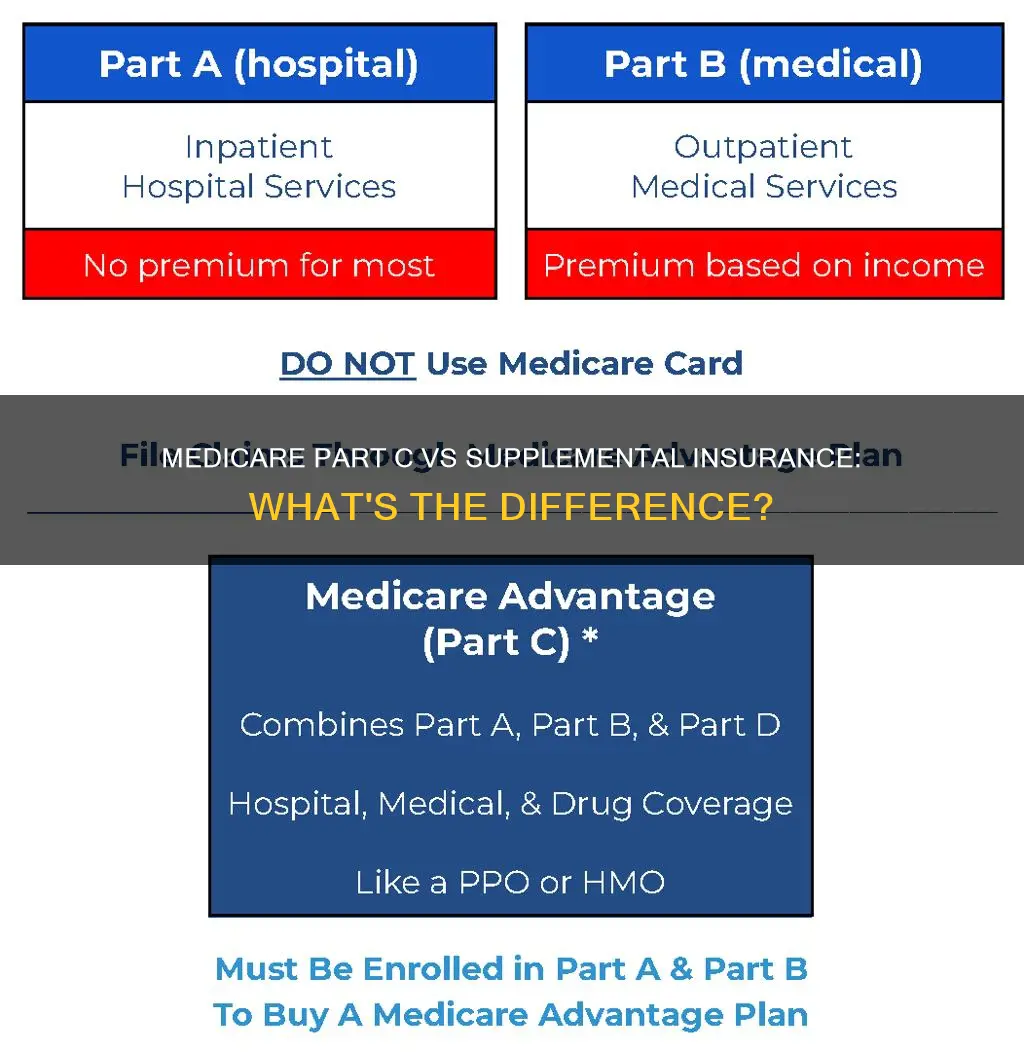

Medicare Part C, also known as Medicare Advantage, is one of the two main ways to get your Medicare coverage. The other is Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). Medicare Advantage is a Medicare-approved plan from a private company that offers an alternative to Original Medicare for your health and drug coverage. It is important to note that you must have both Part A and Part B to join a Medicare Advantage Plan.

Medicare Advantage plans bundle several coverage types, including Parts A, B, and usually Part D. Part D helps cover prescription drug costs. Most Medicare Advantage Plans include Part D coverage, and in most types of Medicare Advantage Plans, you cannot join a separate Medicare drug plan.

Medicare Advantage plans may have different rules from Original Medicare, but they must provide at least the same level of coverage. For example, if you use an insulin pump that is covered under Part B's durable medical equipment benefit, or you get your covered insulin through a Medicare Advantage Plan, your cost for a month's supply of Part B-covered insulin for your pump cannot be more than $35.

Medicare Supplement Insurance (Medigap) is extra insurance that you can buy from a private company to help pay your share of costs in Original Medicare. Medigap policies are standardized, and in most states, they are named by letters, like Plan G or Plan K. The benefits in each lettered plan are the same, regardless of the insurance company. Generally, you need to have Original Medicare (Part A and Part B) to buy a Medigap policy. It is important to note that Medigap is different from Medicare Advantage, and you cannot have both at the same time.

Eye Doctors: Insurance Specialists?

You may want to see also

Explore related products

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UY218_.jpg)

![]()

Medicare Advantage is an alternative to Original Medicare

Medicare Advantage, also known as Part C, is an alternative to Original Medicare. Original Medicare includes Part A (Hospital Insurance) and Part B (Medical Insurance). Once you have signed up for Parts A and B, you can choose to stick with Original Medicare or switch to Medicare Advantage. Medicare Advantage is a Medicare-approved plan from a private company that offers an alternative to Original Medicare for health and drug coverage.

Medicare Advantage plans have become increasingly popular. In 2024, nearly 33 million people were enrolled in a Medicare Advantage plan. Medicare Advantage plans have certain benefits that Original Medicare does not cover, such as vision, hearing, and dental services. Medicare Advantage may also have lower premiums than Original Medicare, but there may be other cost differences. Additionally, Medicare Advantage plans have geographic limits, whereas Original Medicare can be used anywhere in the US.

Medicare Advantage plans may have different rules than Original Medicare, but they must provide at least the same level of coverage. For example, if you use an insulin pump that is covered under Part B's durable medical equipment benefit, your cost for a month's supply of insulin for your pump cannot be more than $35, regardless of whether you have Original Medicare or a Medicare Advantage plan.

Medicare Supplement Insurance, or Medigap, is extra insurance that can be purchased from a private company to help pay your share of costs in Original Medicare. Medigap policies are standardized and named by letters, like Plan G or Plan K. The benefits in each lettered plan are the same, regardless of the insurance company. Medigap policies generally do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Additional Insured: Protecting Clients and Professional Services

You may want to see also

Explore related products

![]()

Medigap is supplemental insurance

Medicare Supplement Insurance, also known as Medigap, is extra insurance that helps pay your share of costs in Original Medicare. Medigap policies are standardized, and in most states, they are named by letters, like Plan G or Plan K. The benefits in each lettered plan are the same, no matter which insurance company sells it. The price is the only difference between policies with the same letter sold by different companies. Generally, you need to have signed up for Part A (Hospital Insurance) and Part B (Medical Insurance) to buy a Medigap policy.

Medigap policies do not cover long-term care (like care in a nursing home), vision, dental, hearing aids, private-duty nursing, or prescription drugs. However, some Medigap policies offer coverage when you travel outside the U.S. You must buy a Medigap policy within 6 months of when you first get Part A and Part B; otherwise, you may not be able to buy a policy or you may pay more.

The best time to enroll in a Medigap plan is during your Medigap Open Enrollment Period, which starts on the first day of the month in which you turn 65 and are enrolled in Medicare Part B. During this period, you have guaranteed issue rights, meaning that insurance companies cannot deny you coverage or charge you higher premiums based on pre-existing conditions.

The Intricacies of Reciprocal Insurance: Unraveling the Unique Concept in the Industry

You may want to see also

Explore related products

![]()

Supplemental insurance helps pay your share of costs

Medicare is federal health insurance for anyone aged 65 and over, as well as some people under 65 with certain disabilities or conditions. There are different parts to Medicare, and you can choose which way you get your health coverage.

Original Medicare includes Part A (Hospital Insurance) and Part B (Medical Insurance). You can also join a separate Medicare drug plan to get Medicare drug coverage (Part D). You can use any doctor or hospital that accepts Medicare, anywhere in the US.

Medicare Advantage (Part C) is a Medicare-approved plan from a private company that offers an alternative to Original Medicare for health and drug coverage. In many cases, you can only use doctors who are in the plan's network. Most Medicare Advantage Plans include Part D coverage.

Supplemental insurance (Medigap) is extra insurance you can buy from a private company that helps pay your share of costs in Original Medicare. Generally, you need Part A and Part B to buy a Medigap policy. Supplemental insurance helps pay your share of costs by covering what is known as your out-of-pocket costs, such as your 20% coinsurance. Supplemental insurance companies will pay your doctor whatever amount you owe under your policy, and you are responsible for any costs that are left. Some Medigap policies offer coverage when you travel outside the US. Generally, Medigap policies don't cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Naming Additional Insureds: A Quick Guide

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

You can't have Medigap and Medicare Advantage at the same time

Medicare is federal health insurance for individuals aged 65 and older, as well as some people under 65 with certain disabilities or conditions. There are two main ways to get Medicare coverage: Original Medicare and Medicare Advantage.

Original Medicare includes Part A (Hospital Insurance) and Part B (Medical Insurance). You can also join a separate Medicare drug plan (Part D) to get prescription drug coverage. With Original Medicare, you can see any doctor or hospital that accepts Medicare anywhere in the US.

Medicare Advantage, also known as Part C, is an alternative to Original Medicare. It is offered by private health insurers and includes the same coverage as Part A and Part B. Many Medicare Advantage Plans also include Part D coverage and may offer additional benefits such as dental, vision, and hearing coverage. With Medicare Advantage, you may be required to use doctors within the plan's network and may need a referral from your primary care provider to see a specialist, resulting in additional time and expenses.

Medigap, or Medicare Supplement Insurance, is extra insurance sold by private companies that fills the "gaps" in Original Medicare. It helps cover some of the out-of-pocket expenses that Original Medicare does not cover, such as deductibles and copays. Medigap policies are standardized, and you must have both Part A and Part B to purchase a Medigap policy.

While both Medicare Advantage and Medigap can help fill coverage gaps and control out-of-pocket costs, you cannot have both at the same time. If you drop a Medigap policy to join Medicare Advantage, you have a one-time opportunity to switch back to Medigap within 12 months if you return to Original Medicare.

Unraveling the Insurance Angle in 340B: Understanding the Intersection

You may want to see also

Frequently asked questions

Part C, also known as Medicare Advantage, is one of the two main ways to get your Medicare coverage. It is run by private companies and approved by the federal government.

Medicare Supplemental Insurance, or Medigap, is extra insurance that helps pay your share of costs in Original Medicare. It is also provided by private companies.

Generally, yes. You need to have both Part A and Part B to buy a Medigap policy.

Some Medigap policies offer coverage when you travel outside the U.S. and may also cover your deductible. However, they generally do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Part C is one of the main ways to get your Medicare coverage, while Supplemental Insurance is extra insurance that can help pay for costs not covered by Original Medicare.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)