Flood insurance is a crucial consideration for homeowners, as flooding can occur in various locations and cause significant financial losses. The National Flood Insurance Program (NFIP), managed by FEMA, offers flood insurance to property owners, renters, and businesses. This insurance covers the cost of rebuilding and repairing damage caused by flooding, which is typically excluded from standard homeowners insurance policies. To determine flood risk, individuals can refer to flood maps and risk assessments provided by FEMA, which indicate the likelihood of flooding in specific areas. These tools help communities understand their vulnerability to flooding and make informed decisions about insurance requirements and risk reduction strategies. While flood insurance is mandatory for properties in high-risk flood zones with government-backed mortgages, it is recommended for all homeowners to protect against potential financial devastation caused by flooding.

| Characteristics | Values |

|---|---|

| Flood insurance provider | National Flood Insurance Program (NFIP) |

| Administered by | FEMA |

| Participating communities | 22,600 |

| Insurance companies | More than 47 |

| Policyholders | 4.7 million |

| Coverage | Nearly $1.3 trillion |

| Flood maps | Show flood risk, flood zone, floodplain boundaries, and base flood elevation |

| Flood risk | Depends on ground elevation, proximity to water sources, drainage, and construction projects |

| High-risk areas | 1% or higher chance of flooding each year; 1 in 4 chance during a 30-year mortgage |

| Mandatory insurance | For high-risk areas with government-backed mortgages |

| Average claim payment | $68,000 |

| Waiting period | Typically 30 days |

| Coverage | Building coverage, contents coverage, and flood avoidance measures |

| Quote | Available through the NFIP Quote Tool |

Explore related products

What You'll Learn

- Flood insurance is mandatory for properties in high-risk zones with government-backed mortgages

- Flood maps help determine insurance requirements and community flood risk

- Flood insurance covers losses directly caused by flooding

- Flood risk mitigation can lower insurance costs

- The National Flood Insurance Program (NFIP) provides flood insurance to property owners, renters and businesses

![]()

Flood insurance is mandatory for properties in high-risk zones with government-backed mortgages

Flood insurance is a crucial consideration for homeowners, especially in areas prone to flooding. While floods can occur almost anywhere and are largely unpredictable, certain zones are deemed high-risk due to their proximity to bodies of water or other factors like heavy rainfall and drainage issues. For properties located in these high-risk flood zones, purchasing flood insurance is not just a wise precaution but, in some cases, a mandatory requirement.

When it comes to determining whether flood insurance is mandatory, the type of mortgage on the property plays a significant role. If a property is located in a high-risk flood zone and has a mortgage backed by a federal agency or the government, flood insurance becomes a requirement. This is because lenders of federally-backed or government-insured mortgages are mandated by Congress to enforce flood insurance for these properties to mitigate the financial risks associated with flooding.

FEMA's National Flood Insurance Program (NFIP) is a key player in this context. The NFIP provides flood insurance to property owners, renters, and businesses, aiding in their recovery after flood events. FEMA also maintains flood maps, which are essential tools for communities and mortgage lenders to assess flood risk. These maps help lenders determine insurance requirements, and communities can use them to develop strategies to reduce their vulnerability to flooding.

It's important to note that not all properties in high-risk zones will require flood insurance. If a property is purchased without a mortgage or with a private lender that doesn't require flood insurance, it may not be mandatory. However, even in these cases, it's highly recommended to consider flood insurance due to the significant financial losses that can occur from flood damage. Most homeowners' insurance policies do not cover flood damage, leaving property owners vulnerable without specialized flood insurance.

To summarize, flood insurance is mandatory for properties in high-risk zones with government-backed mortgages to protect both lenders and homeowners from the financial repercussions of flooding events. For those in high-risk areas without government-backed mortgages, flood insurance is still strongly advised due to the limited coverage provided by standard homeowners' insurance policies. By understanding their flood risk and taking appropriate precautions, homeowners can safeguard their finances and gain peace of mind.

National General Auto Insurance: Is It Worth the Hype?

You may want to see also

Explore related products

![]()

Flood maps help determine insurance requirements and community flood risk

Flood maps are a tool that communities use to determine which areas are at the highest risk of flooding. They are maintained and updated by FEMA through flood maps and risk assessments. Flood maps are useful in showing how likely an area is to flood. Places with a 1% or higher chance of flooding each year are considered high-risk areas. These areas have at least a one-in-four chance of flooding during a 30-year mortgage. Flood maps are also used by citizens, governments, insurance agents, and banks to determine whether flood insurance is required.

In communities that participate in the National Flood Insurance Program (NFIP), flood insurance is mandatory for properties located in high-risk flood zones if mortgages are government-backed. Flood insurance is not federally mandated in moderate-to-low-risk areas, but it is advised for all property owners and renters. Over a 30-year mortgage, homes in high-risk areas have a 1 in 4 chance of flooding at least once. There is still a risk of flooding in areas with low or moderate flood risk. About 40% of NFIP claims come from outside high-risk flood areas. Although some lenders may not require flood insurance, FEMA recommends flood insurance to protect property owners from financial losses.

FEMA provides technology and works with community leaders to make the maps as accurate as possible. Community members are also invited to provide information to help local officials better understand how water drains in the area. The FEMA Flood Map Service Center (MSC) is the official online location to find all flood hazard mapping products created under the National Flood Insurance Program, including your community's flood map.

The mapping process helps communities understand their flood risk and make more informed decisions about how to reduce or manage their risk. Flood maps can be used to determine insurance requirements and help communities develop strategies for reducing their risk. Flood maps are an important tool for communities to understand their flood risk and make informed decisions about reducing or managing their risk.

Florida Commercial Auto Insurance: Cost and Coverage

You may want to see also

Explore related products

![]()

Flood insurance covers losses directly caused by flooding

Flood insurance is a separate policy from homeowners' or renters' insurance and is managed by FEMA through the National Flood Insurance Program (NFIP). It is delivered to the public by a network of more than 50 insurance companies and the NFIP Direct. Flood insurance covers losses directly caused by flooding, including damage to your home and belongings, and helps you recover faster when the floodwaters recede.

The NFIP provides flood insurance to property owners, renters, and businesses. Building coverage includes electrical and plumbing systems, furnaces and water heaters, refrigerators, stoves, and built-in appliances. Belongings coverage, or contents coverage, includes clothing, furniture, electronic equipment, washers and dryers, portable and window air conditioners, and valuable items such as original artwork and furs (up to $2,500).

It's important to note that flood insurance policies are unique to your location and needs. The NFIP offers coverage options to protect your home, belongings, or business from floods, and policy rates will depend on factors such as where you live, the type of house you have, its age, and how it's built and arranged. Flood maps are used to determine the risk of flooding in a particular area, and communities that participate in the NFIP are required to adopt and enforce floodplain management regulations to help mitigate flooding effects.

To purchase flood insurance, you can contact an insurance agent or company, or visit the NFIP website to find an insurance provider and get a quote. It's recommended to plan ahead, as there is typically a 30-day waiting period for an NFIP policy to go into effect, unless coverage is mandated by a government-backed lender or is related to a community flood map change.

U.S. Auto Association: Understanding Auto Repair Coverage

You may want to see also

Explore related products

![]()

Flood risk mitigation can lower insurance costs

Flooding can occur almost anywhere, even in areas that are not near a body of water. Flood maps can help communities understand their risk and take actions to protect their families, homes, and businesses. FEMA maintains and updates flood map data and risk assessments. Any place with a 1% chance or higher chance of experiencing a flood each year is considered to have a high risk of flooding. In communities that participate in the National Flood Insurance Program (NFIP), flood insurance is mandatory for properties located in high-risk flood zones if mortgages are government-backed.

The NFIP provides flood insurance to property owners, renters, and businesses, helping them recover faster when floodwaters recede. The first step towards buying a policy is to get a quote using the NFIP Quote Tool. FEMA administers the NFIP, and over 47 private insurance companies participate in the Write-Your-Own (WYO) program, selling and servicing NFIP policies through their insurance agents.

Increased Cost of Compliance (ICC) coverage is another way to lower insurance costs. ICC coverage provides funding to help rebuild a home to meet safety standards and local flood safety rules. If a building has been substantially or repeatedly damaged by floods, policyholders may receive up to $30,000 to make changes that lower the risk of future flood damage. Communities can also participate in the Community Rating System (CRS), a voluntary incentive program that recognizes communities for implementing floodplain management practices. In exchange for proactive efforts to reduce flood risk, policyholders can receive discounted flood insurance premiums of up to 45%.

Applying for New Jersey Manufacturer Auto Insurance

You may want to see also

Explore related products

![]()

The National Flood Insurance Program (NFIP) provides flood insurance to property owners, renters and businesses

The National Flood Insurance Program (NFIP) is a program created by the Congress of the United States in 1968 through the National Flood Insurance Act of 1968. It is managed by the Federal Emergency Management Agency (FEMA) and delivered to the public by a network of more than 47 insurance companies and the NFIP Direct. The NFIP is the nation's largest single-line insurance program, providing nearly $1.3 trillion in coverage against floods. It offers flood insurance to property owners, renters, and businesses in the 22,600 participating NFIP communities.

Flood insurance is a separate policy from homeowners insurance and is specific to flooding. Most homeowners insurance does not cover flood damage, and flooding is the most common and costly natural disaster, with 90% of presidentially declared US natural disasters involving flooding. Flooding can be caused by poor drainage systems, summer storms, melting snow, neighborhood construction, or broken water mains, and it can happen anywhere it rains or snows. Even one inch of floodwater can cause thousands of dollars' worth of damage.

The NFIP offers two types of coverage: building coverage and contents coverage. Building coverage protects against direct physical losses to the structure of a building, while contents coverage protects against direct physical losses to belongings within a building. The cost of coverage depends on various factors, including the location of the property, the type of house, its age, and its construction.

In addition to providing insurance, the NFIP also works with communities to adopt and enforce floodplain management regulations that help mitigate flooding effects. The program has two main purposes: to share the risk of flood losses through flood insurance and to reduce flood damages by restricting floodplain development. The NFIP requires communities to adopt adequate land use and control measures to reduce flood damage and restrict development in areas exposed to flooding.

Unregistered Vehicles: SR22 Insurance Options

You may want to see also

Frequently asked questions

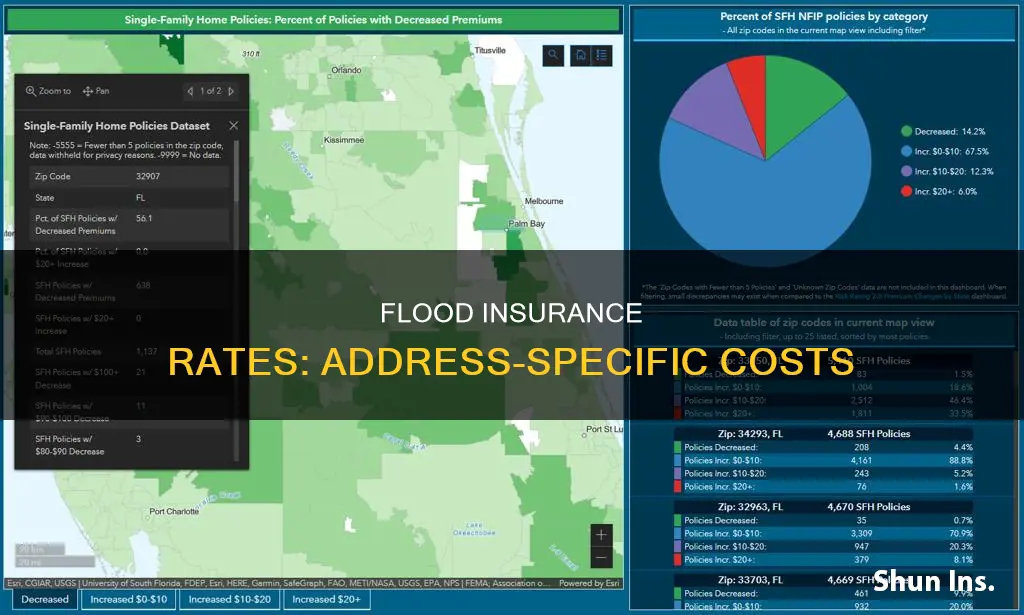

The flood insurance rate for your address will depend on your flood risk level. You can find out your flood risk level by using the flood risk tool on the National Flood Insurance Program (NFIP) website.

Flood risk levels are determined by flood maps, which show a community's flood zone, floodplain boundaries, and base flood elevation. FEMA maintains and updates data through these flood maps and risk assessments.

If your property is in a high-risk flood zone and you have a government-backed mortgage, you must purchase flood insurance. However, FEMA recommends that everyone get flood insurance to protect against financial losses, as flooding can occur anywhere.