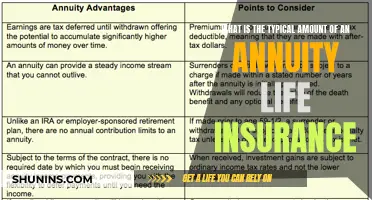

Life insurance can be a valuable asset for retirees, providing a financial legacy and a source of income. Permanent life insurance policies offer a cash value that can be accessed during retirement, but it's important to purchase such a policy well in advance. Term life insurance is often a more cost-effective option, providing more money to invest for retirement. Life insurance can also protect against the loss of income, which may be particularly relevant for retirees with children or other dependents. However, the value of life insurance for retirees depends on individual circumstances, such as net worth and the need for an asset uncorrelated to the stock market.

| Characteristics | Values |

|---|---|

| Type | Permanent or term |

| Risk | Whole life insurance offers the lowest amount of risk |

| Tax | Growth is tax-deferred |

| Benefits | Can be used as an additional income stream in retirement |

Explore related products

What You'll Learn

![]()

Permanent life insurance

The cash value of a permanent life insurance policy can be accessed in a tax-advantaged manner, but you have to pay interest on any loans you take from your policy, and you have to repay them, or your beneficiaries will receive a reduced death benefit, or your policy may lapse. The total death benefit to be paid to your beneficiaries is simply reduced by the amount of cash-value withdrawals you've made.

Switching Life Insurance: Is It Possible to Change Providers?

You may want to see also

Explore related products

![]()

Term life insurance

Life insurance retirement plans (LIRPs) bring life insurance and retirement together through the cash value feature of permanent life insurance. As you make premium payments, your cash value increases based on the policy's terms, and growth is tax-deferred. At retirement, you can access your cash value to generate extra income or pay for various expenses.

Life Insurance Proceeds: Maryland's Tax Laws Explained

You may want to see also

Explore related products

$14.99 $25.99

![]()

Whole life insurance

Life insurance retirement plans (LIRPs) bring together life insurance and retirement through the cash value feature of permanent life insurance. Whole life insurance is a type of permanent life insurance, which means it does not have an expiration date as long as you keep paying the premiums. Whole life insurance tends to offer policyholders the lowest amount of risk.

As you make premium payments, your cash value increases based on the policy's terms, and growth is tax-deferred. At retirement, you can access your cash value to generate extra income or pay for various expenses. The total death benefit to be paid to your beneficiaries is simply reduced by the amount of cash-value withdrawals you've made.

Life and Health Insurance: Is Your License Active?

You may want to see also

Explore related products

![]()

Using life insurance as an additional income stream

Life insurance can be used as an additional income stream during retirement. This is done through the cash value feature of permanent life insurance. As you make premium payments, your cash value increases based on the policy's terms, and growth is tax-deferred. At retirement, you can access this cash value to generate extra income or pay for various expenses.

There are three types of permanent policies: whole life insurance, term life insurance, and universal life insurance. Whole life insurance tends to offer policyholders the lowest amount of risk and does not have an expiration date as long as you keep paying the premiums. Term life insurance is temporary and offers coverage for a set period, normally 10 to 30 years. If you outlive the term or stop paying premiums, your coverage ends. Universal life insurance is a type of permanent insurance that offers flexible premiums and death benefits.

The cash value of your policy can be used to supplement your retirement income, in addition to your other sources of income such as Social Security, pensions, and investments. It can also be used to cover unexpected expenses, fund your hobbies, travel, or donate to your favourite causes. You can access the cash value of your policy in a tax-advantaged manner, however, you have to pay interest on any loans you take from your policy, and you have to repay them, or your beneficiaries will receive a reduced death benefit, or your policy may lapse.

Life Insurance Certificate: Understanding Your Policy Proof

You may want to see also

Explore related products

![]()

Using life insurance to protect family assets

Life insurance is a commonly used tool to protect against potential income and other losses. One of the benefits of permanent life insurance is the ability to accrue "cash value". This is the balance remaining after a portion of a premium payment is applied to insurance costs. As you make premium payments, your cash value increases based on the policy's terms, and growth is tax-deferred.

At retirement, you can access your cash value to generate extra income or pay for various expenses. You can use the cash value of your policy to supplement your retirement income, in addition to your other sources of income such as Social Security, pensions, and investments. You can also use it to cover unexpected expenses, fund your hobbies, travel, or donate to your favourite causes.

The total death benefit to be paid to your beneficiaries is simply reduced by the amount of cash-value withdrawals you've made. While you might be more familiar with retirement savings tools like IRAs and 401(k)s, some life insurance plans offer you the opportunity to create an additional income stream.

Life Insurance: Estate Planning and Inclusion Explained

You may want to see also

Frequently asked questions

The value of retiree life insurance is that it can be used as an additional income stream in retirement.

Certain types of life insurance policies allow you to accumulate cash value that you can access while you're alive. This cash value increases as you make premium payments.

You can use the cash value of your policy to supplement your retirement income, in addition to your other sources of income such as Social Security, pensions, and investments. You can also use it to cover unexpected expenses, fund your hobbies, travel, or donate to your favourite causes.