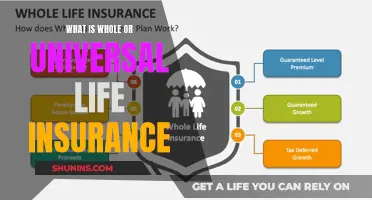

Whole life insurance is a form of permanent life insurance that offers lifelong coverage. It is a financial tool that can help protect your loved ones in case you pass away while the policy is active. Whole life insurance is generally more expensive than term life insurance, with premiums increasing as you age, but it also offers peace of mind that comes with knowing your family will not be left with bills after you pass. It can also help seniors support their surviving partner, pass down wealth to their children or grandchildren, and even support charitable organizations.

| Characteristics | Values |

|---|---|

| Purpose | To provide financial support to loved ones after the policyholder's death |

| Coverage | Lifelong |

| Cost | More expensive than term life insurance; premiums increase with age |

| Payout | Generally tax-free; can be used to replace income, pay off debts, and cover expenses |

| Additional benefits | Accelerated death benefit rider, long-term care rider, living benefits |

| Riders | Additional benefits that can be added to the policy |

| Medical exam required | Varies; some policies do not require a medical exam |

| Peace of mind | Knowing that your loved ones will be taken care of |

Explore related products

What You'll Learn

- Whole life insurance for seniors can be a good option to support your family

- Whole life insurance is a permanent form of insurance that offers lifelong coverage

- Whole life insurance policies are more expensive than term life insurance

- Whole life insurance policies can be purchased without a medical exam

- Whole life insurance policies can be used to pay off debts and cover expenses

![]()

Whole life insurance for seniors can be a good option to support your family

Whole life insurance is a good option for seniors because it provides a guaranteed death benefit, which is generally tax-free. This ensures your loved ones will receive a financial gift when you pass away, without the burden of taxes. Additionally, whole life insurance policies often come with "living benefits," which can be useful if you experience health issues as you age. For example, the accelerated death benefit rider allows policyholders to receive a portion of their insurance's death benefit while still alive if they are diagnosed with a fatal condition. This can help family members cover the cost of care.

Another advantage of whole life insurance is its wealth-building potential. The cash value of the policy can grow over time, and you may be able to borrow money from it to supplement your retirement income, cover family emergencies, or pay for other expenses. However, it's important to remember that you will need to repay the loan, with interest, to ensure the amount your loved ones receive remains unchanged.

Whole life insurance can also provide peace of mind, knowing that your family will not be burdened with end-of-life medical expenses or funeral costs, which can be significant. As you age, the cost of a new life insurance policy increases, and term life insurance may become unaffordable or difficult to obtain. Whole life insurance ensures your coverage is guaranteed for life, and you won't have to worry about outliving your policy.

When considering whole life insurance, it's important to think about your family's needs and your personal finances. The amount of coverage you need will depend on factors such as whether you have young children or grandchildren to support, adult children who need assistance, or outstanding debts you want to be paid off. Working with a financial advisor can help you navigate the complexities of different policies and choose the best option for your situation.

Fully Underwritten Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Whole life insurance is a permanent form of insurance that offers lifelong coverage

Whole life insurance is a type of permanent life insurance designed to provide coverage for an individual's entire lifetime. Unlike term life insurance, which has a specified duration, whole life insurance offers a lifelong financial safety net for seniors and their loved ones. This type of policy combines a death benefit with a savings component, known as the policy's cash value, making it an attractive option for those seeking long-term financial security.

One of the key advantages of whole life insurance for seniors is the guaranteed coverage regardless of age or health condition. While the premiums may be higher compared to term life insurance, whole life insurance policies offer fixed premiums that do not increase with age. This can be especially beneficial for seniors who may have medical issues or face challenges in obtaining affordable coverage. With whole life insurance, they can secure permanent coverage without worrying about future insurability or increasing costs.

The death benefit associated with whole life insurance provides a guaranteed payout to the policyholder's beneficiaries upon their death. This benefit remains tax-free and can be used to cover funeral expenses, pay off outstanding debts, or provide financial support to dependents. The savings component of the policy, known as the cash value, also grows over time. Policyholders can borrow against this cash value or withdraw a portion of it if needed, providing flexibility and access to funds during their lifetime.

Another advantage of whole life insurance for seniors is the potential for cash value accumulation. A portion of the premiums paid into the policy is invested, and the cash value grows tax-deferred. This means that the policy can act as a savings vehicle, providing an additional source of funds for retirement or other financial needs. Policyholders can borrow against the cash value to supplement their income or cover unexpected expenses without reducing the death benefit.

Getting Your Non-Resident Life Insurance License: A Guide

You may want to see also

Explore related products

![]()

Whole life insurance policies are more expensive than term life insurance

Whole life insurance is designed to provide coverage for life. As long as the payments are made on time, the insurance will remain active. This lifelong coverage is particularly beneficial for seniors who want long-term coverage and have more complex financial needs.

The cash value component of whole life insurance grows over time on a tax-deferred basis. You can borrow against the accumulated cash value or withdraw from it, often tax-free, for expenses like college tuition, home repairs, or retirement income. This cash value feature is particularly attractive to those who want coverage for life as well as the ability to build retirement wealth and income through the policy's cash value account.

While whole life insurance is more expensive, it is important to consider the benefits and drawbacks of both types of policies. Term life insurance is ideal if you only need coverage for a finite period, such as while raising children or paying off a mortgage. It is also more affordable and can provide a financial safety net for your family in the event of your death.

The right type of policy depends on your financial goals and budget. Seniors should consider their family's needs and their personal finances when deciding on a life insurance policy.

Life Insurance: Making Profit from Policy Premiums

You may want to see also

Explore related products

![]()

Whole life insurance policies can be purchased without a medical exam

Whole life insurance is a form of permanent life insurance that offers lifelong coverage. It is designed to provide coverage for the entire life of the policyholder. This type of insurance can be a popular choice for seniors who want long-term coverage and have more complex financial needs. The coverage never expires, and your loved ones can use the death benefit payout to replace income, pay off debts, and cover expenses.

In some cases, you may be able to defer your medical exam for a certain period after your policy is issued. During this time, you can take steps to improve your health, which may qualify you for a better rate after you take your medical exam. It is important to note that when insurers offer no-exam life insurance, they take on additional risk by not knowing how healthy you are. As a result, most charge higher premiums to balance that risk. No-exam policies have become very competitive, but you may end up paying more than you would for a medically underwritten policy.

The most common no-exam life insurance policies include simplified issue, guaranteed issue, and employer-sponsored life insurance. Simplified issue life insurance is best for young and healthy individuals who want life insurance without a waiting period. Guaranteed issue life insurance provides limited coverage amounts for a predictable premium, and these policies may not be sufficient to meet your family's needs. Employer-sponsored life insurance is typically offered as part of an employee benefits package and is often free or highly affordable. However, the coverage may only be active while you are employed, and the coverage amounts may be limited.

Life Insurance: What Makes a Policy Appreciable?

You may want to see also

Explore related products

![]()

Whole life insurance policies can be used to pay off debts and cover expenses

Whole life insurance is a form of permanent life insurance that offers lifelong coverage. While it is more expensive than term life insurance, the coverage never expires. This type of insurance can be particularly beneficial for seniors who want long-term coverage and have more complex financial needs.

Whole life insurance policies can provide financial protection for your loved ones in the event of your passing. The death benefit payout can be used to replace lost income, pay off debts, and cover various expenses. This can include funeral costs, which typically range from $8,000 to $10,000 or more. By opting for whole life insurance, you can ensure that your family is not burdened with these expenses during their time of grief.

Additionally, whole life insurance policies can assist with end-of-life medical expenses, which can be significantly high. This ensures that your family is not left with substantial medical bills to settle after your passing. Some policies also offer long-term care riders, allowing the policy's death benefit to be used for long-term care in assisted living communities or nursing homes. This can be a prudent decision, given the high cost of long-term care.

Whole life insurance policies can also provide benefits during your lifetime. Some policies offer "living benefits," which can be useful if you encounter health issues as you age. Additionally, whole life insurance may build cash value over time, allowing you to borrow money from your policy for retirement, family emergencies, or other expenses. However, it is important to remember that any borrowed amounts, including interest, will need to be repaid to maintain the full death benefit for your beneficiaries.

Life Insurance in Islam: Halal or Haram?

You may want to see also

Frequently asked questions

Whole life insurance is a form of permanent life insurance that offers lifelong coverage. While whole life insurance is generally more expensive than term life insurance, it offers peace of mind to seniors who want long-term coverage and have more complex financial needs.

Whole life insurance for seniors can help support their surviving partner, pass down wealth to their children or grandchildren, and even support charitable organizations. It can also help cover end-of-life medical expenses, which can be particularly high, and ensure that your family is not left with bills after you pass away. Additionally, whole life insurance may build cash value over time, which can be borrowed for retirement, family emergencies, or other expenses.

The cost of whole life insurance for seniors depends on various factors, including age, health history, and income. Age is one of the main factors, with premiums increasing as you delay purchasing life insurance. For example, a 50-year-old male non-smoker of average height and weight may pay an average of $5,125 per year for a whole life insurance policy with a $250,000 death benefit. This amount is likely to increase for people over 50.