The cost of health insurance in the US has been rising steadily over the years, with workers in 37 states spending 10% or more of their median income on health insurance premiums and deductibles. This has resulted in many families finding it challenging to keep up with the rising healthcare costs, and some even forgoing necessary medical treatment. The percentage of income spent on health insurance varies based on income levels, with lower-income families spending a greater share of their income on health insurance than higher-income families. Federal laws have capped the amount that households need to pay for health insurance at a percentage of their annual income, with the percentage ranging from 0% to 8.5% for tax years 2021 to 2025. This has been implemented through the health insurance premium tax credit, which is facilitated by the state's Health Insurance Marketplace on behalf of the IRS.

| Characteristics | Values |

|---|---|

| Federal laws cap | ranges from 0% to 8.5% for tax years 2021 to 2025 |

| Household income relative to federal poverty level | If the household income is greater than or equal to 400% of the poverty level, the cap is 8.5% |

| Premium tax credit | A tax credit that offsets annual health insurance premiums |

| Modified adjusted gross income (MAGI) | Used to determine eligibility for premium tax credits and other savings for health insurance plans |

| MAGI calculation | Adjusted gross income (AGI) plus untaxed foreign income, non-taxable social security benefits, and tax-exempt interest |

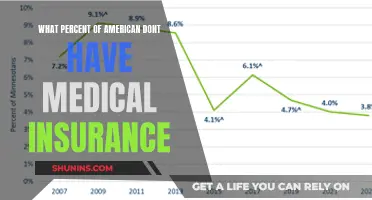

| Average employee premium contributions and deductibles as a percentage of median household income | 11.6% in 2020, including 6.9% in employee premium contributions and 4.7% in deductibles |

| Employer-sponsored health insurance | Organizations contribute a minimum percentage, and employees pay the remaining share |

| Qualified small employer HRA (QSEHRA) | Employers with fewer than 50 full-time employees can reimburse employees tax-free for medical expenses and health insurance premiums up to a maximum contribution limit |

| Individual coverage HRA (ICHRA) | Employers of all sizes can reimburse employees tax-free for individual plan premiums and other out-of-pocket costs |

| Household income estimation | Includes income from all household members, including those with job-based plans, self-purchased plans, or public programs like Medicaid |

| Income adjustments | Deductions for IRA contributions, student loan interest, child care, health coverage, retirement plans, etc. |

| Rising health insurance costs as a percentage of income | Due to increased healthcare costs, insurance premium increases, and economic factors |

| Recommended health insurance costs as a percentage of income | Ideally not exceeding 10% of annual income |

Explore related products

What You'll Learn

![]()

Federal laws cap insurance costs at 0-8.5% of income

Federal laws in the United States cap the cost of individual and family health insurance as a percentage of a household's annual income. This is achieved through a health insurance premium tax credit, which is facilitated by the Health Insurance Marketplace on behalf of the IRS. This tax credit offsets annual health insurance premiums, with the government paying some or all of the costs. For tax years 2021 to 2025, the percentage of income cap ranges from 0% to 8.5%.

The percentage of income cap depends on where a household's income falls relative to the federal poverty level. If a household's annual income is greater than or equal to 400% of the poverty level, the percentage of income cap is 8.5%. This figure is set each year by Health and Human Services (HHS) and is used to determine eligibility for government assistance programs.

The premium tax credit is calculated based on a benchmark plan, which is the second-lowest-cost silver plan available in a particular area. However, individuals are not required to purchase the benchmark plan and can use their premium tax credit to buy any Marketplace plan available in their state.

The percentage of income that goes towards health insurance premiums can vary depending on factors such as plan type, network of providers, plan features, location, and demographics. Employers who offer health insurance coverage to their employees also have a minimum percentage that they must contribute, with employees paying the remaining share.

Battling Insurance Companies: Strategies for Refused Medication Coverage

You may want to see also

Explore related products

![]()

Rising healthcare costs increase insurance premiums

The cost of health insurance is a significant expense for many households, and rising healthcare costs can increase insurance premiums, impacting individuals and employers. While federal laws in the US attempt to cap the amount paid for health insurance as a percentage of household income, the rising cost of healthcare can push insurance premiums higher.

Rising Healthcare Costs and Insurance Premiums

Market concentration among a smaller number of insurance companies is one factor contributing to higher insurance costs. With fewer companies operating in each state, markets become less competitive, leading to higher premiums and reduced access to affordable health insurance. This trend is concerning, as it may result in fewer options and higher costs for consumers.

Impact on Individuals

Rising health insurance premiums can have a detrimental effect on individuals, reducing their chances of employment and lowering their take-home pay. Every 10% increase in health insurance costs reduces the likelihood of employment by 1.6% and leads to a 1% reduction in hours worked. Employers may respond by converting full-time jobs into part-time positions, which often do not include health benefits.

Impact on Employers

Employers are also affected by rising health insurance costs. They may be forced to increase their contributions to maintain coverage for their employees. Alternatively, they may pass on a portion of the cost increase to their employees or shift more positions to part-time roles, which are often exempt from providing health benefits.

Impact on Insurance Coverage

The increase in health insurance premiums can lead to a decline in coverage rates. As premiums rise, low-risk individuals may separate from high-risk individuals, causing adverse selection in the insurance market. This can result in a tendency for the market to unravel as costs increase, leading to declining coverage rates.

In conclusion, rising healthcare costs can significantly impact insurance premiums, affecting individuals' employment and income prospects, employers' operations, and overall insurance coverage rates. These issues highlight the complex challenges faced by individuals, employers, and policymakers in managing the financial burden of healthcare.

Medical Insurance and Dietician Coverage: What's the Verdict?

You may want to see also

Explore related products

![]()

Employers can reimburse employees for medical expenses

In the US, the cost of health insurance is capped at a certain percentage of a household's annual income. This is achieved through a health insurance premium tax credit, which is facilitated by the Health Insurance Marketplace on behalf of the IRS. The premium tax credit offsets annual health insurance premiums, with the government paying for some or all of the costs. The percentage of income cap depends on the household income relative to the federal poverty level. For instance, for the years 2021 to 2025, the percentage of income cap ranges from 0% to 8.5%.

Now, when it comes to employers reimbursing employees for medical expenses, there are a few options available. Firstly, employers can utilize a Health Reimbursement Arrangement (HRA), which allows employees to receive tax-free reimbursements for health insurance premiums and other qualified out-of-pocket medical costs. With an HRA, employees buy their own individual health plan coverage and then submit proof of purchase to their employer for reimbursement up to their allowance amount. It is important to note that HRAs must be integrated with the employer's major medical plan to avoid violating ACA requirements and incurring penalties.

Another option is a health stipend, where employers offer employees a fixed, taxable amount to help cover health insurance and medical expenses. While stipends offer flexibility, they may increase an employee's annual household income, potentially impacting their premium tax credit.

Additionally, there are specific types of HRAs available, such as the Qualified Small Employer HRA (QSEHRA) and the Individual Coverage HRA (ICHRA). The QSEHRA is designed for employers with fewer than 50 full-time equivalent employees who don't want to offer group health insurance. It allows employers to reimburse employees tax-free for medical expenses, including health insurance premiums, up to a maximum contribution limit. On the other hand, the ICHRA is available to employers of all sizes and can be used to reimburse employees tax-free for individual plan premiums and out-of-pocket costs.

It is worth noting that employers should be cautious about reimbursing employees for out-of-pocket medical expenses outside of a formal structure like an HRA, as it may inadvertently create a new group health plan with associated compliance issues. Therefore, consulting relevant regulations and seeking professional advice is recommended when setting up employee reimbursement programs for medical expenses.

Drug History: Medical Records and Life Insurance

You may want to see also

Explore related products

![]()

Household income affects eligibility for government assistance

Household income is a key factor in determining eligibility for government assistance. In the United States, the government provides various benefits to support individuals and families, including assistance with food, housing, healthcare, and other essential needs. When applying for government assistance, individuals or households are typically required to disclose their income and household composition. This information is crucial for assessing eligibility and determining the amount of support provided.

The Supplemental Nutrition Assistance Program (SNAP), formerly known as the Food Stamp Program, is a prime example of how household income affects eligibility. SNAP is designed to help families and individuals who meet specific income guidelines. The size of the SNAP benefit allocated to a family is directly linked to its income and certain expenses. Households with lower incomes generally qualify for higher benefits. To ensure fairness, SNAP takes into account various factors, including earned and unearned income, assets, and deductions for essential expenses like dependent care and medical costs.

Similarly, income plays a significant role in determining eligibility for healthcare assistance. The Affordable Care Act (ACA) Health Insurance Marketplace offers savings and subsidies based on household income. The IRS facilitates this through the health insurance premium tax credit, which offsets annual health insurance premiums. The premium tax credit is calculated as a percentage of the household's income, with a cap that varies according to the federal poverty level. Households with incomes below or close to the poverty line receive higher credits, reducing their out-of-pocket health insurance costs.

Additionally, income considerations extend to housing assistance. The US Department of Housing and Urban Development (HUD) offers rental assistance programs, such as public housing or Housing Choice Vouchers, which are often income-based. Households with lower incomes relative to their local area may qualify for assistance in securing safe and affordable housing. Eligibility is typically determined by comparing the household's income to the median income in their county or metropolitan area.

It's important to note that household income isn't the sole criterion for government assistance. Other factors, such as age, disability, household size, and assets, also come into play. These factors help create a comprehensive picture of an individual's or family's financial situation and needs, ensuring that assistance is provided to those who need it most.

Medicaid and State Insurance: What's the Deal?

You may want to see also

Explore related products

![]()

Income changes should be reported to avoid missing out on savings

The percentage of income spent on medical insurance varies depending on factors such as household income, the number of dependents, and the type of insurance plan chosen. Federal laws in the United States cap the amount that individuals and families must pay for health insurance as a percentage of their annual income. This percentage, known as the premium tax credit, offsets annual health insurance premiums and ranges from 0% to 8.5% for tax years 2021 to 2025.

To ensure that individuals receive the correct amount of savings and are enrolled in the appropriate insurance plan, it is important to report income and household changes promptly. Here are some reasons why income changes should be reported to avoid missing out on savings:

Impact on Savings and Eligibility

Marketplace savings for health insurance are calculated based on the expected household income for the year an individual wants coverage. This includes income from all household members, even those who do not require insurance themselves. By reporting income changes, individuals can ensure that their savings are accurately calculated, maximizing their benefits. Additionally, income changes may affect eligibility for government assistance programs like Medicaid and premium tax credits, so timely reporting is essential.

Choosing the Right Insurance Plan

Income changes can impact the type of insurance plan that best suits an individual's financial situation. For instance, a high-deductible plan may be more cost-effective for some, while others may benefit from moving dependents to an individual policy. By reporting income changes, individuals can receive guidance in selecting the most suitable insurance plan for their updated financial circumstances.

Adjusting Contributions and Reimbursements

For those with employer-sponsored health insurance, income changes can affect the contribution strategies of their organizations. Reporting income changes allows employers to adjust their contribution limits and reimbursement policies accordingly. This ensures that employees can maximize their benefits and take advantage of tax-free reimbursements for eligible medical expenses.

Impact on Federal Income Taxes

Income changes can influence an individual's federal income taxes. By participating in a Section 125 plan or cafeteria plan, employees can contribute a taxable portion of their salary towards health insurance premiums on a pre-tax basis. As a result, their overall taxable household income decreases, leading to potential savings on federal income taxes, Medicare taxes, and Social Security taxes.

Utilizing Health Savings Accounts (HSAs)

Income changes may impact an individual's ability to contribute to or utilize a Health Savings Account (HSA). HSAs allow individuals to set aside pre-tax dollars for medical costs, including doctor visits, prescriptions, and over-the-counter medications. By reporting income changes, individuals can make informed decisions about contributing to or withdrawing from their HSAs to maximize their savings.

In summary, reporting income changes is crucial to ensure that individuals receive the correct savings, are enrolled in the appropriate insurance plan, and can take advantage of various cost-saving measures. By staying proactive and providing up-to-date income information, individuals can maximize their benefits and avoid missing out on valuable savings opportunities.

Selecting the Right Insurance Plan: A Medicaid Guide

You may want to see also

Frequently asked questions

For tax years 2021 to 2025, the percent of income cap ranges from 0 percent to 8.5 percent. This depends on your household income relative to the federal poverty level.

The federal poverty level is set each year by Health and Human Services (HHS). It is used to determine eligibility for government assistance programs like Medicaid and premium tax credits.

Your income for health insurance purposes is your total (or "gross") income for the tax year, minus certain adjustments. Adjustments include deductions for IRA contributions, student loan interest, and more.

In 2020, an employee’s total potential out-of-pocket medical costs (premium and deductible) amounted to 11.6 percent of median income. However, this varies depending on individual circumstances and states.

This depends on the employer and the type of health insurance plan. Some employers reimburse employees for medical expenses, including health insurance premiums, through a health reimbursement arrangement (HRA).