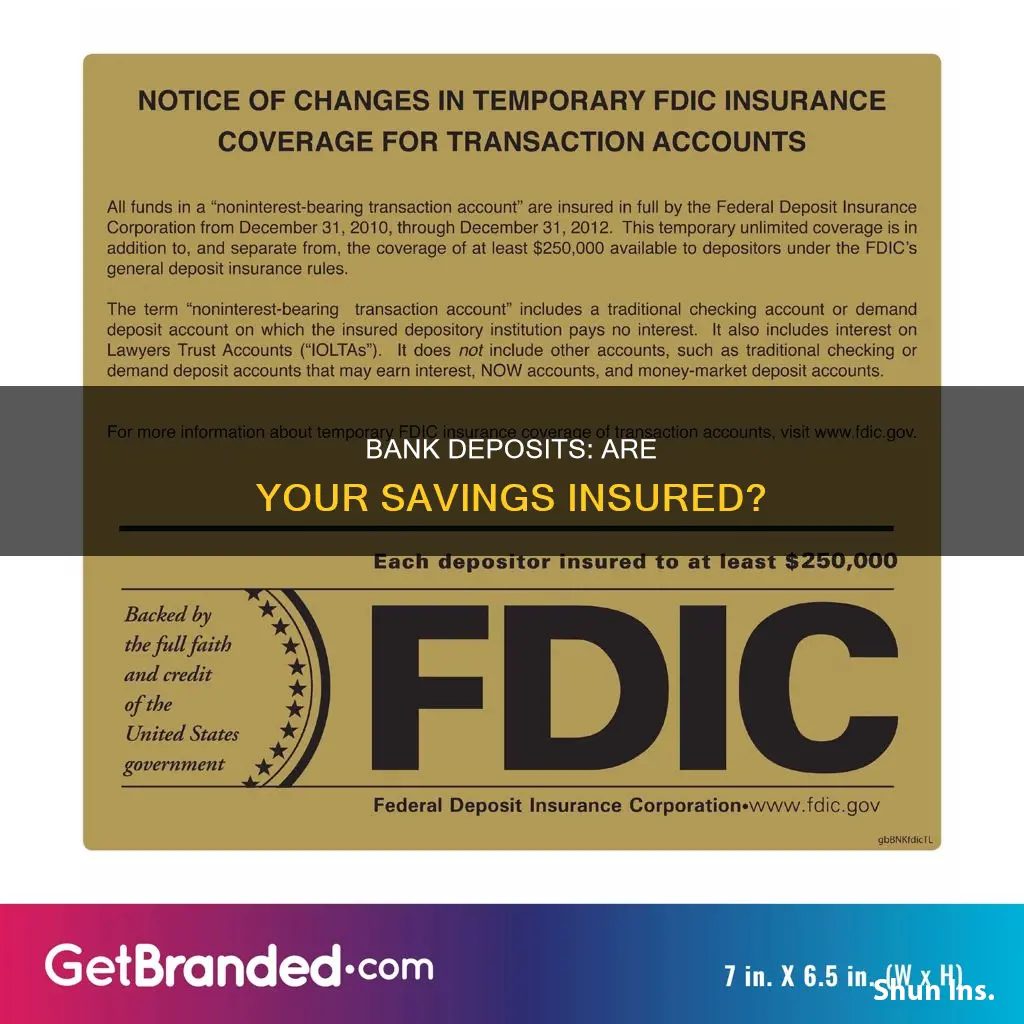

Deposit insurance is the government's guarantee that an account holder's money at an insured bank is safe up to a certain amount. The Federal Deposit Insurance Corporation (FDIC), a government agency, was created in 1933 during the Great Depression to maintain confidence in the nation's financial system. The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category, although this can be higher if you have deposits in different account categories at the same FDIC-insured bank. FDIC deposit insurance covers the balance of each depositor's account, including principal and any accrued interest, and protects depositors against the failure of an insured bank. However, it is important to note that not all banks are FDIC-insured, and as of 2022, about 43% of all bank deposits were uninsured.

| Characteristics | Values |

|---|---|

| Organization | Federal Deposit Insurance Corporation (FDIC) |

| Coverage | $250,000 per depositor, per insured bank, for each account ownership category |

| Account Types Covered | Checking, savings, money market accounts, and certificates of deposit (CDs) |

| Account Types Not Covered | Investment products (stocks, bonds, mutual funds, etc.), cryptocurrencies, contents of safe deposit boxes, life insurance policies, annuities, municipal securities |

| Coverage Calculation | Total of all deposit accounts in the same ownership category at the same bank, regardless of deposit type |

| Coverage Verification | Electronic Deposit Insurance Estimator (EDIE) on the FDIC website |

| Coverage Limit | $250,000 per account |

| Coverage for Joint Accounts | $250,000 per owner |

| Coverage for POD Accounts | $250,000 per beneficiary, up to a total of $1.25 million |

| Coverage for Retirement Accounts | $250,000, separate from other accounts |

| Coverage for Business Accounts | $250,000, independent of personal accounts |

| Coverage for Trust Accounts | $250,000 for each named beneficiary |

| Coverage for Employee Plans | $250,000 for non-contingent interest |

| Coverage for Corporate Deposits | $250,000 |

| Coverage in Case of Bank Failure | Insured deposits are protected, and FDIC acts quickly to ensure prompt access |

| Uninsured Deposits Ratio by Bank Size | Larger banks tend to hold larger percentages of uninsured deposits |

| Total Uninsured Deposits | About $7 trillion (about 45% of all domestic deposits as of 2022) |

Explore related products

What You'll Learn

![]()

The Federal Deposit Insurance Corporation (FDIC)

The FDIC's role is to maintain confidence in the nation's financial system. It does this by insuring bank deposits, examining financial institutions for soundness, working with troubled banks, and managing them in receivership. The FDIC covers the following types of accounts: checking, savings, money market accounts, and certificates of deposit (CDs). FDIC insurance covers the principal and any accrued interest on all bank deposits up to $250,000 per depositor, per insured bank, for each account ownership category. This limit applies to all single accounts owned by the same person at the same insured bank. POD accounts are insured up to $250,000 for each beneficiary, with a maximum total of $1.25 million.

FDIC insurance does not cover investment products such as stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if purchased from an insured bank. U.S. Treasury bills, bonds, and notes are also excluded. The FDIC has no jurisdiction over cases or losses incurred by identity theft.

The FDIC is managed by a five-member Board of Directors, including a Chairman, Vice Chairman, Appointive Director, the Comptroller of the Currency, and the Director of the Bureau of Consumer Financial Protection. No more than three members of the Board can be from the same political party. The FDIC has published documents in the Federal Register, including information on deposit insurance coverage and resources for bankers.

Since its inception in 1933, the FDIC states that no depositor has ever lost money in their FDIC-insured funds.

Private Insurance: Healthcare's Friend or Foe?

You may want to see also

Explore related products

![]()

FDIC-insured banks

The Federal Deposit Insurance Corporation (FDIC) is an independent agency created by Congress to maintain stability and public confidence in the nation's financial system. The FDIC insures deposits, supervises financial institutions for safety, and manages receiverships. FDIC-insured banks protect your money in the event of a bank failure. FDIC deposit insurance covers the balance of each depositor's account, including principal and any accrued interest, up to a maximum of $250,000 per depositor, per insured bank, for each account ownership category. This includes checking, savings, money market accounts, and certificates of deposit (CDs). Coverage is automatic when you open one of these accounts at an FDIC-insured bank.

The FDIC provides tools and resources to help consumers make informed decisions and protect their assets. Their Electronic Deposit Insurance Estimator (EDIE) helps calculate how much of your bank deposits are covered by FDIC insurance and if any portion exceeds the coverage limits. This calculator is available on the FDIC's website, along with other resources such as FAQs and brochures that provide basic information about the types of accounts insured, coverage limits, and how the FDIC insures your money.

It is important to note that FDIC insurance does not cover investment products such as stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if purchased from an insured bank. Additionally, it does not protect against losses due to theft or fraud, which are addressed by other laws. FDIC insurance is also not applicable to uninsured deposits, which make up a significant portion of total domestic deposits, especially in larger banks.

Since 1934, no depositor has lost any FDIC-insured funds. This assurance has helped maintain confidence in the financial system, and the FDIC continues to play a crucial role in ensuring the safety and stability of deposits in FDIC-insured banks.

Pennsylvania's Financial and Insurance Regulatory Body

You may want to see also

Explore related products

![]()

Deposit insurance coverage

The standard insurance amount is $250,000 per depositor, per FDIC-insured bank, for each account ownership category. This includes checking, savings, money market accounts, and certificates of deposit (CDs). Deposit insurance is calculated dollar-for-dollar, including the principal and any interest accrued or due to the depositor through the date of default. For example, if a customer had a CD account with a principal balance of $195,000 and $3,000 in accrued interest, the full $198,000 would be insured.

It is important to note that FDIC insurance does not cover all types of accounts and financial products. It does not insure investment products such as stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if they are purchased from an insured bank. Additionally, U.S. Treasury bills, bonds, and notes are also excluded from FDIC coverage. To determine if a bank is FDIC-insured and to understand the specific coverage for different account types, individuals can refer to the FDIC's resources, including the Electronic Deposit Insurance Estimator (EDIE) calculator available on their website.

Barclays Bank Delaware: Is Your Money Safe?

You may want to see also

Explore related products

![]()

Types of accounts insured

The Federal Deposit Insurance Corporation (FDIC) is an independent agency of the United States government that was established in 1933 after thousands of banks went out of business during the Great Depression. The FDIC protects depositors (bank customers) against the loss of their insured deposits in the unlikely event that an FDIC-insured bank fails. It does not protect against losses due to theft or fraud, which are addressed by other laws.

The FDIC covers the following types of accounts:

- Checking or current accounts

- Savings accounts

- Money market accounts

- Certificates of Deposit (CDs)

- Negotiable orders of withdrawal (NOW)

- Money market deposit accounts (MMDA)

FDIC insurance covers the principal and any accrued interest through the insured bank's closing date on all your bank deposits. The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. This means that if you have deposits in different account categories at the same FDIC-insured bank, your insurance coverage may be more than $250,000, if all requirements are met.

FDIC deposit insurance does not cover all types of accounts. Financial instruments, such as stocks, bonds, money market funds, cryptocurrency, U.S. Treasury securities (T-bills), safe deposit boxes, annuities, and insurance products aren't insured by the FDIC. The FDIC also doesn't insure regular shares and share draft accounts of credit unions.

Self-directed retirement accounts, such as 401ks, IRAs, or profit-sharing plans, are also insured up to $250,000. Trust accounts and employee benefit accounts are less commonly used and have more complex insurance rules and limits.

It is important to note that while FDIC insurance is a safety net, it does not cover all scenarios. Uninsured deposits in banks can still occur and have been observed in recent times, with some large banks reporting that around 90% of their total domestic deposits were uninsured.

TD Bank: FDIC Insurance and Your Money

You may want to see also

Explore related products

![]()

Calculating your insurance coverage

The Federal Deposit Insurance Corporation (FDIC) provides deposit insurance to protect your money in the event of a bank failure. Your deposits are insured up to at least $250,000 per depositor, per FDIC-insured bank, per ownership category. This includes all deposit accounts you hold in the same ownership category at the same bank, regardless of the deposit type (e.g. checking, savings, money market accounts, and certificates of deposit (CDs)).

If you have deposits in different account categories at the same FDIC-insured bank, your insurance coverage may be more than $250,000, provided all requirements are met. On the other hand, if you have accounts at different FDIC-insured banks, the $250,000 limit applies at each bank.

Deposit insurance covers the principal and any accrued interest through the insured bank's closing date. It's important to note that FDIC insurance does not cover investment products such as stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if purchased from an insured bank.

To calculate your specific insurance coverage amount, you can use the FDIC's Electronic Deposit Insurance Estimator (EDIE), available on their website. Alternatively, you can call the FDIC at 1-877-275-3342 (1-877-ASK-FDIC) to determine your deposit insurance coverage.

It's important to ensure that your bank is FDIC-insured. You can do this by asking a bank representative, looking for the FDIC sign at your bank, or using the FDIC's BankFind tool, which provides detailed information about all FDIC-insured institutions.

Fire Insurance for Private Forests: Is It Possible?

You may want to see also

Frequently asked questions

In the US, the Federal Deposit Insurance Corporation (FDIC) insures deposits up to \$250,000 per depositor, per insured bank, for each account ownership category. This means that if you have multiple accounts in different categories at the same bank, your total insured amount may exceed \$250,000. FDIC insurance covers checking, savings, money market, and certificate of deposit (CD) accounts.

Deposit insurance coverage is automatic when you open a deposit account at an FDIC-insured bank. You can determine if a bank is FDIC-insured by asking a bank representative, looking for the FDIC sign at your bank, or using the FDIC's BankFind tool on their website.

In the unlikely event of a bank failure, the FDIC acts quickly to ensure that depositors receive their insured funds. The FDIC will either provide each depositor with a new account at another insured bank with an equal balance to their insured amount or issue a check for the insured balance.

FDIC insurance does not cover investment products such as stocks, bonds, mutual funds, life insurance policies, annuities, or municipal securities, even if purchased from an insured bank. It also does not cover U.S. Treasury bills, bonds, and notes, nor does it protect against losses due to theft or fraud.