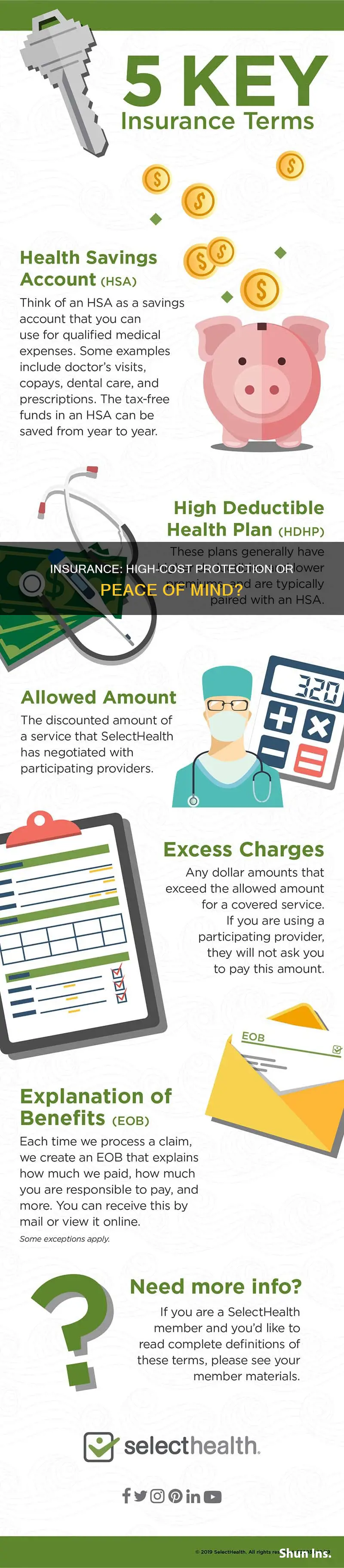

The decision to opt for a high or low deductible insurance plan depends on several factors, including the type of insurance, an individual's financial situation, and their risk appetite. A deductible is the amount paid out-of-pocket by the policyholder before the insurance company covers the remaining costs. In the context of health insurance, a high-deductible plan is suitable for young, healthy individuals who are less likely to incur significant medical expenses. These plans offer lower premiums, providing more manageable monthly payments and access to Health Savings Accounts (HSAs). However, high-deductible plans also shift a larger portion of healthcare costs to the individual, potentially resulting in higher out-of-pocket expenses in the event of a medical issue. On the other hand, car insurance deductibles allow individuals to choose between lower or higher deductibles, impacting their insurance rates. While a high deductible leads to lower rates, it also means higher out-of-pocket costs in the event of a claim. Similarly, homeowners' insurance deductibles vary based on the specific risks associated with natural disasters, such as hurricanes, floods, or earthquakes, in the policyholder's location. Ultimately, the choice between a high or low deductible plan requires careful consideration of one's financial capabilities, health status, and the likelihood of incurring expenses that would trigger the insurance coverage.

| Characteristics | Values |

|---|---|

| Insurance type | Car, health, homeowners |

| Pros of high deductible | Lower premiums, more manageable premiums, lower rates, better for young and healthy individuals |

| Cons of high deductible | Higher out-of-pocket costs, higher out-of-pocket maximum limits |

| Deductible amount | Car insurance: $100-$2000, most common is $500; Health insurance: $1,400 for individuals and $2,800 for family plans in 2022; Homeowners insurance: $500-1000, or a percentage of the policy limits |

| Factors influencing deductible | Coverage, insurer, premium amount, state regulations, risk of natural disasters |

Explore related products

What You'll Learn

- Insurance investigators combat fraud and suspicious claims

- Private investigators need insurance to protect against liabilities and financial losses

- Insurance investigators require strong communication and active listening skills

- Insurance investigators collect data through interviews and research

- Insurance investigators determine the validity of claims

![]()

Insurance investigators combat fraud and suspicious claims

Insurance investigators play a crucial role in combating fraud and suspicious claims, ensuring that only legitimate claims are approved. They inspect and research insurance claims, gathering information from various sources, including adjusters, law enforcement, claimants, and witnesses, to determine the validity of a claim. This process helps insurance adjusters make informed decisions about how to proceed.

The role of an insurance investigator is to examine suspicious or doubtful insurance claims, often triggered by red flags such as suspicious financial activities, inconsistencies in claims, or patterns indicative of fraudulent behaviour. Investigators with varying specialties and backgrounds may be employed in-house by insurance companies or subcontracted to private investigators or investigation firms. They collect and review relevant documents, interview victims and witnesses, and study the claimant's activities and background to assess the legitimacy of reported injuries.

Insurance fraud can take many forms, including false claims, staged accidents, inflated damages, exaggerated injuries, falsified documents, and premeditated incidents like arson. Fraudsters may attempt to deceive insurers by fabricating or inflating claims to receive unwarranted payouts. Investigators look for inconsistencies and gather evidence to support or refute the claim, utilizing tools such as case management software, forensic accounting, and digital forensics.

Common types of insurance fraud include premium diversion schemes, where an unlicensed agent sells insurance and collects premiums without paying claims, and fee churning, where intermediaries repeatedly take commissions through reinsurance agreements, leaving insufficient funds to pay claims. Asset diversion, the theft of insurance company assets during acquisitions or mergers, is another form of fraud.

Insurance investigators help combat these fraudulent activities, protecting insurance companies from significant financial losses and safeguarding the integrity of the claims process. They play a vital role in ensuring fair and legitimate outcomes for all parties involved.

Verify Auto Insurance: Active or Not?

You may want to see also

Explore related products

$3.89

$3.89

![]()

Private investigators need insurance to protect against liabilities and financial losses

Private investigators (PIs) face a multitude of risks and challenges in their line of work. They may be called upon to perform a wide range of services, many of which could potentially expose them to legal action if they make a mistake or fail to fulfil a duty as expected. As such, it is essential that PIs have the right insurance coverage to protect them against liabilities and financial losses.

Private investigator insurance is a specialised liability coverage tailored to protect PIs from the unique risks they face while conducting investigations. Due to the nature of their work, PIs are more exposed to liability than workers in many other occupations. For example, a PI may be sued for negligence or alleged negligence, harmful advice, personal injury, libel and slander, or actions of employees. If an "injured" party wins a lawsuit against a PI, it could have significant career consequences and result in the loss of financial and personal assets.

To mitigate this risk, PIs should carry various types of liability insurance, including general liability, auto liability, property protection, and workers' compensation. General liability insurance protects against personal injury, injury to another person, or damage to their property while performing work duties. Auto liability covers clients who drive during work, whether in a company vehicle or their own car. Property protection covers the client's work location if they own it, and workers' compensation protects clients in the event of on-the-job injuries.

Another important type of liability coverage is professional liability, or errors and omissions (E&O) insurance. This protects the client against professional negligence or mistakes that cause harm to clients, including financial losses. For example, if a PI fails to thoroughly research a situation and provides faulty or incomplete information that causes a client to make a poor decision. Invasion of privacy coverage is also crucial, as claims of "invasion of privacy" are a significant professional risk for PIs.

In conclusion, private investigators need insurance to protect themselves against liabilities and financial losses that could arise during the course of their work. By carrying sufficient liability insurance coverage, PIs can have peace of mind and focus on their investigations without worrying about potential risks and consequences.

Auto Insurance and Legal Representation: Understanding Your Policy

You may want to see also

Explore related products

![]()

Insurance investigators require strong communication and active listening skills

Insurance investigators play a crucial role in the insurance industry by examining suspicious or questionable insurance claims to determine their validity and detect potential fraud. They gather information from various sources, including adjusters, law enforcement, claimants, and witnesses, often through interviews and investigative research. Given the nature of their work, strong communication and active listening skills are essential for insurance investigators.

Effective communication skills enable insurance investigators to interact confidently with a diverse range of individuals, including claimants, witnesses, law enforcement officers, and other professionals. They must be adept at conducting interviews, eliciting information, and building rapport with people from varying backgrounds. Strong communication skills also encompass the ability to explain complex insurance terms and policies in a clear, concise, and understandable manner. This ensures that claimants and clients fully grasp the details of their coverage options.

Active listening is a vital aspect of effective communication for insurance investigators. By actively listening, investigators can carefully process the information provided by claimants, witnesses, and other sources. This skill enhances their ability to identify discrepancies, inconsistencies, or potential signs of fraud. Active listening also enables investigators to demonstrate empathy and build trust with individuals sharing sensitive or personal information.

Strong communication and active listening skills are further advantageous when insurance investigators collaborate with legal professionals. Investigators need to convey their findings accurately and comprehensively to legal experts, who then make informed decisions based on the presented information. Clear communication and active listening facilitate effective collaboration between investigators and legal counsel, ultimately contributing to the resolution of insurance claims.

In addition to strong communication and active listening skills, insurance investigators should possess a range of other competencies. These include critical thinking, decision-making, negotiation, persuasion, and organisational skills. A solid understanding of insurance law and investigative techniques is also essential for their success in detecting fraud and ensuring fair claim outcomes.

Michigan Auto Insurance: Lowering Rates and Reform

You may want to see also

Explore related products

![]()

Insurance investigators collect data through interviews and research

Insurance investigators play a crucial role in the insurance industry by examining suspicious or questionable insurance claims to determine their validity and ensure no fraud is occurring. They collect data through various methods, including interviews and investigative research, to develop a comprehensive understanding of each case.

The process typically begins with a review of relevant documents, such as medical records, police reports, or accident reports, depending on the nature of the claim. This initial document analysis provides a foundation for the investigation and helps identify key individuals to interview.

Interviews are a fundamental tool for insurance investigators. They conduct in-depth interviews with claimants, victims, and witnesses to gather firsthand information and statements. These interviews aim to clarify the circumstances surrounding the incident, understand the impact on the claimant's life, and identify any potential discrepancies or inconsistencies in the information provided.

During their research, insurance investigators also collaborate closely with law enforcement, adjusters, and relevant experts. They seek input from professionals in various fields, such as medical staff for injury claims, to verify the legitimacy of the reported damages or injuries. This collaborative approach ensures a more informed assessment of the claim.

Additionally, insurance investigators may employ surveillance techniques and social media tracking to further corroborate the information gathered. By observing the claimant's activities and behaviour, investigators can identify any signs that contradict the reported injuries or losses. This aspect of the investigation helps detect potential fraud or exaggeration of claims.

Through their meticulous data collection and analysis, insurance investigators play a vital role in protecting insurance companies from fraudulent claims. Their investigations also ensure fair payouts for legitimate claims, ultimately safeguarding the interests of both the insurance providers and honest policyholders.

Auto Insurance: Understanding the Right Amounts to Carry

You may want to see also

Explore related products

![]()

Insurance investigators determine the validity of claims

Insurance investigators play a crucial role in the insurance industry by assessing the validity of claims and preventing fraud. They are responsible for examining suspicious or questionable insurance claims to determine whether they are legitimate or fraudulent. The process involves gathering evidence, conducting interviews, and reviewing records to make an informed decision.

The role of an insurance investigator is to help insurance companies decide whether to pay out on a claim. They work on behalf of insurance companies, either as in-house investigators or as subcontractors, to investigate claims and protect the company from financial losses due to fraud. Insurance fraud can have significant financial implications for insurance companies and policyholders, leading to increased premiums and a loss of trust in the insurance system. Therefore, the work of insurance investigators is vital in maintaining the integrity of the industry.

Insurance investigators handle a range of claims, including those related to suspected criminal activities such as arson, unnecessary medical treatments, and staged accidents. They begin their process by collecting and reviewing relevant documents, such as incident reports and medical records. They then interview the claimant and witnesses to gather statements and perspectives on the incident. Investigators may also examine the scene of the incident, survey damaged goods or property, and consult with law enforcement or other experts to gain a comprehensive understanding of the situation.

In some cases, insurance investigators may employ surveillance techniques or social media tracking to verify the legitimacy of a claim, especially when it comes to assessing the extent of injuries or damages claimed. For example, in a personal injury claim, an investigator may conduct surveillance to determine if the claimant's activities align with the reported injuries. This helps in identifying potential fraud or exaggeration of injuries, which is a common form of insurance fraud.

Throughout the investigation, insurance investigators must be detail-oriented, analytical, and possess strong critical thinking skills. They need to evaluate all the gathered information, identify discrepancies, and make informed conclusions about the validity of the claim. Once their investigation is complete, they document their findings in a report and submit it to the insurance company or legal professionals, who then make the final decision regarding the claim.

Understanding Insurance Coverage for Non-Drivers: What You Need to Know

You may want to see also

Frequently asked questions

A high deductible plan is better suited for those who are young, generally healthy, and don't expect to pay too much for coverage. You pay less each month in premiums but are responsible for a greater portion of out-of-pocket health care costs.

Choosing the right insurance plan depends on your personal situation. If you are older, have a chronic health condition, or need pricey prescriptions, a lower deductible may be more appealing. If you are young and healthy, a high deductible plan could be a better fit.

With a high deductible plan, you pay less each month in premiums but more for your out-of-pocket costs until you pay 100% of your deductible. Once you reach that limit, the insurance pays 100% of the allowable amount for the rest of the calendar year.