When shopping for medical insurance, it is important to consider your needs and ask yourself some basic questions. Are you purchasing insurance for yourself or your family? How often do you typically visit the doctor? Do you have any chronic conditions or require specialist care? Understanding your deductible, copayments, and coinsurance is also essential. You should know what services and benefits are covered by each policy and whether your preferred doctors and hospitals are part of the plan's network. Additionally, consider using tools and calculators to compare plans and understand if you qualify for financial assistance.

| Characteristics | Values |

|---|---|

| Number of people covered | Self, dependent, or family |

| Frequency of doctor visits | Number of times one visits the doctor in a year |

| Specialist requirements | Whether one requires a specialist |

| Chronic conditions | Any chronic condition or medical need that will require attention in the coming year |

| Annual household income | To check if one qualifies for financial help |

| Tier of coverage | Bronze, Silver, Gold, or Platinum |

| In-network doctors | Whether preferred doctors are included in the plan |

| Prescription drugs | Whether regular prescriptions are covered |

| Deductible | The amount one must pay out-of-pocket before the health plan pays |

| Copayments | The amount paid out-of-pocket when visiting a doctor or specialist |

| Coinsurance | The amount of the medical bill one must pay after meeting the deductible |

| Plan type | PPO, EPO, or HMO |

| Provider network | Whether preferred providers are part of the network |

| Open Enrollment period | The period when one can shop for a plan |

Explore related products

What You'll Learn

![]()

Know your deductible, copayments, and coinsurance

When shopping for medical insurance, it is important to understand the financial implications of your plan. Knowing the details of your deductible, copayments, and coinsurance will help you make an informed decision and avoid unexpected costs.

A deductible refers to the amount you must pay out-of-pocket for medical expenses before your insurance provider begins to cover the costs. Different plans have different deductibles, and it is essential to consider how this amount fits within your budget and anticipated medical needs. For example, if you expect to require surgery or have a chronic condition, a lower deductible may be more suitable.

Copayments, or copays, are the fixed amounts you pay out-of-pocket each time you visit a doctor or specialist, in addition to your premium. Copayments vary depending on the insurance plan and the type of medical service provided. It is important to understand what services are covered by your copayments and whether there are any limitations or exclusions.

Coinsurance refers to the percentage of a medical bill that you are responsible for paying after meeting your deductible. For example, if your coinsurance is 20%, you will pay 20% of the cost of a covered service, and your insurance company will cover the remaining 80%. Coinsurance usually applies to more expensive procedures or treatments, so it is crucial to factor this into your decision-making process.

When considering these factors, it is beneficial to use tools provided by insurance companies or state programs, such as Covered California's Compare and Select a Plan tool, to estimate the total cost of different plans based on your personal circumstances. These tools can help you understand the financial implications of your deductible, copayments, and coinsurance, and whether you qualify for financial assistance to reduce these costs.

By understanding the intricacies of deductibles, copayments, and coinsurance, you can make a well-informed decision when purchasing medical insurance that aligns with your financial situation and healthcare needs.

Navigating Medical Insurance Coverage for LASIK Surgery

You may want to see also

Explore related products

$221.2 $245.95

![]()

Compare plans and their costs

When shopping for medical insurance, it is important to compare plans and their costs. This involves understanding the different types of plans available, their coverage, and their associated expenses. Here are some key considerations:

Plan Types

Different types of medical insurance plans offer varying levels of flexibility and coverage. Some common plan types include Health Maintenance Organizations (HMO), Preferred Provider Organizations (PPO), and Exclusive Provider Organizations (EPO). HMOs typically offer lower costs but restrict you to a specific network of healthcare providers. PPOs provide more flexibility, allowing you to use out-of-network providers at an additional cost. EPOs may offer a combination of features from both HMOs and PPOs. Understanding these plan types and their variations is crucial for making an informed decision.

Provider Networks

When comparing plans, pay close attention to the provider networks. In-network providers have contracted with the insurance company to provide services at a pre-negotiated rate, resulting in lower costs for you. Check if your preferred doctors, hospitals, and specialists are included in the plan's network. Some plans may offer a wider range of in-network providers, giving you more choices for your healthcare needs.

Coverage and Benefits

Understanding the coverage and benefits offered by each plan is essential. Review the specific services covered, such as preventive care, prescription drugs, maternity care, and chronic disease management. Ensure that the plan covers your regular medical needs and any anticipated expenses, such as upcoming surgeries or ongoing treatments. All plans are required to cover essential health benefits, but the additional benefits offered may vary, so it's important to read the fine print.

Out-of-Pocket Expenses

Consider the out-of-pocket expenses associated with each plan. This includes deductibles, copayments (copays), and coinsurance. A deductible is the amount you must pay before your insurance plan starts covering your medical expenses. A copay is a fixed amount you pay for each doctor's visit or service, while coinsurance is the percentage of the medical bill you pay after meeting your deductible. Compare these expenses across plans to understand your financial responsibility.

Premium Costs

Premiums are the regular payments you make to maintain your insurance coverage. They can vary significantly between plans and are influenced by factors such as your age, location, and household size. Calculate the monthly and annual premiums for each plan you're considering to understand the ongoing cost. Also, look into cost-sharing options, where you can share the cost of premiums with your employer or avail of financial assistance programs.

Tools and Resources

Take advantage of online tools and resources to compare plans and costs. Many states and insurance providers offer plan comparison tools that consider your personal circumstances and recommend suitable plans. These tools can help you estimate monthly premiums, annual costs, and even determine your eligibility for financial assistance programs. Utilizing these resources can make the process of comparing plans and their costs more straightforward and informative.

Medica Insurance's Membership Numbers: How Many Are Covered?

You may want to see also

Explore related products

$112.62 $245.95

![]()

Understand your needs and ask basic questions

Understanding your needs and asking basic questions is a crucial step in choosing the right medical insurance plan. Before you begin your search, it is essential to reflect on your specific circumstances and requirements. Here are some key questions to ask yourself:

Who needs insurance coverage?

Consider whether you are seeking insurance just for yourself or if you need to include other family members, such as a spouse, children, or dependents. This information will help tailor the plans presented to you and ensure that everyone who requires coverage is accounted for.

Reflect on your past year's healthcare usage. How frequently did you visit your primary care doctor or any specialists? Do you anticipate any significant changes in the coming year, such as an upcoming surgery, maternity needs, or managing a chronic condition? Understanding your healthcare usage will help you assess how often you may need to utilise your insurance plan.

If you have specific doctors, specialists, or hospitals that you prefer or regularly visit, ensure that they are included in the network of the insurance plan you are considering. Check the directories of in-network providers for each plan. Remember that the larger the provider network, the more choices you will have, but also confirm that in-network doctors are accessible in your area, especially if you reside in a rural location.

Your financial situation will play a role in choosing a medical insurance plan. Consider your annual household income, as this may determine whether you qualify for financial assistance or subsidies to lower the cost of insurance. Additionally, be mindful of factors like premiums, deductibles, copayments, and coinsurance associated with different plans. Understand the total cost of the plan, including any out-of-pocket expenses, and whether it aligns with your budget.

Different insurance plans offer varying levels of coverage for specific benefits. Consider whether you require maternity care, prescription drug coverage, rehabilitative services, preventive care, or chronic disease management. Understand the standard benefits included in each plan and whether they align with your specific needs.

By asking yourself these basic questions, you can gain a clearer understanding of your needs and narrow down the options to find the most suitable medical insurance plan.

Understanding Medical Insurance Deductibles: What You Need to Know

You may want to see also

Explore related products

![]()

Check for your preferred doctors and hospitals in the plan's network

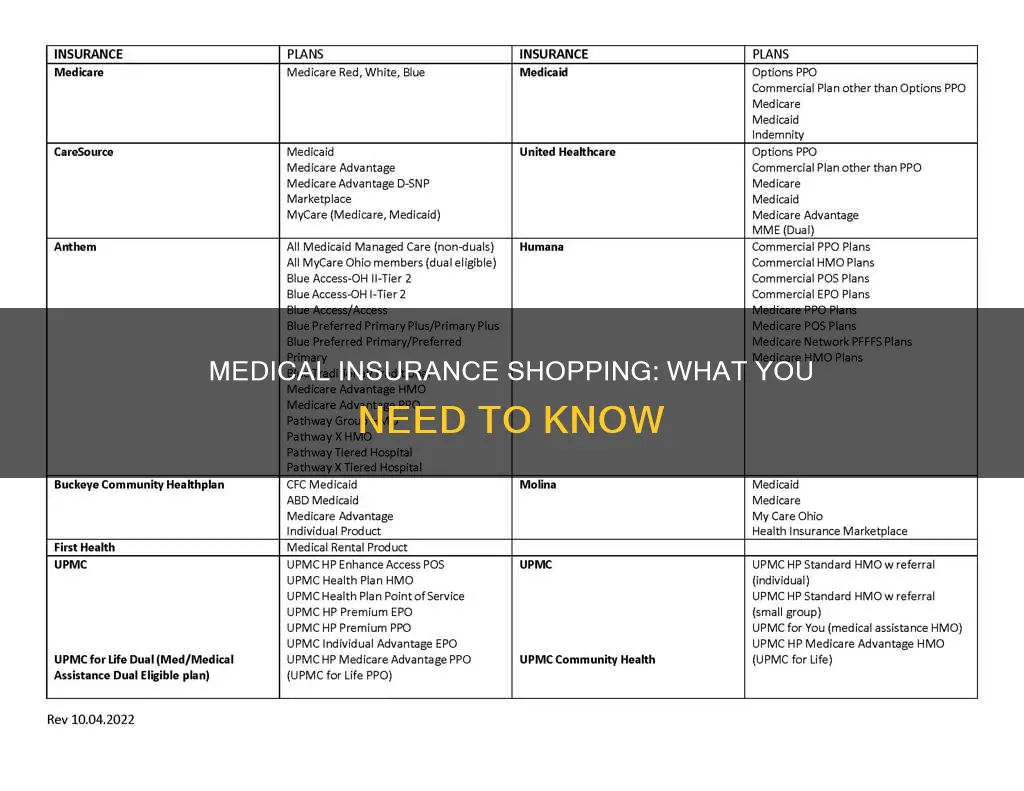

When shopping for medical insurance, it is important to check if your preferred doctors and hospitals are included in the plan's network. This is because some insurance plans have a specific network of healthcare providers with whom they contract to provide care, and you will pay less if you use these in-network providers. If you go to doctors, hospitals, or providers outside of this network, you will likely have to pay an additional cost, and it may not even be covered by your insurance plan unless it is an emergency. Therefore, it is in your best financial interest to check if your preferred healthcare providers are in-network with the insurance plan you are considering.

To do this, you can use the insurance plan's website to check their provider directory, which lists all the in-network doctors, hospitals, and healthcare providers. You can also call the insurer to ask about specific providers. It is also worth noting that the larger the provider network, the more choices you will have, but it is still important to confirm that there are in-network doctors available nearby, especially if you live in a rural area.

In addition, different types of insurance plans have different rules regarding the use of in-network versus out-of-network providers. For example, Health Maintenance Organization (HMO) plans usually limit coverage to in-network care and require you to live or work in their service area to be eligible for coverage. Point of Service (POS) plans require you to get a referral from your primary care doctor to see a specialist, but you will pay less if you use in-network providers. Preferred Provider Organization (PPO) plans offer lower costs for in-network providers, but you can still use out-of-network providers without a referral for an additional cost.

When shopping for medical insurance, it is also important to consider your specific needs and the costs of different plans. Ask yourself questions such as: Are you purchasing insurance for yourself, a dependent, or your whole family? How often do you typically visit the doctor in a year? Do you see specialists? Do you have any chronic conditions or upcoming medical needs, such as surgery or maternity care? Do you have a preferred hospital or primary care doctor you want to continue seeing? By considering these factors, you can ensure that the insurance plan you choose covers your regular care and prescriptions, and that it offers the best value for your needs.

How to Get Insurance to Cover Your Copayments

You may want to see also

Explore related products

![]()

Research providers and insurance companies

When shopping for medical insurance, it is important to research providers and insurance companies. Here are some key things to keep in mind:

Understanding Your Options:

Most health insurance companies offer a standard set of benefits, known as essential health benefits. These typically include services such as maternity and newborn care, preventive services, prescription drug coverage, and rehabilitative services. However, it is important to carefully review the specific benefits covered by each plan, as every plan is different. Understand what your priorities are in terms of healthcare needs and budget, and look for plans that align with those priorities.

Provider Networks:

Some plans have a network of participating providers, including doctors, hospitals, and specialists. Using in-network providers is usually more cost-effective, as you may have to pay additional fees if you choose to go outside of the network. If you have specific doctors or hospitals you prefer, check if they are in-network for the plan you are considering.

Cost Structure:

Understanding the cost structure of a plan is crucial. In addition to monthly premiums, be aware of potential out-of-pocket costs such as deductibles, copays, and coinsurance. Compare the costs across different plans and consider which structure best fits your financial situation and healthcare needs.

Plan Categories:

Health insurance plans are often categorized into metal tiers: Bronze, Silver, Gold, and Platinum. These categories indicate how costs are shared between you and the plan, but they do not reflect the quality of care. Consider the level of coverage you require and choose a plan category that aligns with your anticipated healthcare needs and budget.

Company Reputation and Reliability:

Research the reputation and reliability of insurance companies. Look into customer satisfaction ratings, complaint indices, and the company's financial health. This information can help you assess the quality of their services and their ability to meet your needs over the long term.

Group Health Plans:

If you are considering a group health plan through your employer or another association, understand the specific offerings and limitations of the plan. Employers often offer a choice of plans with different levels of cost-sharing. Evaluate these options carefully and choose the one that best suits your needs.

By thoroughly researching providers and insurance companies, you can make a well-informed decision when choosing a medical insurance plan.

Village Medical at Walgreens: Insurance Options and Coverage

You may want to see also

Frequently asked questions

Before shopping for medical insurance, consider your needs and ask yourself some basic questions: Are you purchasing insurance for yourself, a dependent, or your whole family? How often do you typically visit the doctor each year? Do you see specialists? Do you have a chronic condition or medical need that will require attention in the coming year (e.g., pending surgery or maternity needs)?

There are a few key terms you should be familiar with when shopping for medical insurance:

- Deductible: The amount you must pay out-of-pocket for medical expenses before your health plan starts paying.

- Copayment (copay): The amount you pay out-of-pocket when visiting a doctor or specialist, in addition to your premium.

- Coinsurance: The portion of a medical bill that you must pay after meeting your deductible.

When choosing a medical insurance plan, consider the following:

- Check the directories of in-network healthcare providers to ensure your preferred doctors and hospitals are included.

- Understand what services each policy covers and what your out-of-pocket costs will be.

- Compare the total costs of different plans, including premiums, deductibles, copays, and coinsurance.

- Consider if you qualify for financial assistance to lower your costs.

You can typically buy medical insurance during an Open Enrollment period. There may also be special enrollment periods if you experience certain qualifying events, such as losing your previous coverage.