Many people are asking why their insurance rates are so high. There are many factors that influence insurance costs, such as age, gender, location, credit score, driving record, and type of car. Inflation and the increase in natural disasters and accidents have also contributed to rising insurance costs. Some people find that their insurance rates are higher than average, and this may be due to specific factors such as living in an area with a high crime rate or having a history of accidents.

| Characteristics | Values |

|---|---|

| Driving record | A history of accidents, DUI, or poor behavior on the road will increase insurance rates |

| Age | Younger, less experienced drivers pay higher insurance rates |

| Gender | In most states, gender affects insurance rates |

| Credit score | A credit score under 600 will increase insurance rates (except in California, Hawaii, and Massachusetts) |

| Location | Living in an area with a high crime rate or lots of traffic accidents will increase insurance rates |

| Vehicle safety | Cars with better safety ratings have lower insurance premiums |

| Number of claims | Insurance companies don't like it when a lot of claims are filed |

| Inflation | Rising costs from inflation impact insurance companies, leading to increased rates |

| Natural disasters | An increase in natural disasters and accidents has led to more claims and higher insurance rates |

| Market changes | Tough market changes, such as supply chain issues and shortages, have contributed to rising insurance rates |

Explore related products

What You'll Learn

![]()

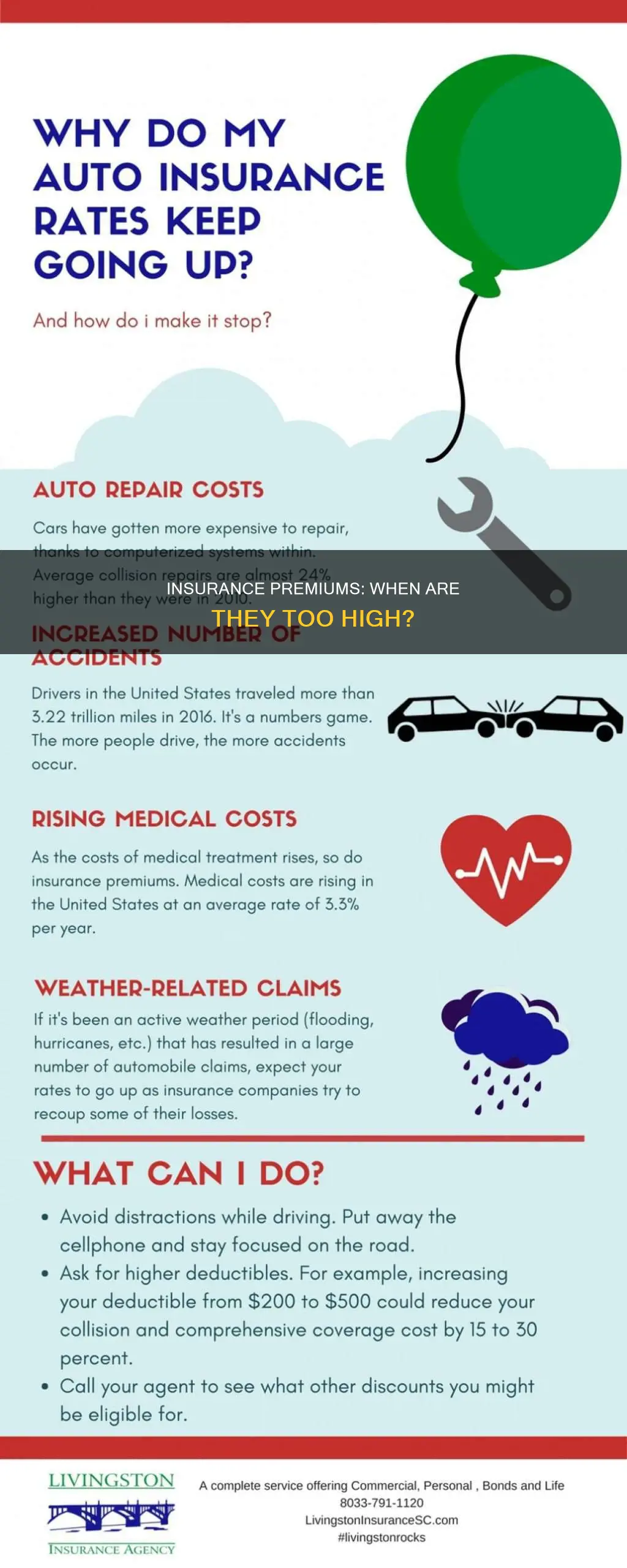

Inflation and rising costs of car repairs

Inflation has had a notable impact on the cost of car repairs. Despite overall inflation slowing to 3.7% in August 2022, down from its 9% peak earlier that year, the cost of vehicle repairs rose by 17% over the same period. Motor vehicle repair prices jumped by 23% from 2022 to 2023, an inflation rate nearly four times higher than overall price increases. This was partly due to a shortage of workers and car parts, which sent costs soaring for auto shops. The pandemic caused mass layoffs and slowed the return of workers, and companies had to raise wages to attract workers, passing on these costs to customers.

The rise of high-tech cars has also contributed to the increased cost of repairs. Repairs to advanced driver-assistance systems and other new technologies can be very expensive, and even some routine repairs now carry added costs. This has resulted in customers opting for basic repairs over more comprehensive ones.

The cost of car repairs is a significant concern for many people, especially those who depend on their vehicles for work. With wages remaining stagnant, many vehicle owners are struggling to keep up with the rising costs of repairs. This has also impacted insurance costs, as insurers are receiving a greater number of claims as more people opt for insurance payouts to cover the cost of repairs.

Canceling Auto Insurance: How and When to Get Out of a Policy

You may want to see also

Explore related products

![]()

Natural disasters and accidents

On the other hand, home insurance premiums are significantly influenced by location. Homeowners in high-risk areas prone to natural disasters, such as hurricanes, tropical storms, wildfires, tornadoes, flooding, and earthquakes, may pay significantly higher insurance rates than those in lower-risk regions. For example, Florida, which is often affected by hurricanes and tropical storms, has an average annual car insurance cost of $3,536, while Vermont, which is not prone to such weather events, has an average rate of $1,237. As the frequency and severity of natural disasters increase due to climate change, reinsurance companies have increased their rates for insurance companies, which is then passed on to policyholders.

It is worth noting that standard homeowners insurance policies often exclude coverage for certain natural disasters like earthquakes, floods, mudflows, landslides, and tsunamis. Homeowners in high-risk areas may need to purchase separate insurance policies for these events, which can be expensive. Additionally, insurance for vehicles damaged on a property by natural disasters is typically not covered by homeowners insurance, and a separate car insurance claim must be filed.

The impact of natural disasters and accidents on insurance costs is complex and far-reaching. As the frequency and severity of these events increase due to climate change, insurance companies will continue to adjust their rates and coverage policies to mitigate their risks. This, in turn, affects the affordability of insurance for many individuals, especially those in high-risk areas.

Auto Insurance Non-Renewal: What You Need to Know

You may want to see also

Explore related products

![A Bridge Too Far [Blu-ray]](https://m.media-amazon.com/images/I/51byTDpw9iL._AC_UY218_.jpg)

![The High Note [Blu-ray]](https://m.media-amazon.com/images/I/71M5wA1478L._AC_UY218_.jpg)

![The High Note [DVD]](https://m.media-amazon.com/images/I/714yvBkcXbL._AC_UY218_.jpg)

![]()

Your age, gender, and location

Age

The cost of insurance is often correlated with age, with younger people paying higher premiums than older people. This is especially true for car insurance, where teens and young adults are charged higher premiums due to their lack of driving experience. As people age and gain more experience behind the wheel, their insurance costs tend to decrease. However, in the senior years, insurance premiums can start to increase again. It's worth noting that not all states or countries allow age to be used as a rating factor, with Hawaii and Massachusetts banning its use in the US.

Gender

In some places, an applicant's gender is used to determine their insurance premiums. This is because insurance companies traditionally tie gender to an applicant's risk. For example, in the US, short-term health insurance plans often charge women higher premiums than men due to higher medical costs during childbearing years. However, this practice is not universal, and some states in the US, such as California, Hawaii, Massachusetts, Michigan, North Carolina, and Pennsylvania, prohibit the use of gender as a rating factor.

Location

Your location can significantly impact your insurance premiums, especially for car insurance. Urban areas, with their high traffic density and crime rates, often have higher insurance costs compared to rural areas. However, this is not always the case, as some rural areas may have higher insurance due to the risk of wildlife collisions. Additionally, state or regional regulations can play a crucial role in determining insurance premiums, as each state or region may have its own laws and minimum insurance requirements.

Auto Insurance: Understanding Adequate Coverage for Peace of Mind

You may want to see also

Explore related products

![]()

Your driving record and history of claims

Insurance companies use your driving record to assess your risk profile. They consider a customer with multiple violations and incidents on their record to be a high-risk driver and more likely to file a claim, thus costing the company money. As a result, insurers charge higher rates to offset that risk. Minor violations, such as speeding tickets, running a red light, or failing to use a turn signal, are considered less severe, but accumulating too many can still lead to higher insurance premiums.

More serious incidents, like driving under the influence (DUI) or reckless driving, fall into the category of major violations and have a substantial impact on insurance rates, often resulting in significant increases. At-fault accidents also indicate a higher risk of future claims, prompting insurers to adjust premiums accordingly. The more severe the incident, the greater the impact on your rates. For instance, drivers with a DUI on their record pay an average of $203 per month for insurance, which is 50% more than those with a clean driving record.

The impact of your driving record on your insurance costs can vary depending on the insurance company. Each company uses a unique formula to set rates, and while most consider similar factors, the weight assigned to each factor may differ. Insurance companies may also review policyholders' driving records at the time of policy renewal, and changes in your driving history can result in adjustments to your premiums, even mid-policy.

In addition to your driving record, other factors that can influence your insurance costs include your age, location, and the type of vehicle you own. Keeping your driving record clean and taking advantage of discounts offered by insurance companies are some ways to help manage insurance costs.

Car Insurance Requirements for Driving with Turo

You may want to see also

Explore related products

![]()

The type of car you drive

Cars with high safety ratings often result in fewer and less severe injuries in the event of an accident, leading to lower insurance costs. Features like anti-lock brakes, airbags, and collision avoidance systems can all contribute to reduced premiums. Conversely, high-performance sports cars or luxury vehicles tend to be more expensive to insure due to their powerful engines and higher repair costs.

The price of your car is a factor in determining insurance rates. More expensive cars usually require higher coverage limits, and if your car is leased or financed, you may be required to carry additional insurance, such as collision and comprehensive coverage, which can increase your premium.

Some cars are more attractive to thieves than others, and this can impact your insurance rates. Vehicles with advanced security features, such as alarms, tracking devices, or immobilizers, may be eligible for insurance discounts. On the other hand, if your car model is commonly targeted by thieves, your insurance rates could be higher.

The availability and cost of car parts can also affect your insurance rates. Rare or exotic cars may have expensive or hard-to-find replacement parts, driving up repair costs and insurance premiums. In contrast, common car models with readily available parts may be more affordable to insure.

Finally, the age of your car matters. Older cars may not have the latest safety features, and their parts may become harder to find over time, making repairs more expensive and increasing insurance rates.

Discovering Your Auto Insurance NAIC Code: A Step-by-Step Guide

You may want to see also

Frequently asked questions

There are many factors that determine your insurance premium. Some of the most common factors include your deductible, the kind of car you drive, driving record, claim history, commute, credit score, history of paying for insurance, your location, age, gender and add-ons to your policy.

The make and model of your car, its safety rating, and its mileage can all affect your insurance premium. Cars that do well on safety tests tend to have lower insurance premiums.

Insurance premiums can vary widely from state to state and even from place to place within the same state. If you live in an area with a high crime rate or high population density, your insurer may charge a higher rate.

Drivers under 25 and over 75 tend to have higher insurance premiums as insurers see their policies as high-risk insurance.