A Health Savings Account (HSA) is a tax-advantaged account that can be used to pay for current or future healthcare expenses. It allows you to set aside pre-tax money to pay for medical costs, and the money grows tax-free. To be eligible for an HSA, you must have a high-deductible health plan (HDHP), which typically has lower monthly premiums but higher deductibles. You can use your HSA to pay for a variety of expenses, including deductibles, co-insurance, prescriptions, vision, and dental care. The money in your HSA is always accessible and can be withdrawn using a debit card or through online transfers. It's important to note that HSA funds generally cannot be used to pay insurance premiums unless it is for specific types of insurance, such as long-term care insurance or COBRA coverage during unemployment.

| Characteristics | Values |

|---|---|

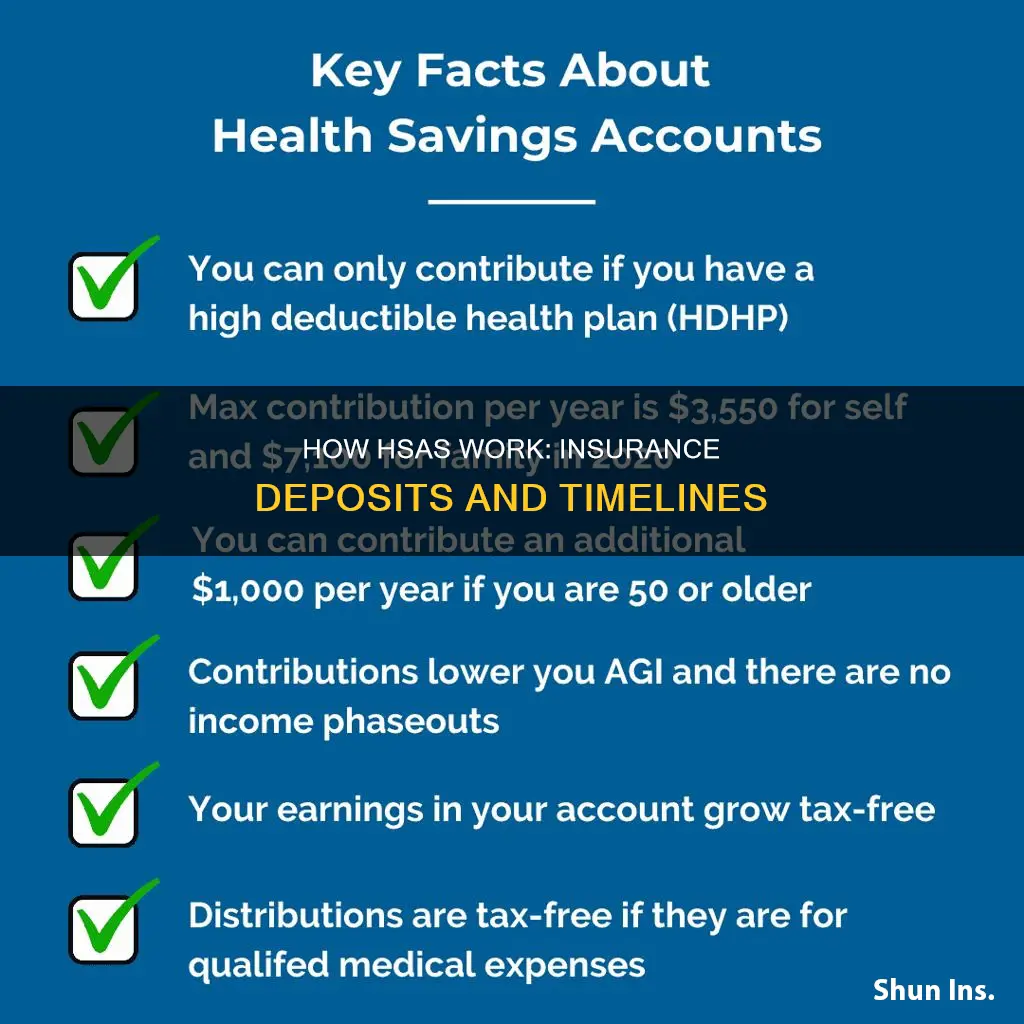

| When can you contribute to an HSA? | When you get your health coverage from a high-deductible health plan (HDHP) |

| How do you set up an HSA? | With a trustee, which can be a bank, an insurance company, or anyone already approved by the IRS to be a trustee of individual retirement arrangements (IRAs) or Archer MSAs |

| When can you use the money in your HSA? | Whenever you want, even if you change jobs or retire |

| What can you use your HSA for? | Qualified medical expenses, including copays, coinsurance, and other health care costs not covered by your health plan, such as vision and dental care, prescription drugs, over-the-counter health products, family planning expenses, and menstrual care products |

| Can you use your HSA for insurance premiums? | Only for certain types of insurance premiums, such as COBRA coverage while unemployed, Medicare premiums if you're 65 or older, and long-term care insurance |

| How do you pay for expenses with your HSA? | With an HSA Bank Health Benefits Debit Card at a point of sale with a signature or PIN, or by reimbursing yourself for eligible expenses paid out-of-pocket at an ATM |

| Can you deduct HSA contributions from your taxable income? | Yes, you can deduct the amount you deposit in an HSA from your taxable income, and any unspent funds roll over from year to year |

| What happens to your HSA when you turn 65? | You can withdraw money from your HSA for any reason without paying a tax penalty, but you'll owe income tax on withdrawals for non-medical expenses |

Explore related products

![]()

HSA eligibility

A Health Savings Account (HSA) is a tax-exempt trust or custodial account that individuals set up with a qualified HSA trustee to pay or reimburse certain medical expenses. To be eligible for an HSA, you must meet the following requirements:

- You are covered under a high-deductible health plan (HDHP) on the first day of the month.

- You have no other health coverage except what is permitted.

- You aren't enrolled in Medicare.

- You can't be claimed as a dependent on someone else's tax return.

Under the last-month rule, you are considered an eligible individual for the entire year if you are an eligible individual on the first day of the last month of your tax year (December 1 for most taxpayers) and you meet certain other requirements. If you meet these requirements, you are an eligible individual even if your spouse has non-HDHP family coverage, provided that your spouse's coverage doesn't include you.

An HSA is "portable" and stays with you if you change employers or leave the workforce. It is a unique tax-advantaged account that can be used for current or future healthcare expenses. You can deduct the amount you deposit in an HSA from your taxable income, and unspent funds roll over from year to year. HSA funds can be used to pay for deductibles, co-insurance, prescriptions, vision, dental care, and more. Once you turn 65, you can use the money in your HSA for anything you want.

Maximizing Your Blackjack Strategy: Insurance Explained

You may want to see also

Explore related products

![]()

HSA tax benefits

A Health Savings Account (HSA) offers a triple-tax advantage. Firstly, deposits are tax-deductible. Secondly, growth is tax-deferred. Thirdly, spending is tax-free. All contributions to your HSA are tax-deductible, or if made through payroll deductions, are pre-tax, which lowers your overall taxable income. Your contributions may be 100% tax-deductible, meaning contributions can be deducted from your gross income. All interest earned in your HSA is 100% tax-deferred, meaning the funds grow without being subject to taxes unless they are used for non-eligible medical expenses. Withdrawals from your HSA are 100% tax-free for eligible medical expenses (i.e. deductibles, copays, prescriptions, vision, and dental care).

HSA funds can be used to pay for IRS-qualified healthcare expenses, including deductibles, co-insurance, prescriptions, vision, dental care, and more. You can use a Health Benefits Debit Card to access your HSA funds at the point of sale, at an ATM, or to reimburse yourself for eligible expenses paid out-of-pocket (a transaction fee may apply).

HSA funds roll over from year to year and can be held and added to tax-free savings to pay for medical care later. You can also invest your HSA funds, which remain in the investment account. HSAs offer the potential for long-term, tax-free savings that can be used for future healthcare expenses, including out-of-pocket expenses after retirement, Medicare, and long-term care (LTC) premiums, up to IRS limits and certain LTC expenses.

Admitting Fault: Navigating the Complexities of Insurance Adjusters

You may want to see also

Explore related products

![]()

HSA-eligible expenses

A Health Savings Account (HSA) is a unique tax-advantaged account that can be used for current or future healthcare expenses. HSA-eligible expenses are designated by the IRS and include medical, dental, vision, and prescription expenses. These expenses are subject to change by the IRS at any time. It is important to verify that the expenses incurred are designated as HSA-eligible expenses by both the IRS and the plan sponsor.

Some examples of HSA-eligible expenses include deductibles, co-insurance, prescriptions, vision, and dental care. Additionally, transportation to medical appointments, such as Alcoholics Anonymous (AA) meetings, is also considered an eligible expense. In some cases, alternative treatments such as acupressure may be eligible for reimbursement with a Letter of Medical Necessity (LMN) from a medical professional.

HSA funds can also be used for adaptive equipment reimbursement and eligible expenses incurred for a dependent adopted child. It's important to note that adult day care reimbursement is typically not eligible with an HSA, but it may qualify under a dependent care flexible spending account (DCFSA) in certain circumstances.

While HSA funds generally cannot be used to pay premiums, they can be used for qualified medical expenses that Medicare doesn't cover once you turn 65. Any unspent funds in your HSA can be rolled over from year to year, allowing you to save for future healthcare needs. You can easily access your HSA funds using a Health Benefits Debit Card at eligible merchants or through online transfers to your bank account.

How Much Can Insurers Spend on Ads?

You may want to see also

Explore related products

![]()

HSA debit cards

A Health Savings Account (HSA) is a tax-advantaged account that can be used for current or future healthcare expenses. HSA debit cards are offered by several banks, including Bank of America, HSA Bank, and Associated Bank. These cards provide easy access to your HSA funds and allow you to pay for eligible healthcare products and services directly at the point of sale.

When using an HSA debit card, payments are automatically deducted from your account, and you don't need to submit receipts to verify your purchases. However, it's important to maintain detailed records of expenses reimbursed through your HSA in case of an IRS audit. The daily purchase limit for the HSA debit card varies depending on the merchant type and generally ranges from $3,500 to $5,000. Additionally, the number of transactions allowed per day is limited to safeguard against fraudulent activity.

Bridging the Gap: Effective Strategies for Communicating Treatment Gaps to Insurance Adjusters

You may want to see also

Explore related products

![]()

HSA rollover

A Health Savings Account (HSA) rollover is when you transfer your HSA from one provider to another. This could be an HSA that you open on your own at a financial institution or one that you get access to through a new employer. HSAs are portable, meaning you can carry them with you from company to company and health plan to health plan.

There are several benefits to an HSA rollover:

- Centralizing your health savings and simplifying account management.

- Minimizing fees.

- Accessing investments that align with your goals.

- Maintaining pre-tax contributions via payroll deductions.

- Ability to meet investment thresholds.

- No closure due to inactivity.

- Your old provider may directly transfer your funds and any investments to your new provider.

- Your old provider may ask you to sell off your investments and then transfer only cash to your new provider.

- Your old provider may ask you to sell your investments and then send a check or electronic transfer with your HSA funds directly to you. If you receive a check or electronic transfer, you must deposit the funds yourself with the new provider within 60 days. If you don’t, the IRS considers this a taxable withdrawal, which means you may owe taxes and a 20% penalty.

It's important to note that you are allowed by law to perform only one indirect rollover every 12 months. Direct transfers, on the other hand, can be done without limit.

Unraveling the Complexities of Fault Determination: A Guide to the Insurance Adjuster's Process

You may want to see also

Frequently asked questions

You can set up an HSA with a trustee, which can be a bank, an insurance company, or anyone already approved by the IRS to be a trustee of individual retirement arrangements (IRAs) or Archer MSAs. You can contribute to your HSA through your paycheck before taxes are taken out, or you can make after-tax contributions and claim these as deductions when filing your federal income tax return.

You can use your HSA to pay for qualified medical expenses, including copays, coinsurance, and other health care costs not covered by your health plan. This can include standard doctor visits, vision and dental care, prescription drugs, over-the-counter health products, family planning expenses, and even menstrual care products. Additionally, your HSA may cover limited types of insurance premiums, such as COBRA coverage while you are unemployed.

You can use the money in your HSA whenever you want to pay for qualified medical expenses. The money in your HSA never expires and stays with you even if you change jobs or retire. Once you turn 65, you can use the money in your HSA for anything you want, but you will owe income tax on withdrawals for non-medical expenses.

You can access your HSA funds through a Health Benefits Debit Card, which can be used at points of sale with a signature or PIN, or at ATMs for withdrawals. You can also pay providers directly from your HSA through a mobile app or website, or transfer funds to an external bank account.